Kuberan Strategy: The Confluence Approach for Market Mastery

Strategy Overview

The Kuberan strategy is a powerful trading strategy developed by Kathir. It combines multiple analytical techniques to form a unique and potent trading approach. Named after the god of wealth, Kuberan, the strategy symbolizes its goal of enriching traders' portfolios.

Kuberan is more than just a strategy; it is a comprehensive trading system. It integrates trend analysis, momentum indicators, and volume metrics to identify high-probability trading opportunities. By leveraging the synergy of these elements, Kuberan provides clear entry and exit signals, suitable for traders of all levels.

Strategy Principles

At the core of the Kuberan strategy is the principle of multi-indicator confluence. It utilizes a unique combination of indicators that work in harmony to reduce noise and false signals. Specifically, the strategy employs the following key components:

- Trend direction determination: By comparing current prices with support and resistance levels, it determines the prevailing trend direction.

- Support and resistance levels: Identifies key support and resistance levels using the zigzag indicator and pivot points.

- Divergence detection: Compares price action with momentum indicators to spot potential trend reversals signaled by divergences.

- Volatility adaptation: Dynamically adjusts stop-loss levels based on the ATR indicator to adapt to varying market volatility.

- Candlestick pattern recognition: Confirms trend and reversal signals using specific candlestick combinations.

By comprehensively considering these factors, the Kuberan strategy can adaptively adjust to various market conditions and capture high-probability trading opportunities.

Strategy Advantages

- Multi-indicator confluence: Kuberan leverages the synergy of multiple indicators, greatly enhancing signal reliability and reducing noise interference.

- High adaptability: Through dynamic parameter adjustments, the strategy can adapt to changing market environments, avoiding obsolescence.

- Clear signals: Kuberan provides clear entry and exit signals, simplifying the trading decision process.

- Robust backtesting: The strategy has undergone rigorous historical backtesting, demonstrating consistent performance across various market scenarios.

- Wide applicability: Kuberan is applicable to multiple markets and instruments, not limited to specific trading vehicles.

Strategy Risks

- Parameter sensitivity: The performance of the Kuberan strategy is sensitive to parameter selection; inappropriate parameters may lead to suboptimal results.

- Black swan events: The strategy primarily relies on technical signals and has limited ability to handle fundamental black swan events.

- Overfitting risk: If too much historical data is considered during parameter optimization, the strategy may become overly fitted to the past, reducing its adaptability to future market conditions.

- Leverage risk: Using excessive leverage poses the risk of margin calls during significant drawdowns.

To mitigate these risks, appropriate control measures can be implemented, such as periodic parameter adjustments, setting reasonable stop-losses, moderating leverage, and monitoring fundamental changes.

Optimization Directions

- Machine learning optimization: Introduce machine learning algorithms to dynamically optimize strategy parameters and enhance adaptability.

- Incorporation of fundamental factors: Consider integrating fundamental analysis into trading decisions to handle situations where technical signals fail.

- Portfolio management: At the capital management level, include the Kuberan strategy in a diversified portfolio to achieve effective hedging with other strategies.

- Market-specific optimization: Customize strategy parameters based on the characteristics of different markets and instruments.

- High-frequency transformation: Adapt the strategy into a high-frequency trading version to capture more short-term trading opportunities.

Conclusion

Kuberan is a powerful and reliable trading strategy that ingeniously combines multiple technical analysis methods. Through the principle of indicator confluence, it excels in capturing trends and identifying turning points. While no strategy is immune to risks, Kuberan has proven its robustness in backtesting. With appropriate risk control measures and optimization efforts, this strategy can help traders gain an edge in market battles, driving long-term, steady growth of their investment portfolios.

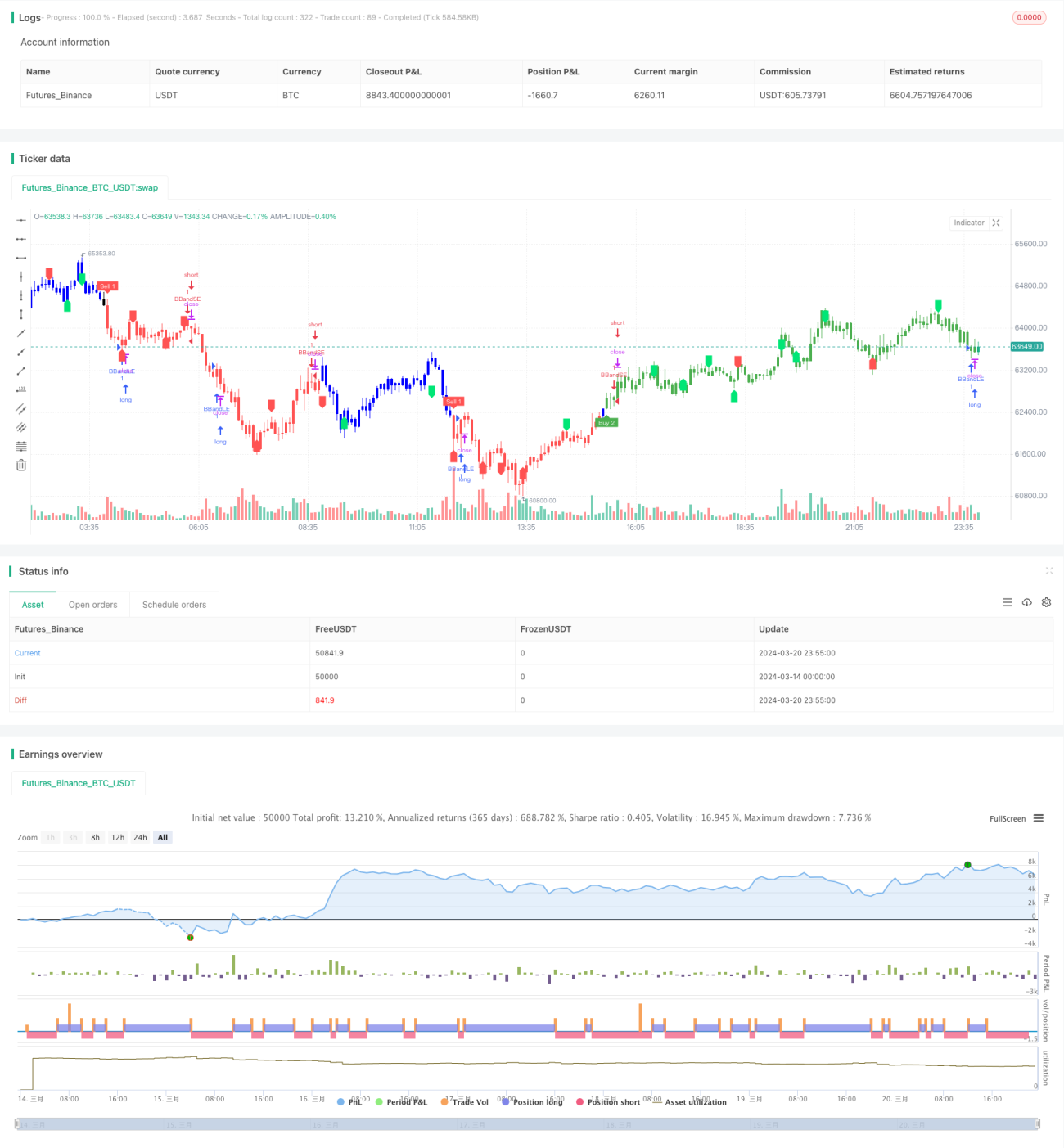

/*backtest

start: 2024-03-14 00:00:00

end: 2024-03-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue- 1