Black-Scholes Gamma Scalping Strategy: Quantitative Wisdom from Options Market Makers

BS, GAMMA, DELTA, THETA, VEGA

Why Do Options Market Makers Always Profit from Volatility?

In the world of quantitative trading, there's a seemingly paradoxical phenomenon: while retail investors become anxious due to market volatility, options market makers manage to profit consistently. What's the secret behind this? The answer lies in the Black-Scholes-based gamma scalping strategy we're analyzing today.

The core concept of this strategy is to simulate options market makers' trading behavior: by constructing synthetic long straddle positions, utilizing gamma effects for dynamic hedging, and thus capturing profits through volatility arbitrage. Simply put, it's about making mathematics work for us rather than fighting market emotions.

Mathematical Foundation: Practical Application of the Black-Scholes Model

The Black-Scholes model isn't just academic theory—it's the cornerstone of modern options pricing. In this strategy, we focus on five Greek letters:

Delta (Δ): Measures option price sensitivity to underlying asset price changes. For straddle positions, Delta changes provide hedging signals.

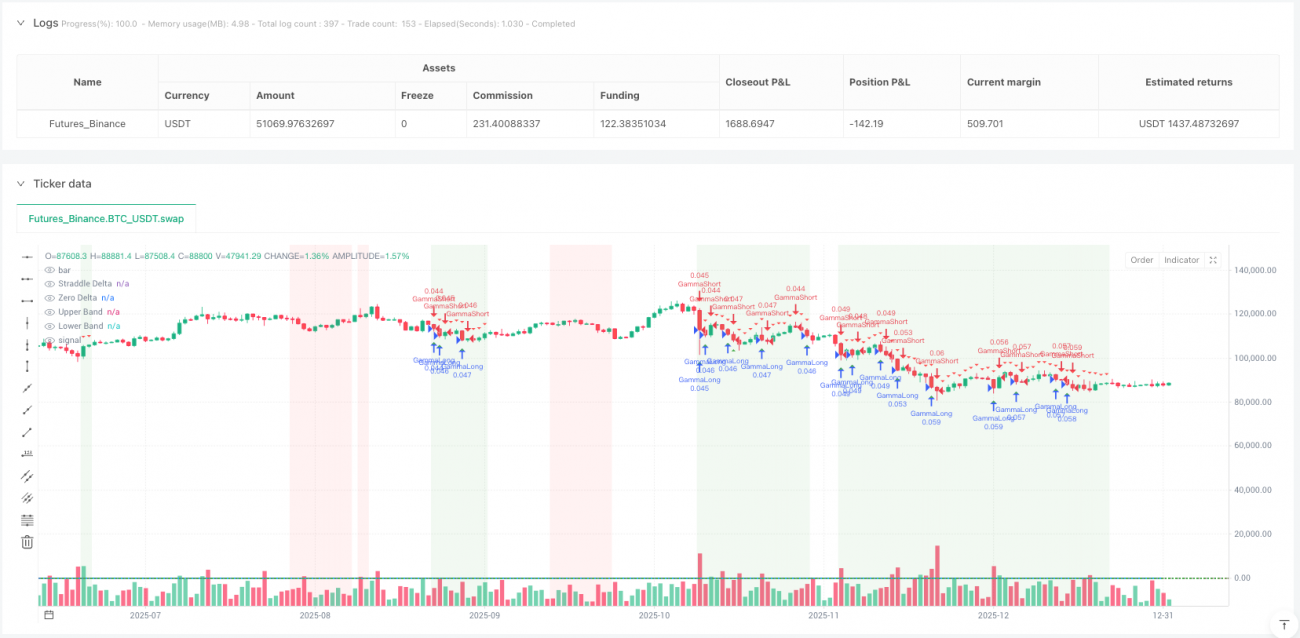

Gamma (Γ): The rate of Delta change, which is the strategy's core. Positive gamma means Delta increases when prices rise and decreases when prices fall, creating "buy low, sell high" opportunities.

Theta (Θ): Time decay, representing the cost we need to overcome. Gamma trading profits can only cover time decay when realized volatility exceeds implied volatility.

Vega (ν): Sensitivity to volatility, helping us assess the volatility environment.

From the code implementation perspective, the strategy uses standard Black-Scholes formulas to calculate these Greeks, employing standard normal distribution functions (using Abramowitz & Stegun approximation) to ensure computational accuracy.

How to Identify Optimal Trading Opportunities?

The strategy employs a three-layer signal filtering mechanism:

Layer 1: Volatility Regime Identification

By comparing the ratio of historical volatility to implied volatility to determine the current volatility environment. When Historical Volatility/Implied Volatility > 1.2, it indicates actual market volatility exceeds options pricing expectations—an ideal environment for gamma scalping.

Layer 2: Gamma Scalping Trigger

Trading signals are triggered when price movements exceed specific ATR multiples. This design is clever: it ensures we only execute hedging trades when there's sufficient price movement, avoiding overtrading.

Layer 3: Delta Hedge Bands

Hedging signals are generated when the net Delta of the straddle position deviates from neutral beyond set thresholds. This simulates market makers' behavior of maintaining Delta neutrality.

When Is This Strategy Most Effective?

Based on strategy logic analysis, optimal use cases include:

-

High Volatility Environments: When market realized volatility consistently exceeds implied volatility, gamma trading can generate excess returns.

-

Pullbacks in Trending Markets: Short-term retracements in strong trends often create excellent gamma scalping opportunities.

-

Event-Driven Volatility: Volatility changes around earnings, central bank decisions, and other events provide ideal trading environments for the strategy.

Note that the strategy has limited effectiveness in low-volatility consolidating markets, as price movements are insufficient to trigger effective gamma trading signals.

Sophisticated Risk Management Design

This strategy's risk management reflects professional quantitative trading standards:

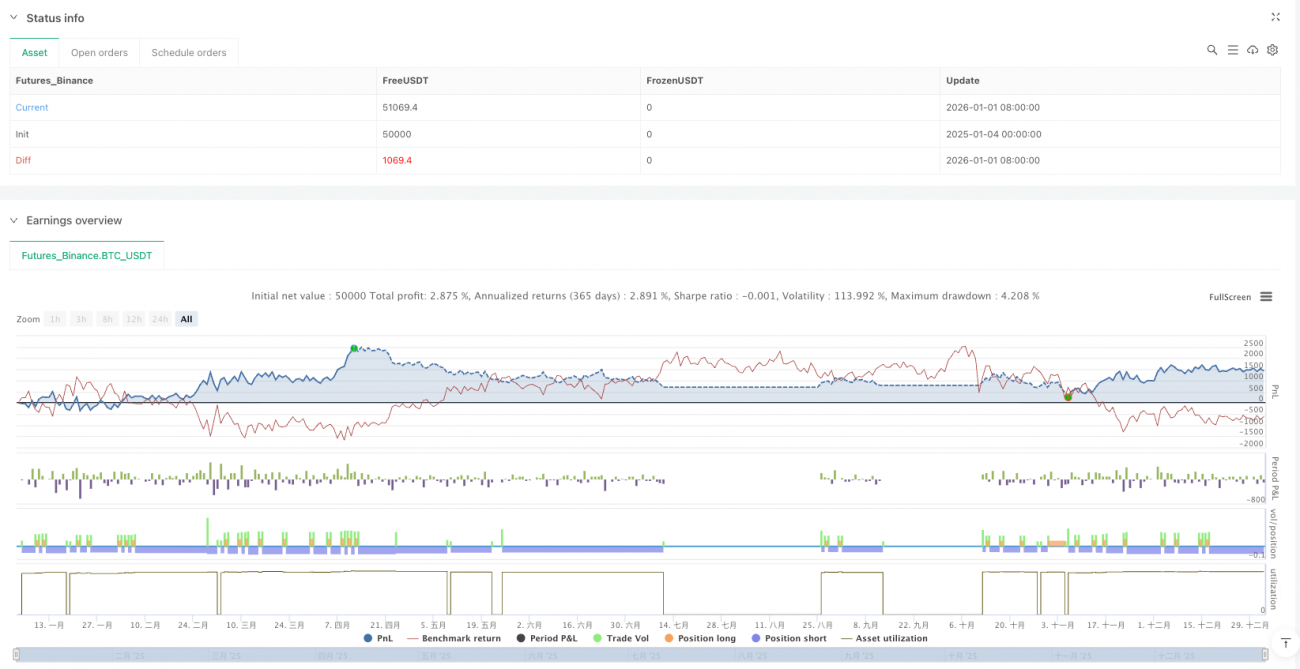

Dynamic Position Sizing: Adjusting position sizes based on volatility—reducing positions during high volatility and increasing them during low volatility, contrasting sharply with traditional fixed position management.

Multi-Layer Stop Mechanisms: Combining ATR-multiple stops, maximum drawdown protection, and time-value-based exit mechanisms.

Concurrent Position Limits: Controlling overall risk exposure by limiting maximum simultaneous positions.

Strategy Innovation and Limitations

Innovative Aspects:

- Complete migration of complex options Greeks calculations to stock/futures trading

- Dynamic volatility regime identification rather than static parameters

- Multi-dimensional signal confirmation mechanisms reducing false signals

Potential Limitations:

- Sensitivity to trading costs, requiring low commission environments

- Black-Scholes model assumptions may fail under extreme market conditions

- High strategy complexity requiring thorough backtesting validation

Practical Recommendations and Optimization Directions

Based on in-depth code analysis, I recommend:

- Parameter Optimization: Dynamically adjusting volatility thresholds and hedge band widths for different market environments

- Multi-Timeframe Confirmation: Incorporating longer-term volatility trends for signal filtering

- Cost Control: Strictly controlling slippage and commissions in live trading, as these directly impact strategy profitability

This strategy showcases the charm of quantitative trading: using mathematical models to simplify complex market behaviors into executable trading rules. While it cannot guarantee every trade will be profitable, from a long-term perspective, it provides us with a positive expected value trading framework.

For quantitative traders seeking to understand the essence of options trading, this strategy is undoubtedly an excellent learning case. It not only demonstrates how to transform theory into practice but, more importantly, reveals how professional traders think about markets: not predicting direction, but managing risk and letting probability work for us.

- 1