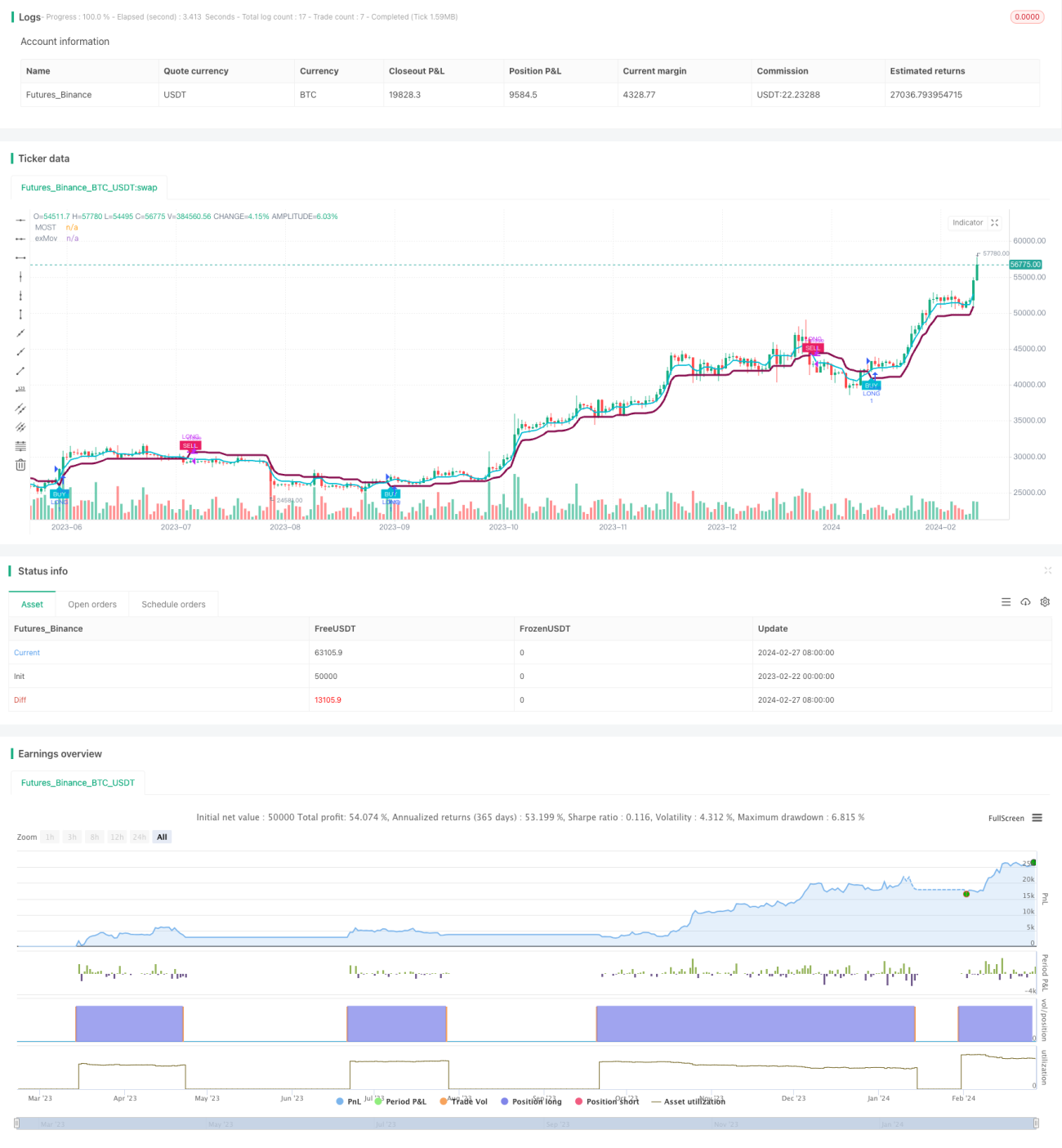

Trend Riding Strategy Based on MOST and KAMA

This strategy combines multiple moving averages such as SMA and EMA to identify price trend direction, and sets stop loss lines based on price breakthrough to design a trend following strategy. When prices rise, it trails the upper band as a stop loss; when prices fall, it trails the lower limit as a stop loss. The advantage of the strategy is that the combination of multiple moving averages can smooth price data and identify trends; The dynamic stop loss design avoids overly sensitive stops. The risk of the strategy is that the Setting of the stop loss line may be too loose to stop loss in time.

Strategy Principle

This strategy uses KAMA as the basis for judging trend direction, because KAMA responds to price changes more sensitively and can identify turns in advance. At the same time, the strategy contains combinations of other multiple moving averages such as SMA and EMA to filter prices and identify main trend directions.

The strategy's stop-loss line setting is based on the price itself and the moving average. Specifically, the upward trailing stop loss line is the moving average plus a proportion as a buffer; The downward trailing stop loss line is the moving average minus a proportion as a buffer. This allows for immediate stop loss when prices reverse.

The entry conditions are long when prices break through the upside stop loss line from bottom up; short when prices break through the downside stop loss line from top down.

Advantage Analysis

The biggest advantage of this strategy is that by combining multiple moving averages, the accuracy of trend judgment can be improved and false signals can be reduced. At the same time, the strategy's stop loss line changes dynamically based on the moving average, which can adjust in real time and respond to sudden events.

In addition, compared to single indicator strategies, this strategy combines the advantages of trend tracking and breakthrough strategies. In a trending market, it can maximize profits; while in a whipsaw market, it can reduce losses through stop loss settings.

Risk Analysis

The main risk of this strategy is that the stop loss line setting may be too loose to stop loss in time. This is because the retracement ratio of the stop loss line is fixed, if there is a violent change in the market, the stop loss line cannot be updated in time, which may lead to greater losses.

In addition, Moving Average itself has high hysteresis and cannot react immediately to price changes. This may also lead to failure to stop loss in time when the market reverses rapidly.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Test different parameter settings for stop loss line ratios to find better parameter combinations;

-

Try to make the stop loss line change dynamically according to the degree of market fluctuation;

-

Increase other indicators to judge, introduce more variables in the stop loss basis to improve the adaptability of the strategy;

-

Optimize the cycle parameters of the moving average to find the best cycle setting to smooth prices.

Summary

Overall, this strategy is quite robust, combining multiple moving averages to determine trend direction, and designing a dynamic trailing stop loss mechanism aiming to follow trends. The advantages are that it can reduce false signals, control risks through stop loss; The disadvantage is that the stop loss line may be set too wide to stop loss quickly. The next step to optimize the strategy should focus on the design of the stop loss line to make it adjustable dynamically according to market changes.

/*backtest

start: 2023-02-22 00:00:00

end: 2024-02-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Atlantean Trend Signal BUY SELL Strategy', overlay=true)

ma_length = input.int(title='Moving Average Length', minval=1, defval=3)- 1