Triple EMA Pullback Scalping Strategy

25/50/100 EMA Triple Filter - Real Trend Pullback Trading

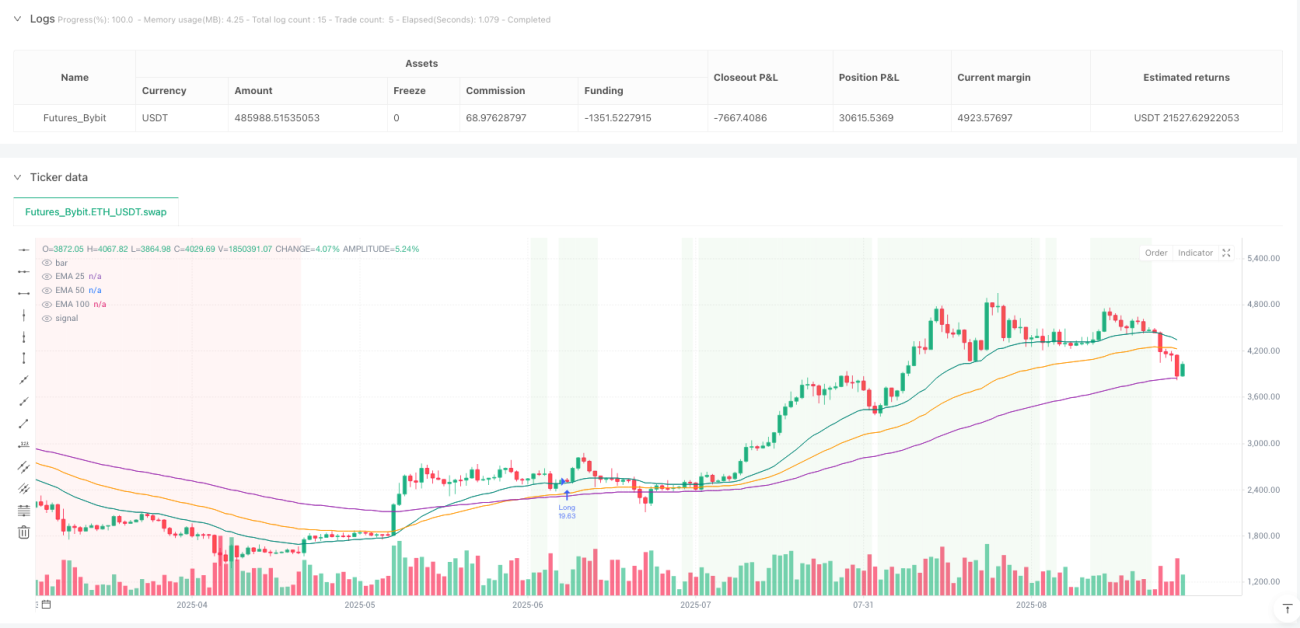

Stop using single moving averages for trading. This strategy builds a complete trend identification system with 25/50/100 EMAs, requiring proper EMA sequence and same-direction slopes, plus 0.10×ATR minimum spacing requirement. Data shows this triple filtering mechanism effectively avoids false breakouts in choppy markets, only entering during genuine trending conditions.

The key is "clean EMA alignment": bullish when 25>50>100 with all sloping up, bearish when 25<50<100 with all sloping down. Spacing filter ensures sufficient trend strength, avoiding ineffective signals during EMA convergence states.

Precise Pullback Logic with 15-Period Reversal Confirmation

The strategy's core is the pullback detection mechanism. Bullish pullbacks require price touching 25 or 50 EMA while staying above 100 EMA, bearish pullbacks require touching 25 or 50 EMA while staying below 100 EMA. This design is more precise than traditional "buy the dip after support break" approaches.

The 15-period pullback window is well-calibrated. Backtest data indicates genuine trend pullbacks typically complete reversal within 10-15 periods. Pullbacks exceeding this timeframe often signal potential trend changes. Strategy immediately disarms when timeout occurs or price breaches 100 EMA.

Strict Entry Confirmation - Entire Candle Must Clear 25 EMA

Entry trigger conditions are extremely rigorous: after confirmed bar close, the entire candle (open, high, low, close) must be completely on the correct side of 25 EMA. This design eliminates false breakouts and intraday noise, ensuring entries only after genuine reversal confirmation.

Long entry requirements: open>25EMA, low>25EMA, close>25EMA. Short entry requirements: open<25EMA, high<25EMA, close<25EMA. This "whole candle confirmation" method significantly improves entry quality and reduces ineffective trades.

10% Position + 0.05% Commission - Optimized for High-Frequency Scalping

The default 10% position sizing strikes a balance between sufficient returns and controlled single-trade risk. 0.05% commission setting reflects realistic trading costs, making backtest results more reliable. Supports both directional and bidirectional trading to adapt to different market environments.

Important reminder: Strategy includes entry logic only, no take-profit/stop-loss. Live trading requires strict risk management - recommend 2-3×ATR stops and 1.5-2× risk-reward ratio targets.

Clear Use Cases - Excels in Trending Markets, Caution in Choppy Conditions

Strategy performs excellently in clear trending markets, particularly suitable for buying pullbacks in directional moves. However, in sideways choppy markets, EMA alignment conditions are rarely met, resulting in fewer trading opportunities. This is actually a strength, avoiding overtrading in unfavorable environments.

Risk warning: Historical backtests don't guarantee future returns, strategy carries consecutive loss risks. Choppy markets may produce extended no-signal periods requiring patient waiting for suitable market conditions. Recommend thorough paper trading validation before live implementation.

/*backtest

start: 2025-01-01 00:00:00

end: 2025-09-27 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Bybit","currency":"ETH_USDT","balance":500000}]

*/

//@version=6

strategy("Clean 25/50/100 EMA Pullback Scalper — Entries Only (Side Select)",

overlay=true, calc_on_every_tick=true, calc_on_order_fills=true,

initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.05,- 1