Multi-Level RSI Mean Reversion Strategy with Dynamic Volatility Adjustment

Overview

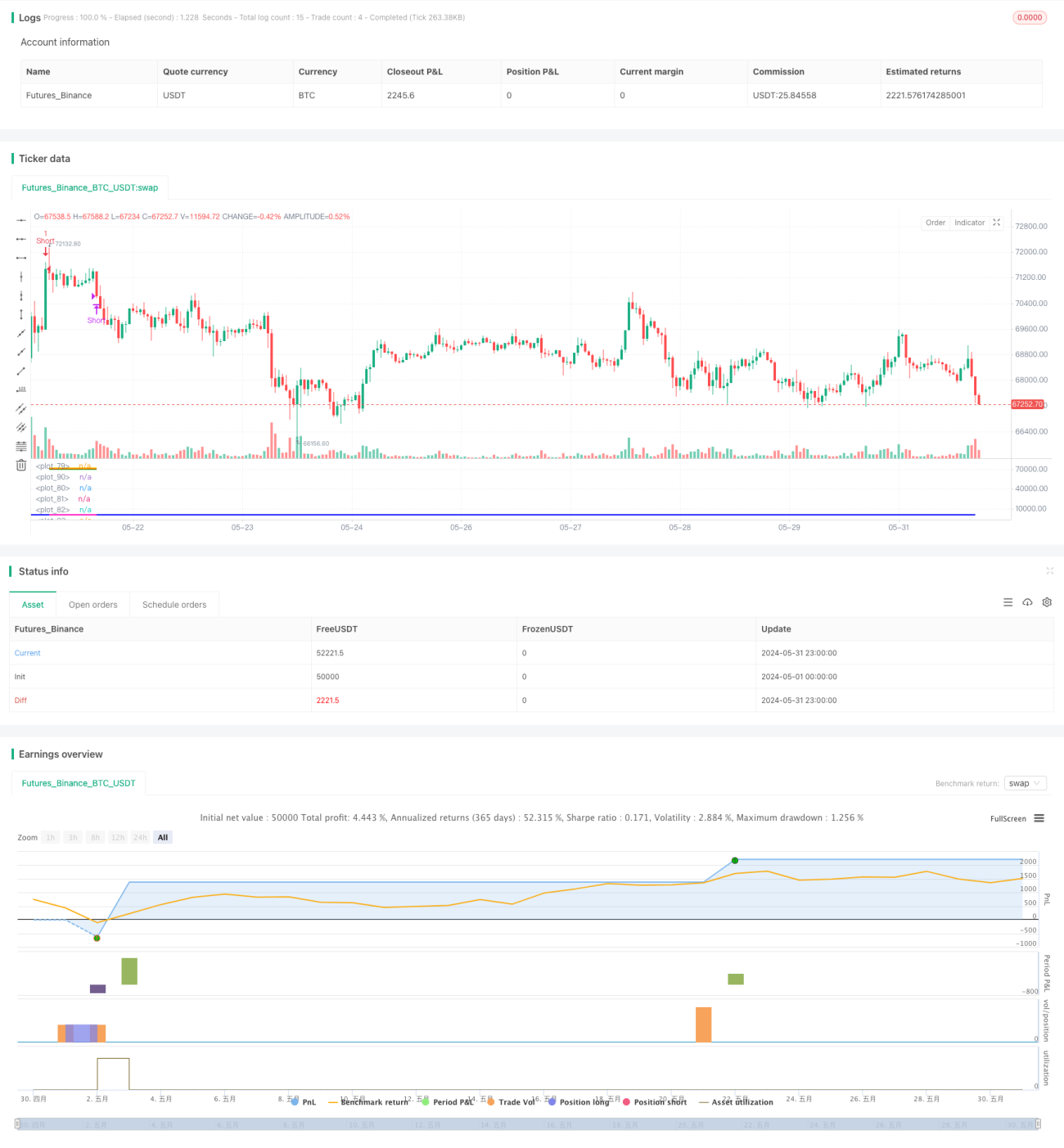

This strategy is a multi-level mean reversion trading system based on the RSI indicator and price volatility. It uses extreme RSI values and abnormally large price fluctuations as entry signals, while employing pyramid-style position scaling and dynamic take-profit levels to manage risk and optimize returns. The core idea of this strategy is to enter the market during extreme volatility and profit when prices return to normal levels.

Strategy Principles

-

Entry Conditions:

- Uses 20-period RSI (RSI20) as the main indicator

- Sets multiple RSI thresholds (35/65, 30/70, 25/75, 20/80) with corresponding volatility thresholds

- Triggers entry signal when RSI reaches a threshold and current candle body size exceeds the corresponding volatility threshold

- Additional condition: price must break through the recent high/low support level by a certain percentage

-

Position Scaling Mechanism:

- Allows up to 5 entries (initial entry + 4 additional entries)

- Each additional entry requires meeting stricter RSI and volatility conditions

-

Exit Mechanism:

- Sets 5 different levels of take-profit points

- Take-profit points are dynamically calculated based on support/resistance levels at entry

- Take-profit targets gradually decrease as the number of open positions increases

-

Risk Control:

- Uses a percentage risk model, with each trade risking a fixed 20% of the account value

- Sets a maximum allowed simultaneous open positions to 5, limiting overall risk exposure

Strategy Advantages

-

Multi-level Entry: By setting multiple RSI and volatility thresholds, the strategy can capture different degrees of market extremes, increasing trading opportunities.

-

Dynamic Take-Profit: Take-profit points calculated based on support/resistance levels can self-adapt to market structure, protecting profits without exiting too early.

-

Pyramid-style Position Scaling: Increasing positions as trends continue can significantly enhance profit potential.

-

Risk Management: Fixed percentage risk and maximum position limits effectively control risk for each trade and overall.

-

Flexibility: Numerous adjustable parameters allow the strategy to adapt to different market environments and trading instruments.

-

Mean Reversion + Trend Following: Combines advantages of mean reversion and trend following, capturing short-term reversals without missing major trends.

Strategy Risks

-

Overtrading: May trigger frequent trade signals in highly volatile markets, leading to excessive fees.

-

False Breakouts: Markets may experience brief extreme volatility followed by quick reversals, causing false signals.

-

Consecutive Losses: Continuous unidirectional market movements may result in significant losses after multiple position increases.

-

Parameter Sensitivity: Strategy performance may be highly sensitive to parameter settings, risking overfitting.

-

Slippage Impact: May face severe slippage during periods of intense volatility, affecting strategy performance.

-

Market Environment Dependence: Strategy may underperform in certain market environments, such as low volatility or strong trend markets.

Strategy Optimization Directions

-

Dynamic Parameter Adjustment: Introduce adaptive mechanisms to dynamically adjust RSI and volatility thresholds based on market conditions.

-

Multi-timeframe Analysis: Incorporate longer-term market trend judgments to improve entry quality.

-

Stop-Loss Optimization: Add trailing stop-losses or ATR-based dynamic stop-losses for further risk control.

-

Market State Filtering: Include trend strength, volatility cycle, and other filtering conditions to avoid trading in unsuitable market environments.

-

Capital Management Optimization: Implement more detailed position management, such as adjusting trade size based on different signal levels.

-

Machine Learning Integration: Utilize machine learning algorithms to optimize parameter selection and signal generation processes.

-

Correlation Analysis: Incorporate correlation analysis with other assets to improve strategy stability and diversity.

Conclusion

This multi-level RSI mean reversion trading strategy is a carefully designed quantitative trading system that cleverly combines technical analysis, dynamic risk management, and pyramid-style position scaling techniques. By capturing extreme market volatility and profiting when prices revert, the strategy demonstrates strong profit potential. However, it also faces challenges such as overtrading and market environment dependence. Future optimization should focus on improving the strategy's adaptability and risk control capabilities to suit different market environments. Overall, this is a strategy framework with a solid foundation that, through further optimization and backtesting, has the potential to develop into a robust trading system.

- 1