সংক্ষিপ্ত বিবরণ

এই কৌশলটি হল একটি ট্রেন্ড অনুসরণকারী সিস্টেম যা ভলিউম এবং মূল্য পরিবর্তনের উপর ভিত্তি করে তৈরি করা হয়েছে। এটি নেট ভলিউম অসিলেটর (NVO) গণনার মাধ্যমে বাজারের গতিবিধি পূর্বাভাস দেয়। কৌশলটি একাধিক মুভিং এভারেজ টাইপ (EMA, WMA, SMA, HMA) একত্রিত করে, অসিলেটর এবং এর EMA ওভারলে লাইনের অবস্থানের তুলনা করে বাজারের প্রবণতা নির্ধারণ করে এবং উপযুক্ত সময়ে ট্রেড করে। কৌশলটিতে ঝুঁকি নিয়ন্ত্রণ এবং লাভ লক করার জন্য স্টপ-লস এবং টেক-প্রফিট ব্যবস্থাও অন্তর্ভুক্ত রয়েছে।

কৌশলের মূলনীতি

কৌশলের মূল হল প্রতিদিনের নেট ভলিউম অসিলেটর মান গণনা করে বাজারের মেজাজ নির্ধারণ করা। নির্দিষ্ট গণনা পদ্ধতি নিম্নরূপ:

- মূল্য পরিসীমা মাল্টিপ্লায়ার গণনা: দিনের সর্বোচ্চ, সর্বনিম্ন এবং ক্লোজিং মূল্যের ভিত্তিতে 0-1 এর মধ্যে একটি মাল্টিপ্লায়ার গণনা করা হয়।

- কার্যকরী ঊর্ধ্বগতি এবং নিম্নগতি ভলিউম গণনা: মূল্যের দিক এবং মাল্টিপ্লায়ারের ভিত্তিতে ভলিউমকে ওজন করা হয়।

- নেট ভলিউম গণনা: কার্যকরী ঊর্ধ্বগতি ভলিউম থেকে কার্যকরী নিম্নগতি ভলিউম বিয়োগ করা হয়।

- নির্বাচিত মুভিং এভারেজ প্রয়োগ: নেট ভলিউম ডেটাকে মসৃণ করা হয়।

- EMA ওভারলে লাইন গণনা: প্রবণতা নির্ণয়ের জন্য রেফারেন্স লাইন হিসাবে ব্যবহার করা হয়।

- পরিবর্তনের হার (ROC) গণনা: প্রবণতার শক্তি পরিবর্তন নির্ণয়ের জন্য ব্যবহার করা হয়।

ট্রেডিং সিগন্যাল নিম্নলিখিত নিয়মের ভিত্তিতে তৈরি হয়:

- লং শর্ত: অসিলেটর EMA ওভারলে লাইনের উপরে উঠে আসে।

- শর্ট শর্ত: অসিলেটর EMA ওভারলে লাইনের নিচে নেমে যায়।

- স্টপ-লস: শতাংশ ভিত্তিক মূল্য স্টপ-লস।

- টেক-প্রফিট: শতাংশ ভিত্তিক মূল্য টেক-প্রফিট।

কৌশলের সুবিধা

- বহুমাত্রিক বিশ্লেষণ: মূল্য, ভলিউম এবং প্রবণতা পরিবর্তনের হার - এই তিনটি মাত্রার বাজারের তথ্য একত্রিত করা হয়েছে।

- উচ্চ নমনীয়তা: একাধিক মুভিং এভারেজ টাইপ সমর্থন করে, যা বিভিন্ন বাজারের বৈশিষ্ট্য অনুযায়ী সমন্বয় করা যায়।

- সম্পূর্ণ ঝুঁকি ব্যবস্থাপনা: স্টপ-লস এবং টেক-প্রফিট ব্যবস্থা অন্তর্ভুক্ত, যা কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করে।

- দৃশ্যমান প্রভাব: হিস্টোগ্রামের মাধ্যমে প্রবণতার শক্তি পরিবর্তন দেখানো হয়, যা বাজারের অবস্থা বোঝা সহজ করে।

- উচ্চ অভিযোজন ক্ষমতা: প্যারামিটারাইজড ডিজাইনের মাধ্যমে বিভিন্ন বাজারের পরিবেশ এবং ট্রেডিং পণ্যের সাথে খাপ খাইয়ে নেওয়া যায়।

কৌশলের ঝুঁকি

- ট্রেন্ড রিভার্সাল ঝুঁকি: অস্থির বাজারে ঘন ঘন মিথ্যা সিগন্যাল তৈরি হতে পারে।

- ল্যাগ ঝুঁকি: মুভিং এভারেজের নিজস্ব কিছু ল্যাগ থাকে, যা প্রবেশ এবং প্রস্থানের সময়কে অপর্যাপ্ত করতে পারে।

- প্যারামিটার সংবেদনশীলতা: বিভিন্ন প্যারামিটার সংমিশ্রণে কৌশলের কার্যক্ষমতা ব্যাপকভাবে ভিন্ন হতে পারে।

- বাজারের পরিবেশের উপর নির্ভরশীলতা: নির্দিষ্ট বাজারের পরিবেশে কার্যক্ষমতা খারাপ হতে পারে।

- প্রযুক্তিগত সীমাবদ্ধতা: শুধুমাত্র প্রযুক্তিগত সূচকের উপর নির্ভর করে, মৌলিক বিষয়গুলি বিবেচনা করে না।

ঝুঁকি নিয়ন্ত্রণের পরামর্শ:

- বিভিন্ন বাজারের পরিবেশে প্যারামিটার অপ্টিমাইজেশন করার পরামর্শ দেওয়া হয়।

- সিগন্যাল নিশ্চিতকরণের জন্য অন্যান্য প্রযুক্তিগত সূচক যুক্ত করা যেতে পারে।

- বিভিন্ন বাজারের অস্থিরতার সাথে খাপ খাইয়ে নিতে স্টপ-লস এবং টেক-প্রফিট প্যারামিটারগুলি যথাযথভাবে সমন্বয় করুন।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

-

সিগন্যাল নিশ্চিতকরণ পদ্ধতি অপ্টিমাইজেশন:

- ভলিউম নিশ্চিতকরণ শর্ত যোগ করা।

- প্রবণতা শক্তি ফিল্টার যুক্ত করা।

- অস্থিরতা-অভিযোজিত প্রক্রিয়া চালু করা।

-

ঝুঁকি ব্যবস্থাপনা অপ্টিমাইজেশন:

- গতিশীল স্টপ-লস পদ্ধতি বাস্তবায়ন করা।

- অর্থ ব্যবস্থাপনা মডিউল যুক্ত করা।

- ধাপে ধাপে পজিশন খোলা এবং কমানোর পদ্ধতি চালু করা।

-

প্যারামিটার অপ্টিমাইজেশন:

- অভিযোজিত প্যারামিটার সমন্বয় পদ্ধতি তৈরি করা।

- বাজারের পরিবেশের ভিত্তিতে প্যারামিটার পরিবর্তনের পদ্ধতি বাস্তবায়ন করা।

- প্যারামিটার অপ্টিমাইজেশনের জন্য মেশিন লার্নিং মডেল যুক্ত করা।

সারসংক্ষেপ

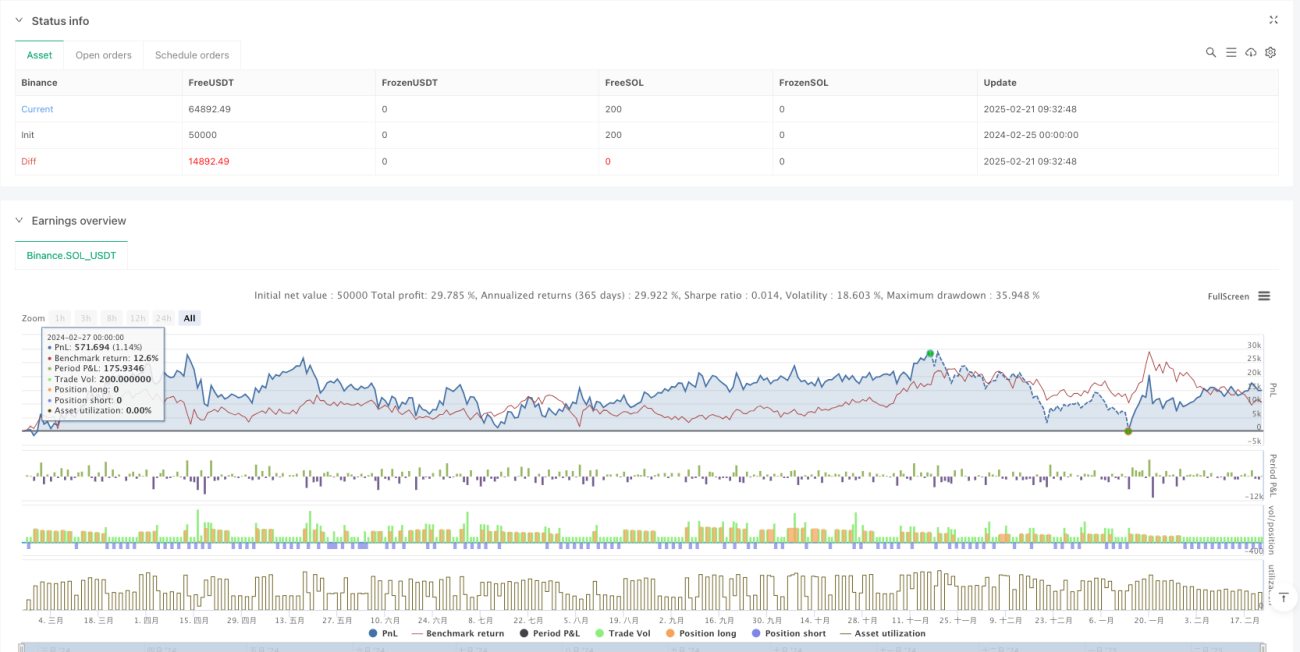

এই কৌশলটি ভলিউম এবং মূল্য ডেটা সমন্বিত বিশ্লেষণের মাধ্যমে একটি অপেক্ষাকৃত সম্পূর্ণ ট্রেন্ড অনুসরণকারী ট্রেডিং সিস্টেম তৈরি করেছে। কৌশলটির প্রধান বৈশিষ্ট্য হল একাধিক প্রযুক্তিগত সূচকের সংমিশ্রণ এবং নমনীয় প্যারামিটার কনফিগারেশন বিকল্প প্রদান। যদিও কিছু ঝুঁকি রয়েছে, তবে যথাযথ ঝুঁকি নিয়ন্ত্রণ এবং ধারাবাহিক অপ্টিমাইজেশনের মাধ্যমে এই কৌশলটি বাস্তব ট্রেডিংয়ে স্থিতিশীল লাভ অর্জন করতে সক্ষম। সুপারিশ করা হচ্ছে যে, ট্রেডাররা লাইভ ট্রেডিংয়ে ব্যবহারের আগে পর্যাপ্ত ব্যাকটেস্টিং করুন এবং নির্দিষ্ট বাজারের অবস্থা অনুযায়ী প্যারামিটারগুলি যথাযথভাবে সমন্বয় করুন।

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("EMA-Based Net Volume Oscillator with Trend Change", shorttitle="NVO Trend Change", overlay=false, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input parameters- 1