Quant Trading Strategy Based on HullMA Percentage Bands

Overview

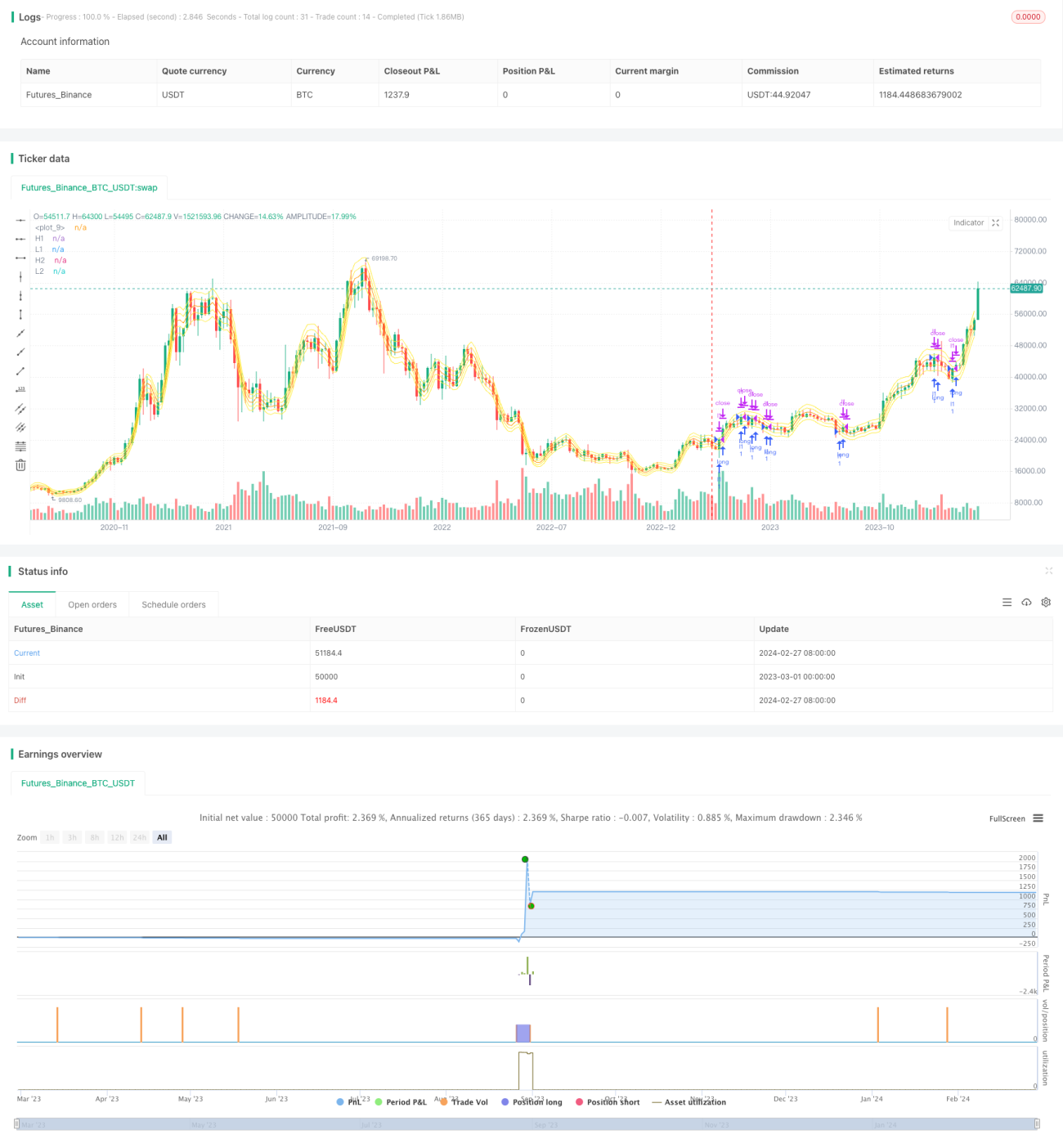

This strategy implements quantitative trading through calculating Hull moving average and its percentage bands to make entry and stop-loss decisions. Its advantages include adjustable parameters, simple implementation, and strict stop loss. But risks like chasing peaks and killing dips, frequent trading also exist. Further optimizations on stop loss strategy and adding short-term operations could lead to better performance.

Strategy Principle

-

Calculate Hull moving average hullma with length length.

-

Plot percentage bands xL1, xL3, xL2, xL4 based on hullma.

-

Long when close crosses below xL2 or xL4, close long when close crosses above xL1, xL2 or xL3.

Advantage Analysis

The advantages include:

-

HullMA is sensitive to price changes and tracks trends well.

-

Percentage bands are highly adjustable for different products.

-

Dual bands strategy filters out wrong signals effectively.

-

Stop loss strategy controls risks effectively.

Risk Analysis

Some risks:

-

Chasing peaks and killing dips.

-

Slippage from frequent trading.

-

Improper parameter tuning leads to overtrading.

-

Stop loss position needs iterative optimization.

Optimization Directions

Some optimization directions:

-

Optimize hullMA length parameter for different products.

-

Optimize percentage bands to reduce wrong trades.

-

Add short-term operations to get more profits.

-

Optimize stop loss strategy to ensure effectiveness.

-

Test robustness across different products.

Conclusion

This strategy builds a relatively simple breakout trading system using HullMA and percentage bands. With clear pros and cons, and further optimizations on parameters and functionalities, it can become a very practical quant strategy.

- 1