Triple Confirmation Trend Tracking Strategy

Overview

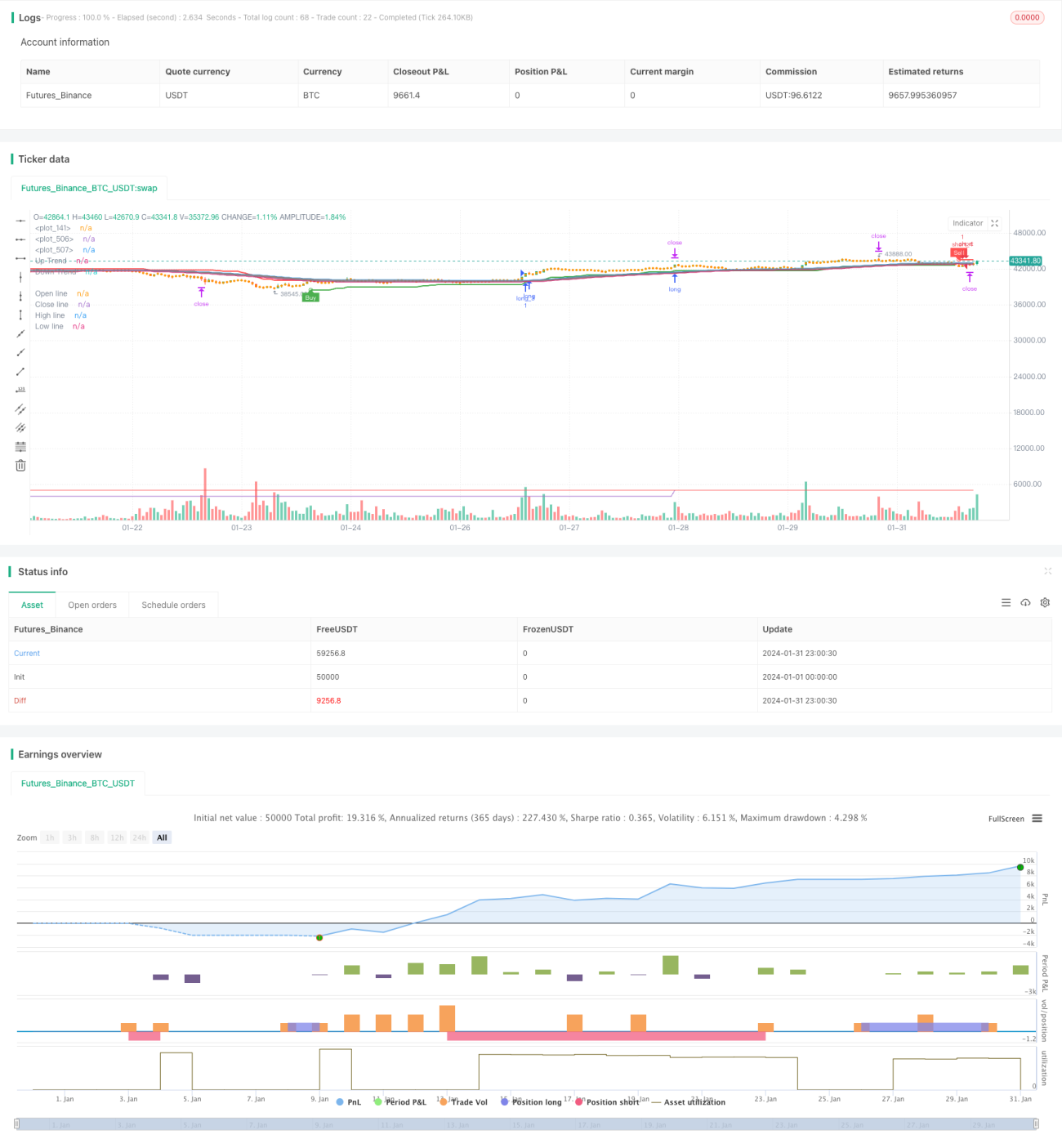

The Triple Confirmation Trend Tracking strategy captures trend signals with high probability by combining signals from three major indicators - Moving Average, Heiken Ashi and Supertrend. When all three indicators give buy or sell signals simultaneously, the strategy will enter trades timely to track trends. When trend reverses, the strategy will quickly stop loss and even open reverse positions.

How The Strategy Works

Moving Average Judges Main Trend

The strategy uses a Moving Average of 52 periods to determine the main trend direction. When price crosses above MA, it indicates an upward trend. When price crosses below MA, it indicates a downward trend.

Heiken Ashi Identifies Secondary Reversals

The strategy also uses Heiken Ashi to identify secondary short-term reversals. Heiken Ashi is calculated similarly to Moving Average but with open prices instead of close prices, thus able to reflect reversal signals faster. When price crosses above a falling Heiken Ashi line, it signals stabilizing rebound. When price crosses below a rising Heiken Ashi line, it signals short-term pullback.

Supertrend Determines Key Reversal Points

Additionally, the strategy incorporates Supertrend indicator to spot key reversal points. Supertrend combines ATR and price data to dynamically adjust upper/lower channel bands and hence effectively judge reversals.

Triple Confirmation Filter

Only when signs of all three indicators line up, the strategy will go long. When all three give sell signals, the strategy will open short positions. The triple confirmation mechanism filters out false signals substantially and ensures high-probability setups.

Strengths Analysis

High Probability with Multi-dimensional Assessment

The combinted signals of Moving Average, Heiken Ashi and Supertren from different dimensions ensure high-probability entry.

Promptly Reacts and Tracks in Real Time

The introduction of Heiken Ashi ensures fast response to short-term reversals. The adaptive Supertrend channel also tracks price changes timely.

Auto Profit Taking & Loss Cutting

The inbuilt auto profit-taking and stop-loss mechanism dynamically adjusts profit/loss levels based on ATR, effectively capping losses per trade.

Risks & Solutions

Excessive Trading Frequency

The abundance of trading signals may incur over-trading. Moderately increasing the MA period helps to limit trade frequency.

Uncertainty of Reversal Judgement

Heiken Ashi and Supertrend may falsely identiy key reversals. Additional filter conditions on indicator parameters can enhance reversal reliability.

Loss Risk in Range-bound Market

In raging markets, repetitive crossover signals may trigger frequent opening and stop loss of positions, causing losses. Recognizing and sidelining ranging mode will avoid such losses.

Enhancement Directions

Incorporate Volatility Indicators

Volatility indicators like Bollinger Bands could help avoid opening new trades when price stretches near the bands. This effectively prevents whipsaw loss risks.

Additional Entry Filters

Extra auxiliary indicators like KDJ and MACD can provide additional layers of confirmation signals, allowing only qualified setups to pass through. This further screens out false signals.

Optimize Profit Taking Mechanism

The profit-taking mechanism can be upgraded in various ways, like trail stop, exponential trail stop, partial exit at interval etc., to harvest profit as much as possible in a steady manner.

Conclusion

The Triple Confirmation Trend Tracking Strategy fully leverages the strengths of Moving Average, Heiken Ashi and Supertrend to determine trend signals with high accuracy. The embedded automated profit-taking and stop-loss mechanism also effectively limits per trade loss. Potential areas for further enhancements include incorporating other filters before entry, as well as innovating the profit-taking techniques, in order to make the strategy more practical.

- 1