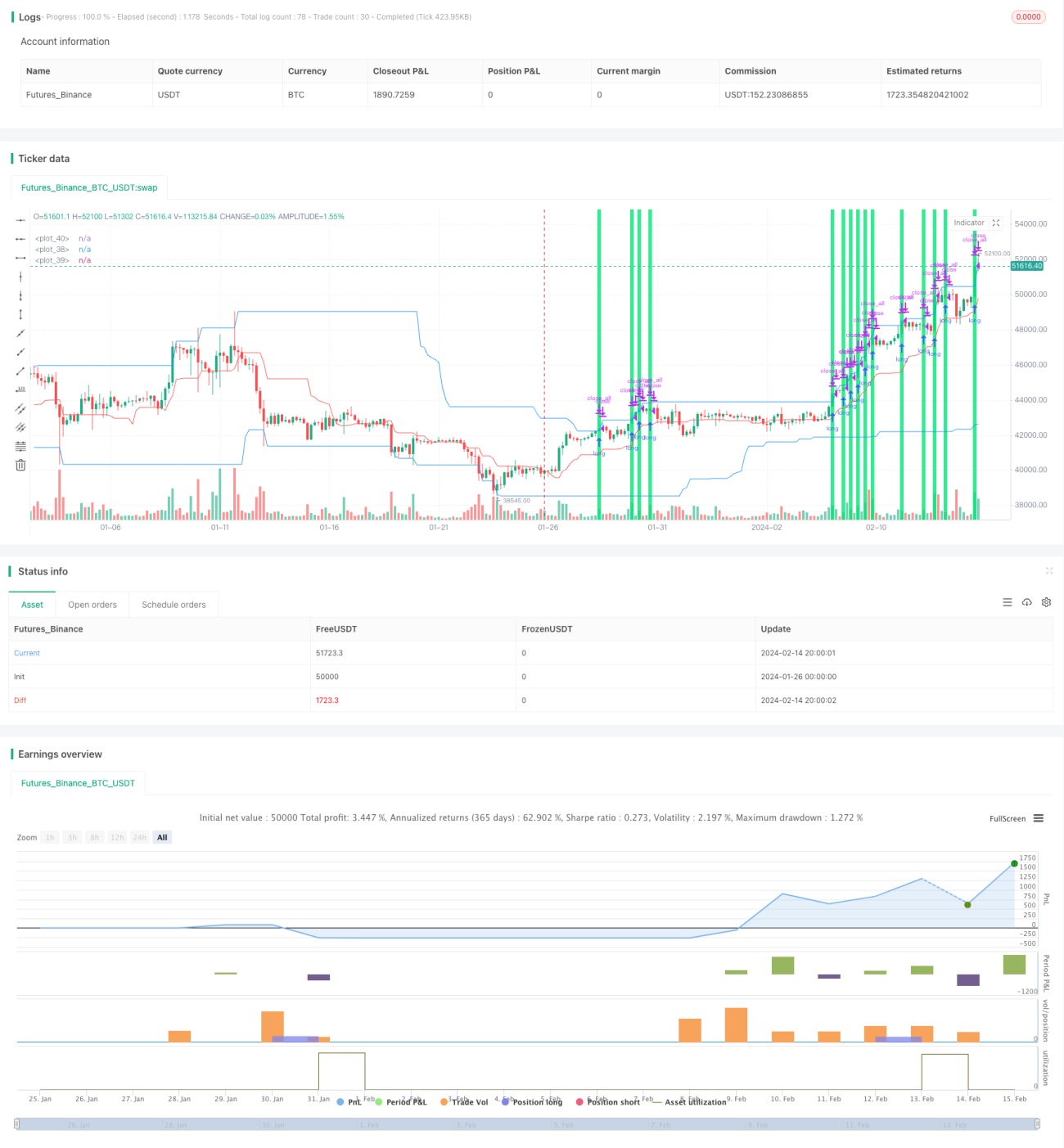

Turtle Trading Strategy Based on Donchian Channels

Overview

The Tang Anqi Turtle Trading Strategy is a highly simplified version of the original Turtle Trading Strategy. It is very different from the original Turtle strategy. The strategy uses two Donchian Channels, a fast channel and a slow channel. The channel periods are set by the user, with default values of 20 bars for the fast channel and 50 bars for the slow channel. The strategy utilizes the upper and lower bands of the slow channel to entry trades and the middle band of the fast channel to set stop loss.

Strategy Logic

The core logic of this strategy is:

-

Calculate the fast Donchian Channel: The upper band is the highest high over the past fast bars, the lower band is the lowest low, and the middle band is the average of the upper and lower bands.

-

Calculate the slow Donchian Channel: The upper band is the highest high over the past slow bars, the lower band is the lowest low.

-

When there is no position, a long signal is triggered when price touches the upper band of the slow channel, and a short signal is triggered when price touches the lower band of the slow channel.

-

After opening a position, the middle band of the fast channel is used as the stop loss.

-

Close the position when there is an opposite signal as the opening signal during the holding period.

Advantage Analysis

The advantages of this strategy are:

-

Simple rules easy to implement. Donchian Channels and moving stop loss are easy to understand, suitable for beginners.

-

Customizable parameters. Users can adjust parameters based on trading products and timeframes to adapt to different market environments.

-

Few conflicting trading signals. Only relies on price breakouts of channel bands, avoids false signals from common indicators.

-

Automatic stop loss management. The moving stop loss based on the fast channel middle band can limit losses on single trades.

Risk Analysis

The risks facing this strategy include:

-

More stop loss when trend is unclear. This affects the profitability of the strategy.

-

Larger drawdowns possible. When trend reverses, floating profits in the previous trend direction will realize into losses.

-

Improper parameter settings lead to over-aggressiveness or over-conservativeness. Proper values need to be found through repeated backtesting.

-

High dependence on automated trading. Server stability is important to avoid exceptions leading to failure in automated trading.

To reduce the above risks, parameters can be optimized, position sizing can be appropriately limited, and risk management modules can be added.

Optimization Directions

The strategies can be improved in the following aspects:

-

Add filters for entry signals to avoid catching trend reversal signals. For example, use trend indicators to determine trend direction.

-

Optimize parameters like channel periods and position sizing to fit different trading instruments better.

-

Add risk management modules like maximum drawdown limits and daily loss limits to prevent excessive losses in extreme events.

-

Improve stop loss strategies. For example, adopt trailing stop loss to make stops more adaptive to market trends.

Conclusion

In summary, the Tang Anqi Turtle Trading Strategy is a simple trend following system. Its advantages lie in its ease of understanding and automation. But it also carries certain risks, and further optimizations on parameters and risk management are needed to make it more practical. With measures like parameter tuning, adding filters, and risk control modules, the strategy can achieve better results in live trading.

- 1