Dynamic Stop Loss and Take Profit Strategy Based on Dual ATR Trailing Stop

Overview

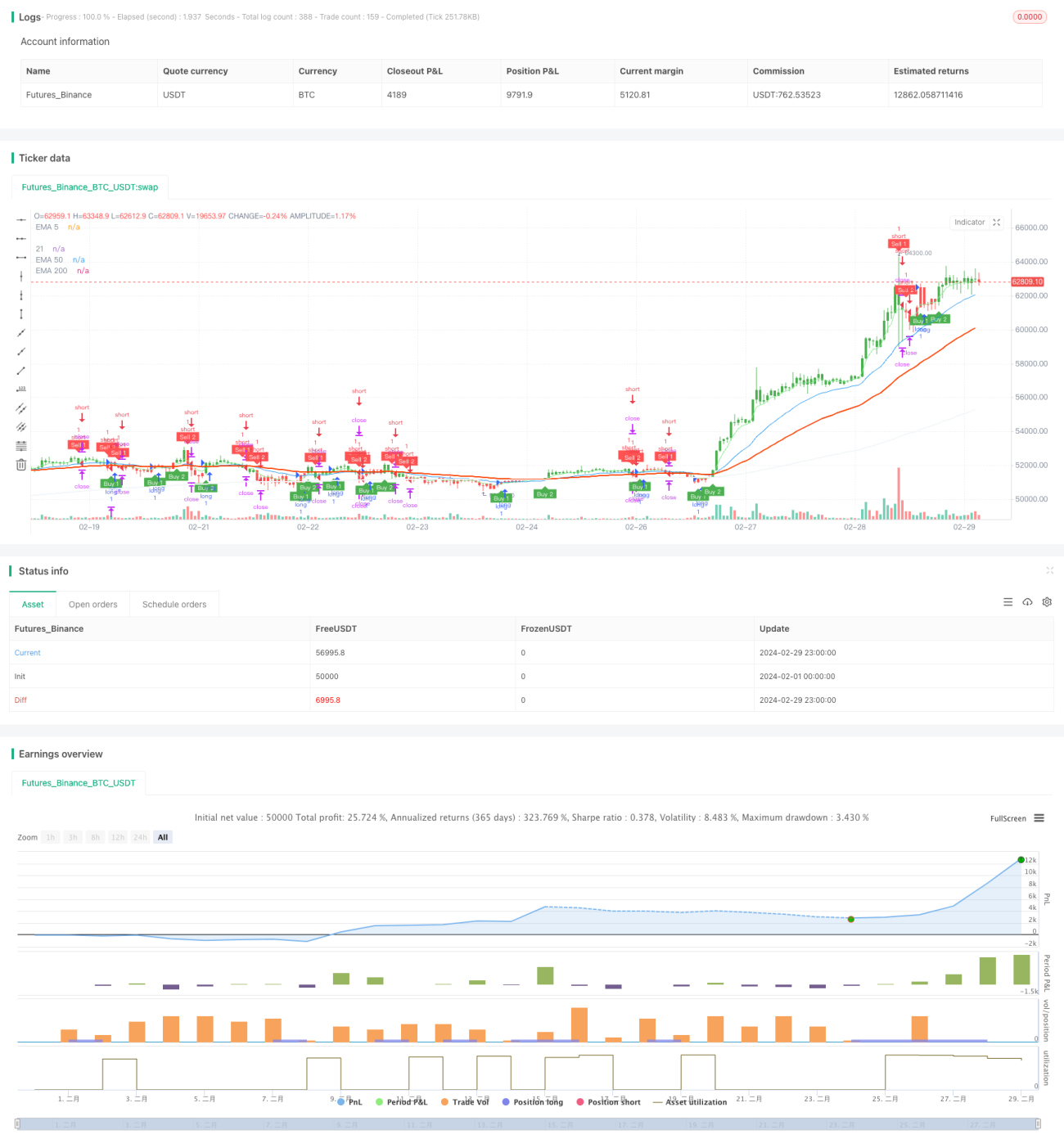

This strategy constructs dual dynamic trailing stop-loss lines using two Average True Range (ATR) indicators with different periods, generating trading signals when the price breaks through the stop-loss lines. It also dynamically sets the take-profit level based on the current candle body length to achieve dynamic stop-loss and take-profit. The strategy also incorporates EMA indicators to assist in judging the trend.

Strategy Principles

- Calculate the ATR indicator values for two different periods (default 10 and 20), then multiply them by their respective sensitivity coefficients (default 1 and 2) to obtain two stop-loss widths.

- Generate long or short signals based on the price position above or below the two stop-loss lines and the breakout situation.

- The take-profit level is dynamically calculated based on 1.65 times (adjustable) the current candle body length.

- After opening a position, if the price reaches the take-profit level, the position is closed to take profits.

- Use indicators such as EMA to assist in judging the current trend and provide reference for entry.

This strategy utilizes the characteristics of the ATR indicator to construct dual dynamic stop-losses, which can adapt well to different market volatilities and quickly respond to market changes. The dynamic take-profit setting allows the strategy to capture more profits in trending markets. Overall, the strategy performs well in trending markets but may experience frequent profit and loss offsets in range-bound markets.

Advantage Analysis

- The dual dynamic stop-loss lines can adapt to different market volatilities and have high flexibility.

- The take-profit level is dynamically calculated based on the current candle body length, allowing for more profits to be captured in trending markets.

- The use of EMA and other indicators to assist in trend judgment provides a reference for entry and enhances the reliability of the strategy.

- The code logic is clear and readable, making it easy to understand and optimize.

Risk Analysis

- In range-bound markets, frequent trading may lead to high transaction costs and affect profitability.

- The settings of stop-loss line parameters and take-profit multipliers need to be optimized according to different market and product characteristics; improper parameters may result in poor strategy performance.

- The strategy mainly relies on price breakouts of dynamic stop-loss lines to generate signals, which may produce false signals in some large fluctuation fake breakouts.

Optimization Directions

- For range-bound markets, consider introducing more indicators or conditions to filter trading signals, such as RSI and MACD.

- For different products and markets, historical backtesting and parameter optimization can be used to find the optimal stop-loss line parameters and take-profit multipliers.

- Consider introducing position management and risk control modules to dynamically adjust position size based on market volatility and account risk.

- Add more trend judgment indicators to improve the reliability and accuracy of signals.

Summary

This strategy, with its design of dual dynamic stop-loss lines and dynamic take-profit, can adapt well to different market environments and perform well in trending markets. However, in range-bound markets, it may face the problem of frequent trading and profit and loss offsets. Therefore, this strategy is more suitable for use in trending markets and needs to be optimized and adjusted based on product characteristics and market conditions. Moreover, there is still room for further optimization, such as introducing more filtering conditions, position management, and risk control modules to improve the robustness and profitability of the strategy. Overall, the strategy has a clear idea, simple and easy-to-understand logic, and has certain practical value and room for optimization, which is worthy of further research and application.

- 1