গতিশীল দ্বৈত সুপারট্রেন্ড ভলিউম-মূল্য কৌশল

সারসংক্ষেপ

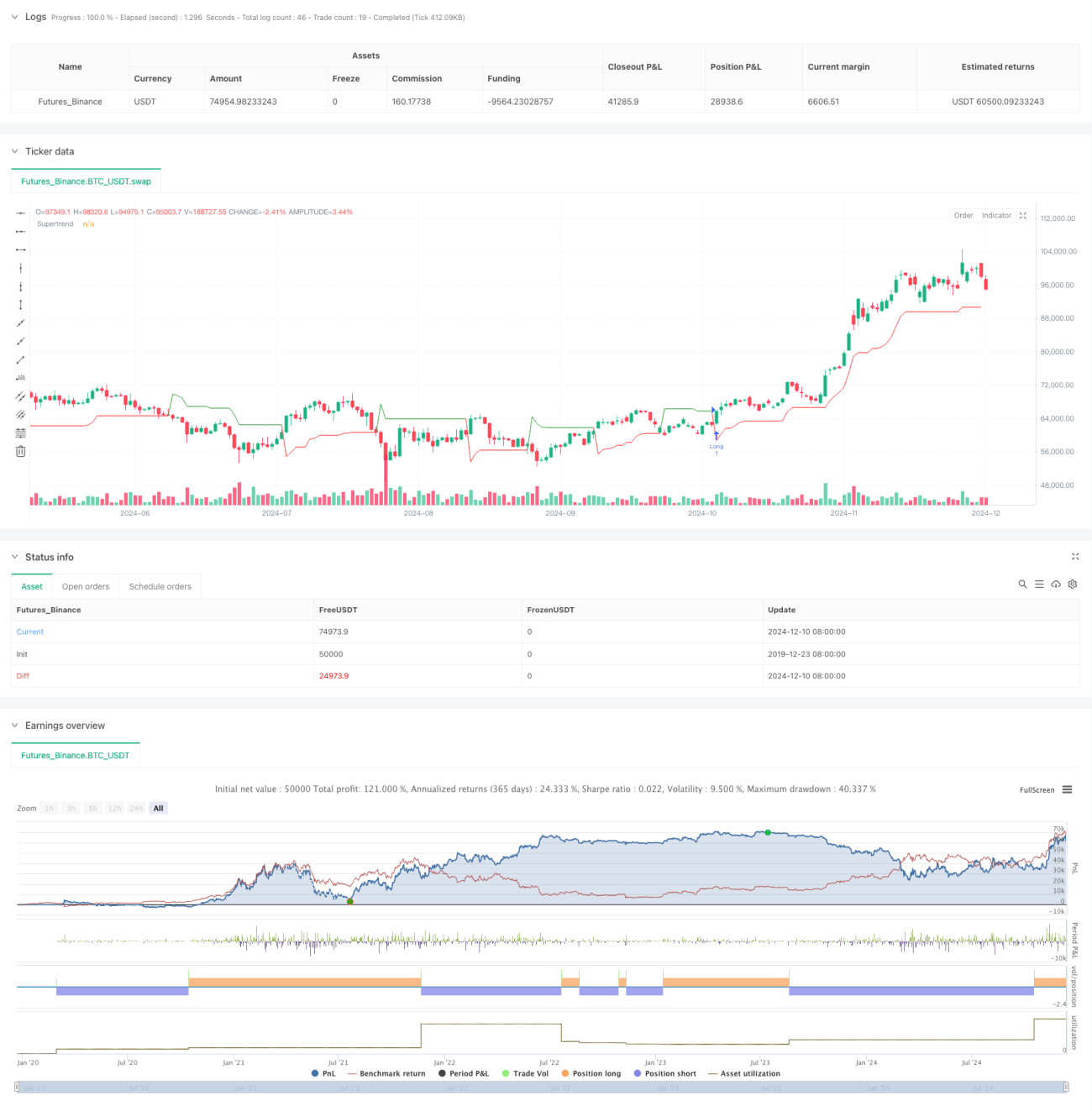

এটি একটি উন্নত কোয়ান্টিটেটিভ ট্রেডিং কৌশল যা সুপারট্রেন্ড নির্দেশক এবং ভলিউম বিশ্লেষণকে একত্রিত করে। এই কৌশলটি মূল্যের গতিশীল পর্যবেক্ষণ, সুপারট্রেন্ড লাইনের ক্রসওভার এবং ভলিউমের অস্বাভাবিক আচরণের মাধ্যমে সম্ভাব্য ট্রেন্ড টার্নিং পয়েন্ট চিহ্নিত করে। কৌশলটি ট্রু রেঞ্জ (ATR) ভিত্তিক ডায়নামিক স্টপ-লস এবং টেক-প্রফিট সেটিংস ব্যবহার করে, যা উভয়ই ট্রেডিংয়ের নমনীয়তা এবং ঝুঁকি নিয়ন্ত্রণের নির্ভরযোগ্যতা নিশ্চিত করে।

কৌশলের নীতি

কৌশলের মূল যুক্তি নিম্নলিখিত মূল উপাদানগুলোর উপর ভিত্তি করে:

- প্রধান ট্রেন্ড নির্ধারণের সরঞ্জাম হিসেবে সুপারট্রেন্ড নির্দেশক ব্যবহার করা হয়, যা ATR ভিত্তিক গণনা করে এবং বাজারের ওঠানামার সাথে গতিশীলভাবে খাপ খাইয়ে নিতে পারে।

- ২০-পিরিয়ডের মুভিং এভারেজ ভলিউমকে বেসলাইন হিসেবে ধরে ১.৫ গুণের থ্রেশহোল্ড নির্ধারণ করা হয় ভলিউমের অস্বাভাবিকতা বিচারের জন্য।

- যখন মূল্য সুপারট্রেন্ড লাইন ভেঙে যায় এবং ভলিউম অস্বাভাবিক অবস্থা পূরণ করে, তখন ট্রেড সংকেত ট্রিগার হয়।

- ATR ভিত্তিক ডায়নামিক স্টপ-লস (১.৫ গুণ ATR) এবং টেক-প্রফিট (৩ গুণ ATR) সেটিংস ব্যবহার করে ঝুঁকি-পুরস্কার অনুপাত অনুকূলিত করা হয়।

কৌশলের সুবিধা

- উচ্চ সংকেত নির্ভরযোগ্যতা: ট্রেন্ড এবং ভলিউমের দুটি মাত্রার নিশ্চিতকরণ মিথ্যা সংকেতের সম্ভাবনা অনেক কমিয়ে দেয়।

- সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা: ডায়নামিক স্টপ-লস এবং টেক-প্রফিট সেটিংস বাজারের ওঠানামার সাথে স্বয়ংক্রিয়ভাবে ঝুঁকির প্যারামিটার সামঞ্জস্য করতে পারে।

- উচ্চ অভিযোজনযোগ্যতা: কৌশলের প্যারামিটারগুলি বিভিন্ন বাজার পরিবেশ এবং ট্রেডিং পণ্যের সাথে নমনীয়ভাবে সমন্বয় করা যায়।

- স্পষ্ট বাস্তবায়ন: ট্রেডিংয়ের নিয়ম স্পষ্ট, ব্যক্তিগত বিচারের কোনো উপাদান নেই, যা স্বয়ংক্রিয় ট্রেডিংয়ের জন্য উপযুক্ত।

কৌশলের ঝুঁকি

- রেঞ্জ-বাউন্ড মার্কেটের ঝুঁকি: সাইডওয়েজ বা রেঞ্জবাউন্ড অবস্থায় ঘন ঘন মিথ্যা সংকেত দেখা দিতে পারে।

- স্লিপেজ ঝুঁকি: অস্বাভাবিক ভলিউমের সময়ে বড় স্লিপেজ ক্ষতির সম্মুখীন হতে পারে।

- প্যারামিটার সংবেদনশীলতা: কৌশলের ফলাফল প্যারামিটার সেটিংসের প্রতি সংবেদনশীল, তাই ক্রমাগত অপ্টিমাইজেশন প্রয়োজন।

- পদ্ধতিগত ঝুঁকি: বাজার তীব্র ওঠানামার সময় স্টপ-লস সেটিংস অকার্যকর হতে পারে।

কৌশলের অপ্টিমাইজেশন দিকনির্দেশনা

- ট্রেন্ড শক্তি ফিল্টার যুক্ত করা: ট্রেন্ড শক্তি নির্ধারণের জন্য ADX নির্দেশক যোগ করা যেতে পারে, শুধুমাত্র শক্তিশালী ট্রেন্ডের সময় পজিশন খোলা।

- ভলিউম নির্দেশক অপ্টিমাইজেশন: সাধারণ গুণকের পরিবর্তে আপেক্ষিক ভলিউম পরিবর্তনের হার (ROC) বিবেচনা করা যেতে পারে।

- স্টপ-লস মেকানিজম উন্নয়ন: ট্রেলিং স্টপ-লস ফিচার যুক্ত করে লাভ লক করতে সাহায্য করে।

- সময় ফিল্টার যুক্ত করা: ট্রেডিংয়ের সময়সীমা নির্ধারণ করে উচ্চ অস্থিরতার সময় এড়ানো যায়।

সারসংক্ষেপ

এই কৌশলটি সুপারট্রেন্ড নির্দেশককে ভলিউম বিশ্লেষণের সাথে একত্রিত করে একটি নির্ভরযোগ্য এবং অভিযোজনযোগ্য ট্রেডিং সিস্টেম তৈরি করে। কৌশলটির শক্তি হলো সংকেত নিশ্চিতকরণের বহুমাত্রিকতা এবং ঝুঁকি ব্যবস্থাপনার গতিশীলতা, তবে বাজার পরিবেশের প্রভাব সম্পর্কে সতর্ক থাকা প্রয়োজন। ক্রমাগত অপ্টিমাইজেশন এবং উন্নয়নের মাধ্যমে, এই কৌশলটি বিভিন্ন বাজার পরিবেশে স্থিতিশীল পারফরম্যান্স বজায় রাখতে সক্ষম হতে পারে।

- 1