The Dual Moving Average Crossover Strategy

Strategy Overview

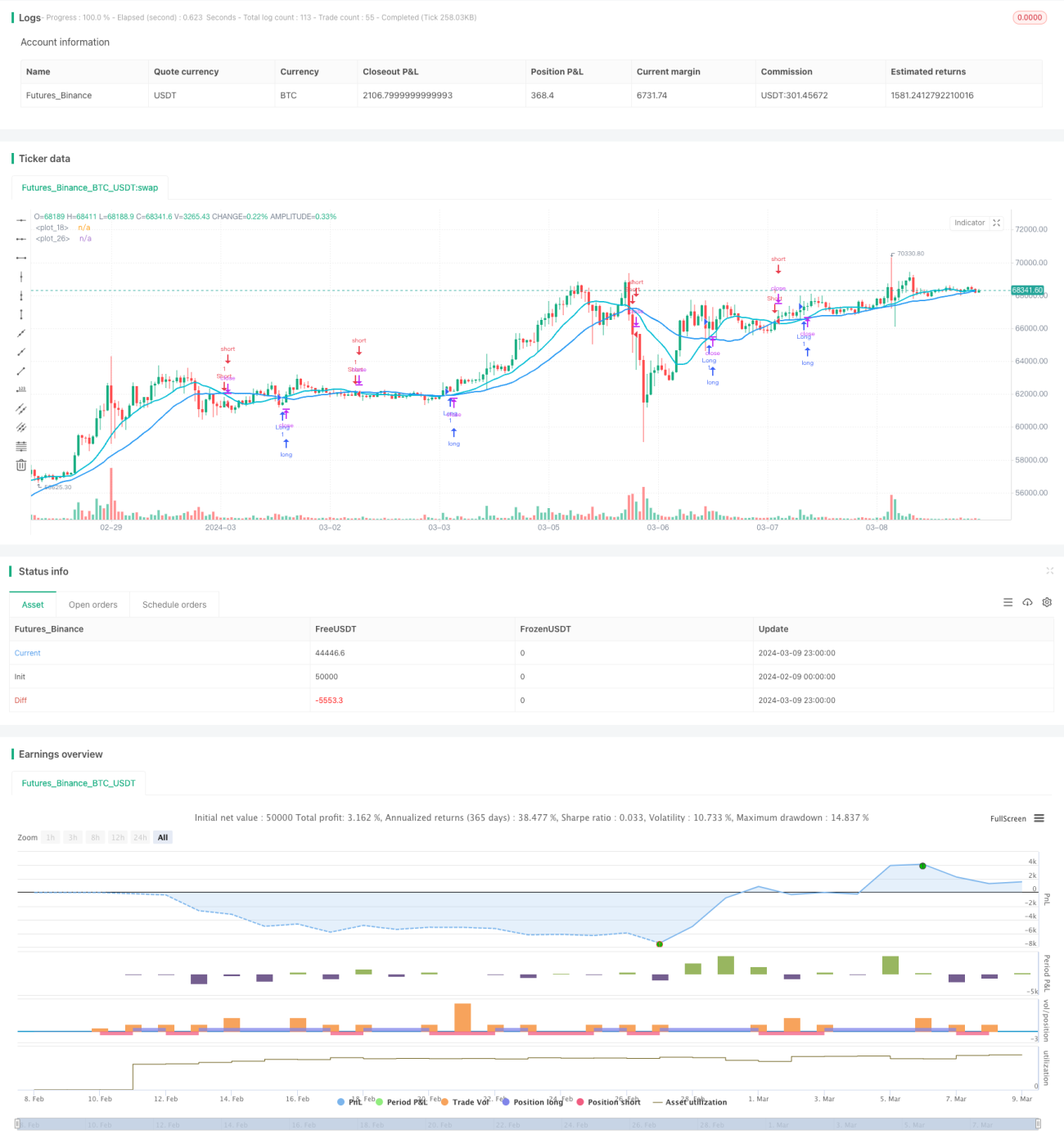

The Dual Moving Average Crossover Strategy is a classic trend-following strategy. This strategy uses two moving averages with different periods to capture market trends. When the fast moving average crosses above the slow moving average, it generates a long signal. When the fast moving average crosses below the slow moving average, it generates a short signal. The core idea of this strategy is that the fast moving average is more sensitive to price changes and can react more quickly to changes in market trends, while the slow moving average reflects the long-term trend of the market. By analyzing the crossover of the two moving averages, we can determine the turning point of the market trend and make trades accordingly.

Strategy Principle

In this strategy code, two moving averages are used: a fast moving average (default 14 periods) and a slow moving average (default 28 periods). The type of moving average can be selected from Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), and Relative Moving Average (RMA).

The main logic of the strategy is as follows:

- Calculate the values of the fast moving average and the slow moving average

- If the fast moving average crosses above the slow moving average, it generates a long signal and opens a long position

- If the fast moving average crosses below the slow moving average and shorting is allowed (allowShorting=true), it generates a short signal and opens a short position

- If the fast moving average crosses below the slow moving average and shorting is not allowed (allowShorting=false), it closes the long position

Through this logic, the strategy can track the main trend of the market, holding long positions in an uptrend and short positions or no positions in a downtrend. The moving average period and type can be adjusted and optimized according to different markets and trading instruments.

Strategy Advantages

- Simple and clear logic, easy to understand and implement

- Suitable for trending markets, can effectively capture medium and long-term market trends

- Adjustable parameters, suitable for different markets and trading instruments

- Can flexibly choose whether to allow shorting based on market characteristics and personal preferences

- Moving averages are classic technical analysis indicators that are widely used and validated

Strategy Risks

- In range-bound markets, frequent moving average crossovers may lead to frequent trading and increase transaction costs

- If the fast moving average is chosen too short or the slow moving average is chosen too long, it may cause signal lag and miss the best trading opportunities

- When the market trend reverses, the strategy may experience consecutive losses

- Fixed moving average period parameters may not adapt to dynamic changes in the market

To address these risks, the following measures can be taken:

- Optimize moving average period parameters based on market characteristics and choose appropriate lengths for fast and slow moving averages

- In range-bound markets, consider adding filtering conditions such as ATR filtering or moving average crossover angle filtering

- Set reasonable stop-loss and take-profit levels to control single trade risk

- Conduct regular backtesting and evaluation, and adjust strategy parameters according to market changes

Strategy Optimization

- Introduce more technical indicators such as MACD and RSI to build a multi-factor strategy and improve signal accuracy

- Optimize position management, such as considering factors like ATR or volatility to dynamically adjust position sizes

- For range-bound markets, consider introducing trend determination indicators such as ADX to avoid frequent trading

- Use machine learning or optimization algorithms to automatically find the optimal parameter combination

These optimizations can improve the adaptability and stability of the strategy to better adapt to different market conditions. However, it should also be noted that over-optimization may lead to overfitting of the strategy and poor performance in live trading. Further validation on out-of-sample data is needed.

Summary

The Dual Moving Average Crossover Strategy is a classic trend-following strategy that generates trading signals through the crossover of two moving averages with different periods. It has simple logic, is easy to implement, and is suitable for trending markets. However, in range-bound markets, it may experience frequent trading and consecutive losses. Therefore, when using this strategy, it is necessary to optimize the moving average period parameters based on market characteristics and set reasonable stop-loss and take-profit levels. In addition, the adaptability and stability of the strategy can be improved by introducing more technical indicators, optimizing position management, trend determination, etc. However, over-optimization may lead to overfitting and should be treated with caution. Overall, the Dual Moving Average Crossover Strategy is a classic strategy worth learning and researching. Through continuous optimization and improvement, it can become an effective trading tool.

- 1