Dual Moving Average Channel Trading Strategy

Overview

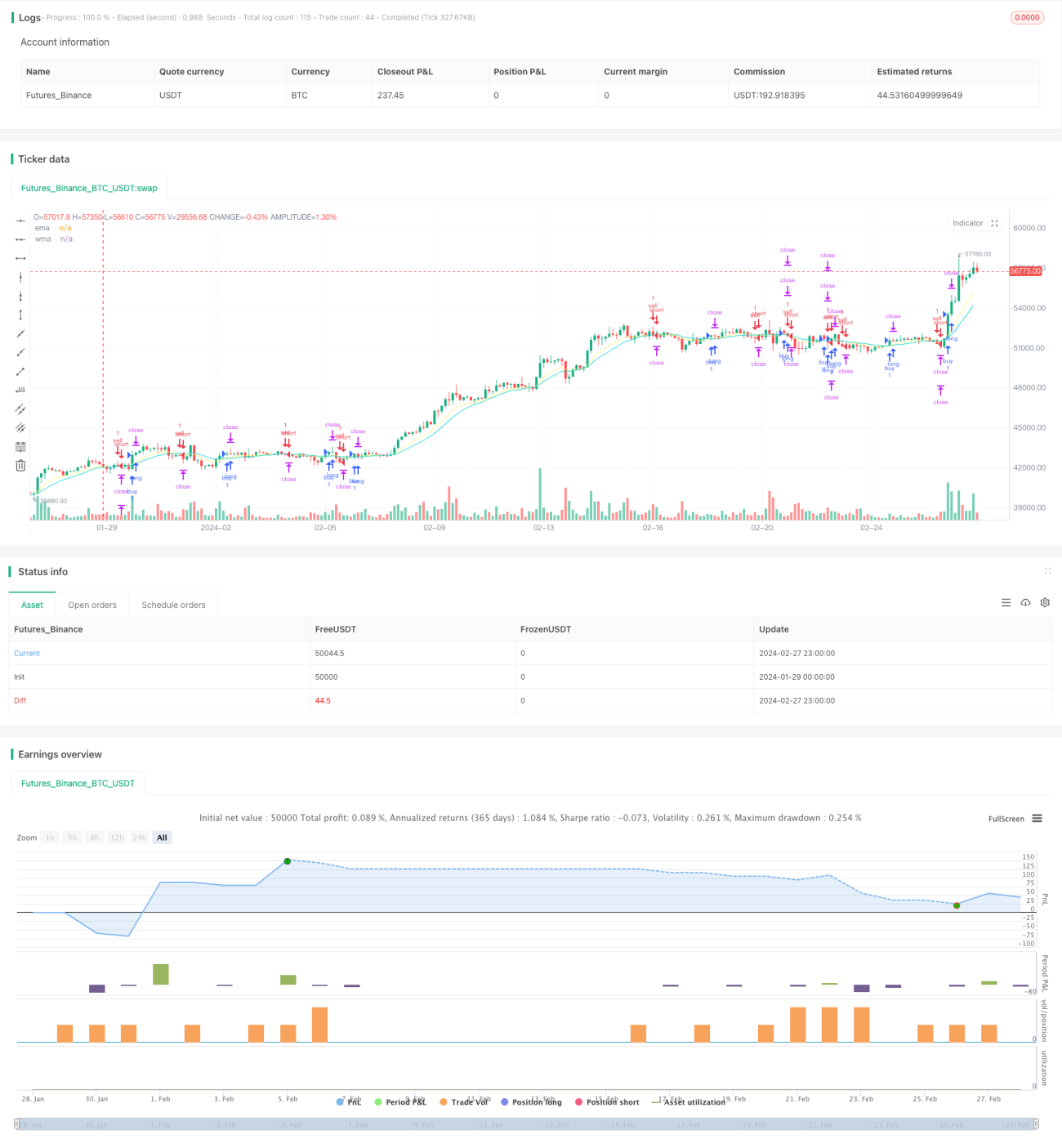

The dual moving average channel trading strategy is a trend trading strategy that tracks crossovers between double moving averages. The strategy uses Exponential Moving Average (EMA) and Weighted Moving Average (WMA) as trading signal indicators. When the short-term EMA crosses above the long-term WMA, the strategy goes long. When the short-term EMA crosses below the long-term WMA, the strategy goes short.

Strategy Logic

The trading signals of this strategy come from the golden cross and death cross between the 10-period short-term EMA and the 20-period long-term WMA. When the short-term EMA crosses above the long-term WMA, it indicates the market is reversing up, thus going long. When the short-term EMA crosses below the long-term WMA, it indicates the market is reversing down, thus going short.

After determining the trading direction, the strategy sets the stop loss below or above the entry price by 1 ATR period, with two take profits - the first take profit is set at 1 ATR above or below the entry price, and the second take profit is set at 2 ATRs above or below the entry price. When the first take profit is triggered, 50% of the position will be closed. The remaining position will keep running towards the second take profit or with a trailing stop loss.

The trailing stop loss logic - it will be activated once the highest price or the lowest price has reached the first take profit level. According to realtime bar update, the stop loss will be trailed between the maximum profit point and entry price as the protection to avoid loss and lock in profit along the way.

Advantage

The strategy utilizes the dual smoothing noise reduction feature of moving averages to effectively filter out random fluctuations in the market and identify medium-to-long-term trend signals, thus avoiding being caught in whipsaws. In addition, the two staged take profits increase the profit zone of the strategy and maximize profits. The trailing stop mechanism also allows the strategy to lock in profits and reduce losses.

Risks

Moving averages themselves have greater lagging, which poses the risk of missing signals. The crossover between double moving averages may also generate excessive false signals in certain markets, causing losses.

The stop loss setting is an important component of the strategy. If the stop loss is too small, it is prone to be hit by market noise. If the stop loss is too large, it may fail to effectively control risks.

In addition, when the market fluctuates violently, the trailing stop may not work very well in protection.

Optimization Directions

-

Test EMAs and WMAs with different parameters to find the optimal parameter combination. Overly short EMAs or overly long WMAs could both impact strategy performance.

-

Choose fixed points or ATR multiple stop loss based on different product characteristics and trading styles.

-

Test the effects of partial position trailing stop and full position trailing stop.

-

Introduce other indicators for signal filtering to assist EMA and WMA, so as to improve signal quality.

Summary

In general, the dual moving average channel trading strategy is relatively robust and performs well in trending markets. By optimizing parameters, stop loss mechanisms, and improving signal quality, the real trading performance of this strategy can be further enhanced. This is a promising strategy idea that is worth in-depth research and application in actual trading.

- 1