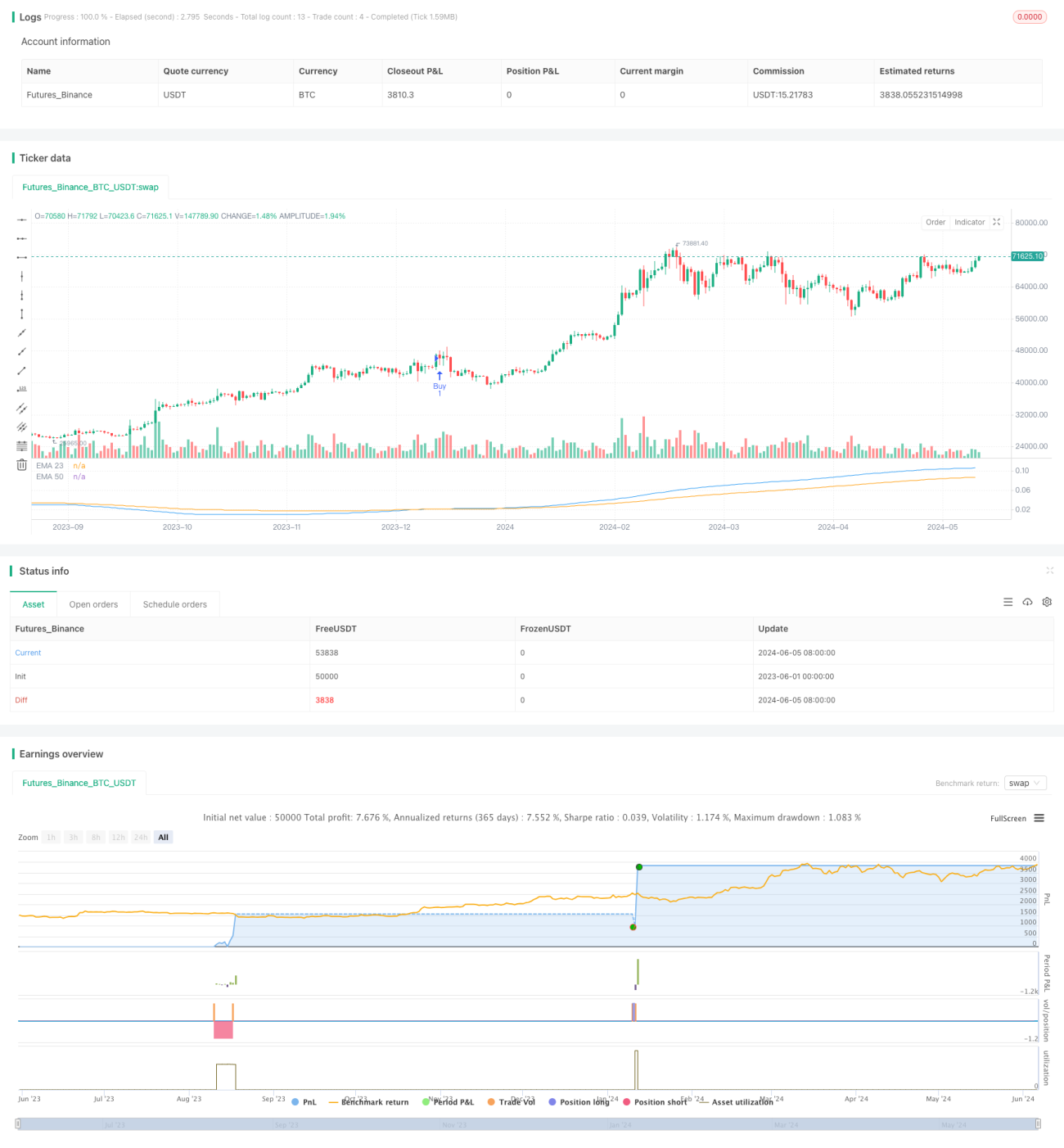

This strategy generates trading signals based on the Chaikin Money Flow (CMF)

CASHISKING | CASHISKING

CMF, EMA, SMA

Overview

This strategy generates trading signals based on the Chaikin Money Flow (CMF) indicator and Exponential Moving Averages (EMA). It first calculates the CMF values for a specified period, then uses two EMAs with different periods to smooth the CMF data. A buy signal is generated when the fast EMA crosses above the slow EMA, while a sell signal is generated when the fast EMA crosses below the slow EMA. The strategy also sets stop-loss and take-profit conditions to manage risk and lock in profits.

Strategy Principles

- Calculate the Chaikin Money Flow (CMF) values for a specified period. CMF incorporates both price and volume data to measure the strength of money flow into and out of the market.

- Apply two Exponential Moving Averages (EMAs) with different periods to smooth the CMF data. The fast EMA captures short-term trends, while the slow EMA identifies long-term trends.

- Generate a buy signal when the fast EMA crosses above the slow EMA, and a sell signal when the fast EMA crosses below the slow EMA.

- After a trading signal is generated, the strategy waits for confirmation from two candles to avoid false signals.

- Set stop-loss and take-profit conditions. The stop-loss price is a certain percentage of the entry price, while the take-profit price is a certain percentage of the entry price.

Advantage Analysis

- Combines price and volume data: The CMF indicator comprehensively considers both price and volume data, providing a more reliable reflection of market money flow and generating more accurate trading signals.

- Trend tracking: By utilizing EMAs with different periods, the strategy can capture both short-term and long-term trends, adapting to various market environments.

- Signal confirmation: After a trading signal is generated, the strategy waits for confirmation from two candles, effectively filtering out some false signals and improving the success rate of trades.

- Risk management: The strategy incorporates stop-loss and take-profit conditions, which effectively controls the risk of individual trades while securing obtained profits.

Risk Analysis

- Parameter optimization: The performance of the strategy depends on the selection of CMF and EMA periods. Different market environments may require different parameter settings, necessitating periodic parameter optimization.

- Trend recognition: In choppy markets or at trend turning points, the strategy may generate more false signals, leading to frequent trades and capital losses.

- Slippage and trading costs: Frequent trading may increase slippage and trading costs, affecting the overall profitability of the strategy.

Optimization Directions

- Dynamic parameter adjustment: Dynamically adjust the CMF and EMA period parameters based on changes in market conditions to adapt to different market states.

- Incorporate other indicators: Combine other technical indicators, such as the Relative Strength Index (RSI) and Average True Range (ATR), to improve the accuracy of trend recognition and the reliability of signals.

- Optimize stop-loss and take-profit: Dynamically adjust the stop-loss and take-profit percentages based on market volatility and risk preferences to better manage risk and lock in profits.

- Implement position sizing: Dynamically adjust position sizes based on market trends and signal strength. Increase position sizes when trends are clear and reduce position sizes during uncertain periods.

Summary

This strategy utilizes the Chaikin Money Flow indicator and Exponential Moving Averages, combining price and volume data with a primary focus on trend tracking. It also sets stop-loss and take-profit conditions to manage risk. The strategy's advantages lie in its ability to comprehensively consider multiple factors and capture trends on different time scales. However, there is still room for optimization in parameter settings and trend recognition. In the future, the strategy's stability and profitability can be further improved through dynamic parameter adjustment, incorporation of other indicators, optimization of stop-loss and take-profit, and implementation of position sizing.

- 1