সংক্ষিপ্ত বিবরণ

এটি একাধিক পরিসংখ্যানগত ব্যান্ড এবং ট্রেন্ড বিশ্লেষণের উপর ভিত্তি করে একটি ট্রেডিং কৌশল। কৌশলটি বোলিঞ্জার ব্যান্ড, কোয়ান্টাইল ব্যান্ড এবং পাওয়ার ল ব্যান্ডের সম্মিলিত ব্যবহারের মাধ্যমে গুরুত্বপূর্ণ সাপোর্ট/রেজিস্ট্যান্স এলাকা চিহ্নিত করে এবং এন্ট্রি ও এক্সিটের সময় নির্ধারণের জন্য উপরের কোয়ান্টাইল ব্যান্ডের নিম্ন স্ট্যান্ডার্ড ডেভিয়েশন লাইনকে ট্রিগার সিগন্যাল হিসেবে ব্যবহার করে। কৌশলটি বাজারের অস্থিরতা বিবেচনায় নিয়ে ডিজাইন করা হয়েছে এবং একাধিক পরিসংখ্যানগত পদ্ধতির স্তরবিন্যাসের মাধ্যমে সংকেতের নির্ভরযোগ্যতা বৃদ্ধি করে।

কৌশলের নীতি

কৌশলের মূল নীতি হলো একাধিক পরিসংখ্যানগত ব্যান্ডের ক্রসওভারের মাধ্যমে বাজারের ট্রেন্ড ধরা। প্রধান উপাদানগুলির মধ্যে রয়েছে:

- বোলিঞ্জার ব্যান্ড সিস্টেম - দামের ওঠানামার পরিসর নির্ণয়ের জন্য; যখন দাম উপরের ব্যান্ড ভেঙে যায়, তখন হলুদ সতর্কতা সক্রিয় হয়।

- কোয়ান্টাইল ব্যান্ড সিস্টেম - দামের উপরের এবং নিচের কোয়ান্টাইল গণনা করে, দামের চরম হওয়ার সম্ভাবনা মূল্যায়ন করে।

- পাওয়ার ল ব্যান্ড সিস্টেম - ঐতিহাসিক রিটার্নের উপর ভিত্তি করে তাৎপর্যপূর্ণ স্তর গণনা করে, ওভারবট/ওভারসেল পরিমাপ করে।

- ট্রিগার সিস্টেম - উপরের কোয়ান্টাইল ব্যান্ডের নিম্ন স্ট্যান্ডার্ড ডেভিয়েশন লাইনকে প্রধান ট্রিগার সংকেত হিসেবে ব্যবহার করে; দাম এই লাইনের উপরে থাকলে তাকে বুলিশ সংকেত ধরা হয়।

- নিশ্চিতকরণ সিস্টেম - ক্রমাগত নিশ্চিতকরণ ক্যান্ডেলের সংখ্যা নির্ধারণের মাধ্যমে মিথ্যা সংকেত ফিল্টার করা হয়।

কৌশলের সুবিধা

- সংকেতের স্থায়িত্ব বেশি - একাধিক পরিসংখ্যানগত ব্যান্ডের স্তরবিন্যাস মিথ্যা সংকেত কার্যকরভাবে কমায়।

- অভিযোজন ক্ষমতা ভালো - কৌশলটি বিভিন্ন সময় ফ্রেম এবং বাজারের অবস্থার সাথে খাপ খাইয়ে নিতে পারে।

- ঝুঁকি নিয়ন্ত্রণ সম্পূর্ণ - একাধিক পরিসংখ্যানগত ব্যান্ড ব্যবহার করে ঝুঁকিপূর্ণ এলাকা বিভক্ত করা হয়েছে, পাশাপাশি স্টপ-লস ব্যবস্থা রয়েছে।

- প্যারামিটার নমনীয়তা - বিভিন্ন বাজারের বৈশিষ্ট্যের জন্য অপ্টিমাইজেশনের জন্য প্রচুর প্যারামিটার বিকল্প সরবরাহ করে।

- দৃশ্যমানতা স্পষ্ট - বিভিন্ন সূচকের লাইনের রঙ পরিষ্কারভাবে আলাদা, ট্রেড সংকেত সহজবোধ্য।

কৌশলের ঝুঁকি

- ল্যাগিং ঝুঁকি - পরিসংখ্যানগত সূচকগুলির কিছুটা বিলম্ব আছে, ফলে সেরা এন্ট্রি পয়েন্ট মিস হতে পারে।

- রেঞ্জ-বাউন্ড বাজারে অসুবিধা - পার্শ্বীয় রেঞ্জিং বাজারে অতিরিক্ত ট্রেড সংকেত তৈরি হতে পারে।

- প্যারামিটার সংবেদনশীলতা - বিভিন্ন প্যারামিটার কম্বিনেশনের ফলাফলে বড় পার্থক্য দেখা যায়, বারবার অপ্টিমাইজেশন প্রয়োজন।

- গণনার ভার বেশি - একাধিক পরিসংখ্যানগত সূচকের রিয়েল-টাইম গণনার জন্য বেশি কম্পিউটেশনাল রিসোর্স প্রয়োজন।

- বাজার পরিবেশের উপর নির্ভরশীলতা - চরম বাজার পরিবেশে পরিসংখ্যানগত প্যাটার্ন ব্যর্থ হতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

- ডায়নামিক প্যারামিটার অন্তর্ভুক্তি - বাজারের অস্থিরতা অনুযায়ী স্বয়ংক্রিয়ভাবে বিভিন্ন প্যারামিটার সামঞ্জস্য করা।

- বাজার পরিবেশ নির্ণয় যোগ করা - রেঞ্জিং বাজারের সংকেত ফিল্টার করার জন্য ট্রেন্ড শক্তি সূচক যুক্ত করা।

- গণনার দক্ষতা অপ্টিমাইজ করা - গণনা প্রক্রিয়ার কিছু অংশ সরল করে রিসোর্স ব্যবহার কমানো।

- ঝুঁকি নিয়ন্ত্রণ উন্নত করা - আরও স্টপ-লস শর্ত এবং পজিশন ম্যানেজমেন্ট কৌশল যোগ করা।

- অভিযোজন ক্ষমতা বাড়ানো - স্বয়ংক্রিয়-অভিযোজিত প্যারামিটার অপ্টিমাইজেশন সিস্টেম তৈরি করা।

সারসংক্ষেপ

এটি একাধিক পরিসংখ্যানগত পদ্ধতির সংমিশ্রণে একটি ব্যাপক ট্রেন্ড-অনুসরণকারী ট্রেডিং কৌশল। বোলিঞ্জার ব্যান্ড, কোয়ান্টাইল ব্যান্ড এবং পাওয়ার ল ব্যান্ডের সমন্বিত প্রভাবের মাধ্যমে এটি বাজারের ট্রেন্ড ভালোভাবে বুঝতে পারে এবং পাশাপাশি ঝুঁকি নিয়ন্ত্রণের ভালো ক্ষমতা রাখে। যদিও কিছু ল্যাগ এবং প্যারামিটার অপ্টিমাইজেশনে অসুবিধা রয়েছে, তবে ক্রমাগত উন্নতি এবং অপ্টিমাইজেশনের মাধ্যমে এই কৌশলটির ব্যবহারিক মূল্য এবং উন্নয়নের সম্ভাবনা ভালো।

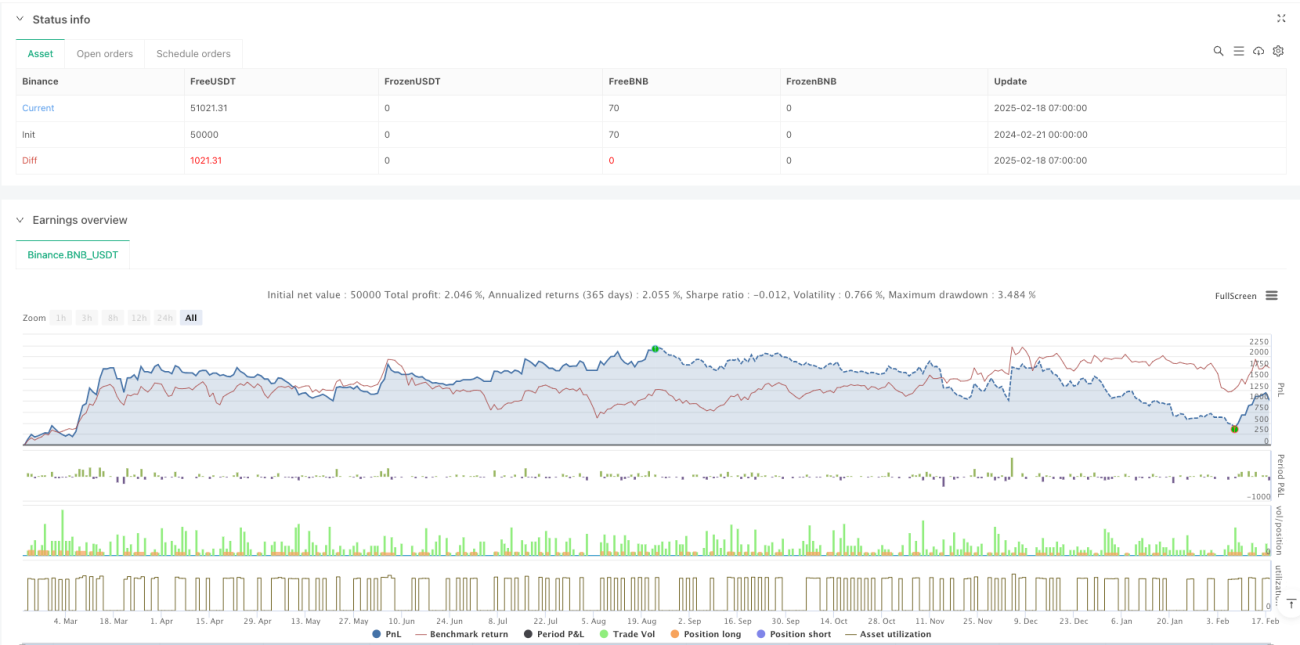

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BNB_USDT"}]

*/

//@version=6

strategy("Multi-Band Comparison Strategy with Separate Entry/Exit Confirmation", overlay=true,

default_qty_type=strategy.percent_of_equity, default_qty_value=10,

initial_capital=5000, currency=currency.USD)- 1