Threefold Overlapping SuperTrend Strategy

Overview

This is a strategy that makes trading decisions based on three overlapping SuperTrend indicators. It can capture larger directional opportunities in trending markets.

Strategy Logic

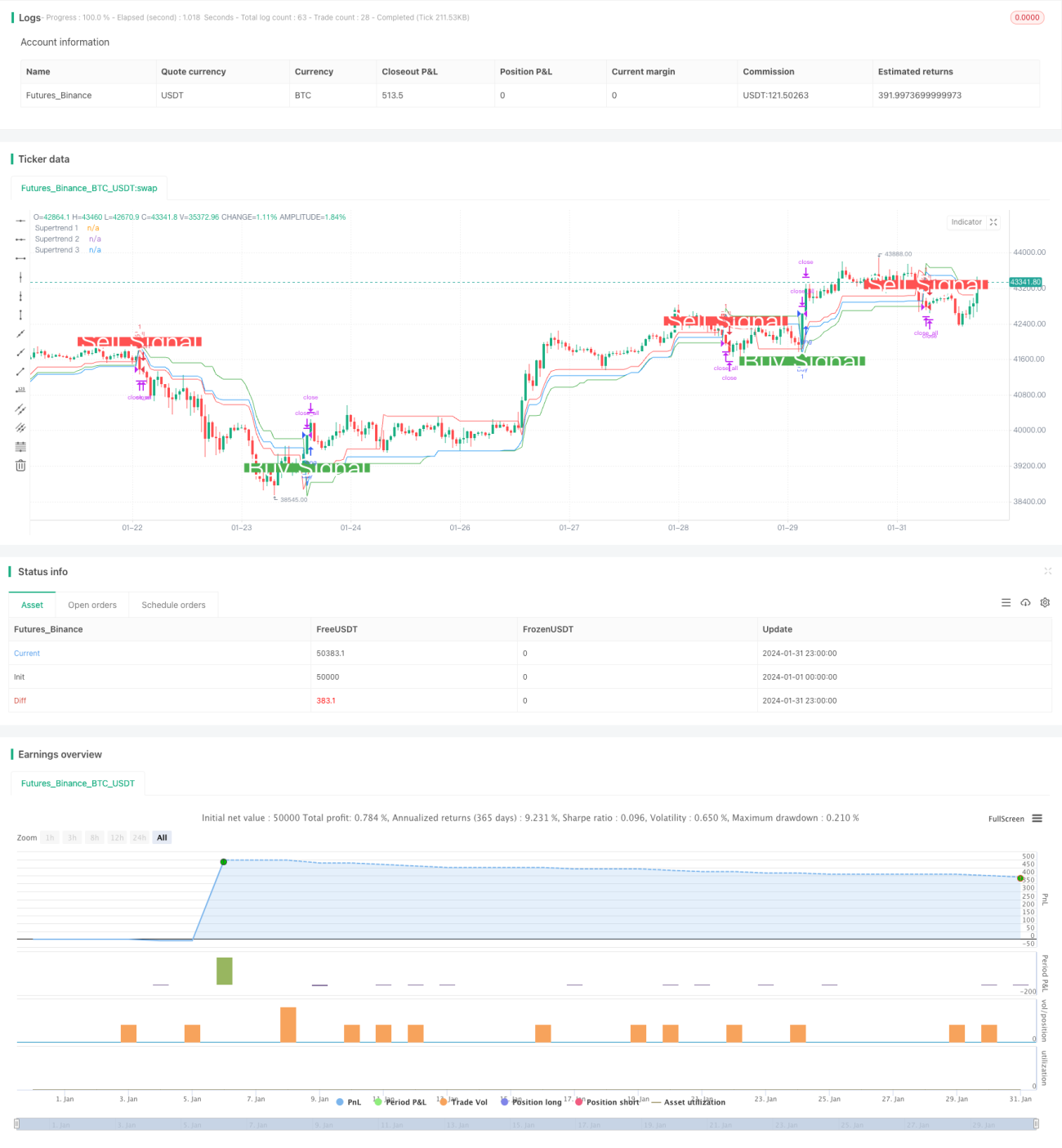

The strategy uses the ta.supertrend() function to calculate three SuperTrend indicators with different parameter settings, namely SuperTrend1 with 10 days and a multiplier of 3, SuperTrend2 with 14 days and a multiplier of 2, and SuperTrend3 with 20 days and a multiplier of 2.5. A buy signal is generated when the price crosses above all three SuperTrend lines. A sell signal is generated when the price crosses below all three SuperTrend lines.

The SuperTrend indicator incorporates the ATR indicator to effectively track price trend changes. The strategy of three overlapping SuperTrends makes the signals more reliable, thereby capturing greater profits in trending markets.

Advantages

- Triple filter mechanism avoids false signals and improves signal quality

- The SuperTrend itself has good noise reduction capability

- Multiple combinations of hyperparameters can be configured to suit more market environments

- Good historical performance with high return to risk ratio

Risks

- Multiple filtering signals may miss some opportunities

- Does not perform well in ranging markets

- Requires optimization of combinations of three sets of hyperparameters

- Concentrated trading time is susceptible to sudden events

The following can be considered to reduce risks:

- Adjust the filtering conditions, keep one or two SuperTrends

- Add stop loss strategy

- Optimize hyperparameters to improve win rate

Optimization Directions

- Test more parameter combinations to find optimal hyperparameters

- Add machine learning algorithms for real-time parameter optimization

- Add stop loss strategies to control single loss

- Incorporate other indicators to identify trends and ranges

- Extend trading time to avoid risks at a single time point

Conclusion

This strategy makes decisions based on three overlapping SuperTrends, which can effectively identify trend direction. It has advantages like high signal quality and configurable parameters. At the same time, there are also certain risks. Parameters and exit timing need to be adjusted to adapt to different market environments. Overall, the strategy performs exceptionally well and is worth further research and application.

- 1