SuperTrend Breakout Strategy

Overview

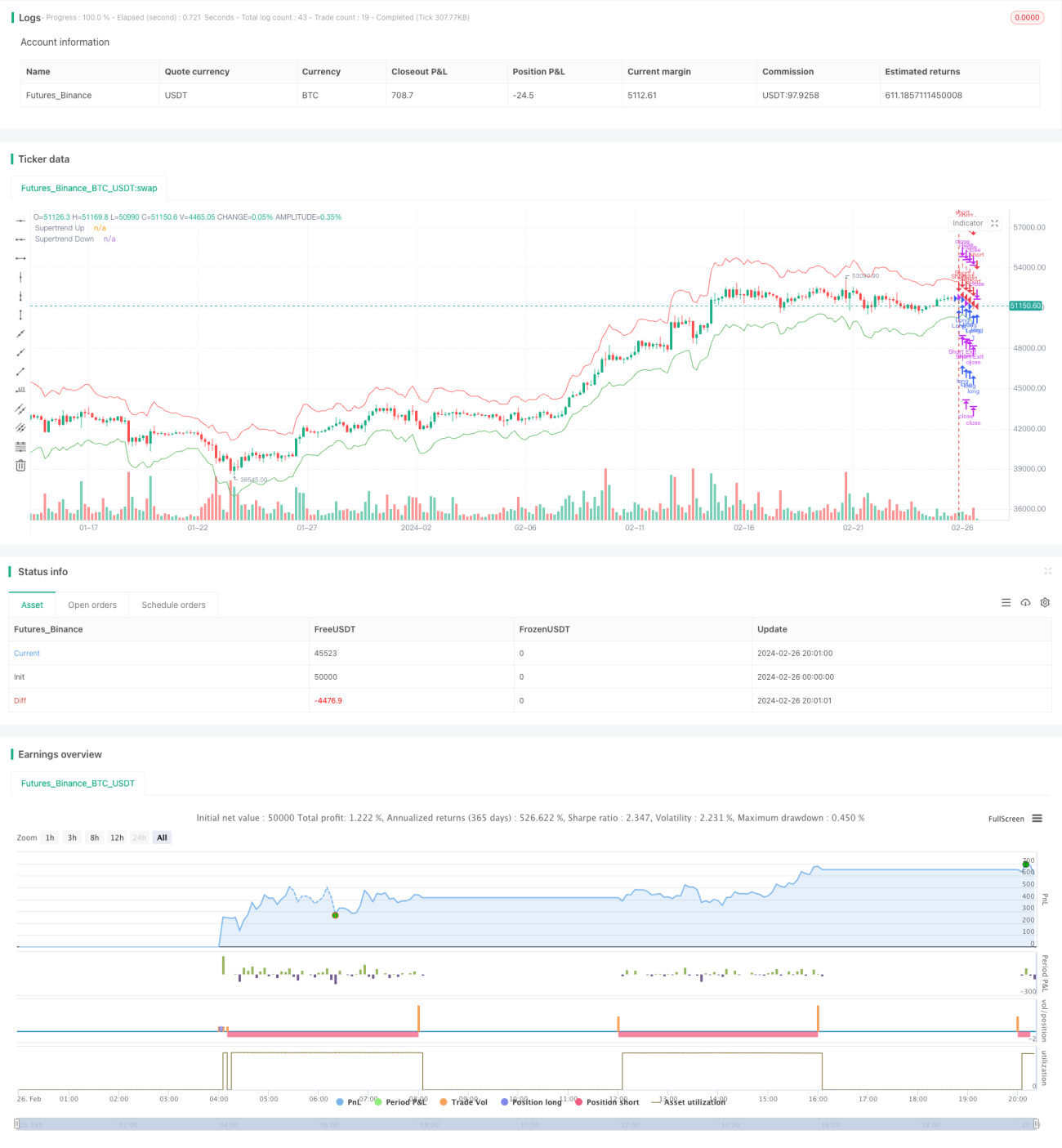

This strategy generates trading signals when price breaks out of the uptrend/downtrend channel formed by the SuperTrend indicator. The strategy has outstanding trend following ability.

Strategy Logic

The strategy first calculates the ATR indicator as a measure of price volatility, then combines it with the average of highest, lowest and closing prices to compute the upper and lower bands. When price breaks above the lower band during an uptrend, a buy signal is generated. When price breaks below the upper band during a downtrend, a sell signal is triggered. This forms an adaptive uptrend/downtrend channel that tracks price trends.

After entering the market, the strategy sets target profit ticks and stop loss ticks. It closes position for profit when price reaches the profit target, and stops out when drawdown hits the stop loss level.

Advantage Analysis

The biggest advantage of this strategy is its excellent trend following ability. The adaptive channel can capture trend changes quickly. Using ATR also provides some assurance of trading along with momentum. In addition, the profit target and stop loss mechanism gives clear risk/reward control.

Risk Analysis

One major risk is that it may generate excessive whipsaws during range-bound markets, as the price constantly pierces through the bands. In addition, stop loss setting also directly impacts final results.

To reduce such risks, parameters like ATR period or channel multiplier could be optimized to fit the true trend better. Other filters may also be added on entry signals to avoid whipsaws.

Enhancement Opportunities

The strategy can be enhanced in several aspects:

-

Optimize ATR parameters to better reflect actual volatility dynamics.

-

Test different multipliers for channel width optimization.

-

Add other indicators as filters on entries, e.g. MACD for better timing.

-

Optimize profit target and stop loss levels for maximized risk-adjusted returns.

-

Consider other objectives like Sharpe ratio or profit factor to evaluate overall quality.

Summary

The strategy leverages the adaptive channel breakout model to achieve great trend following ability. It also has clear risk control mechanisms. With further parameter tuning and logic enhancement, it has the potential to work even better across various market conditions and asset classes.

- 1