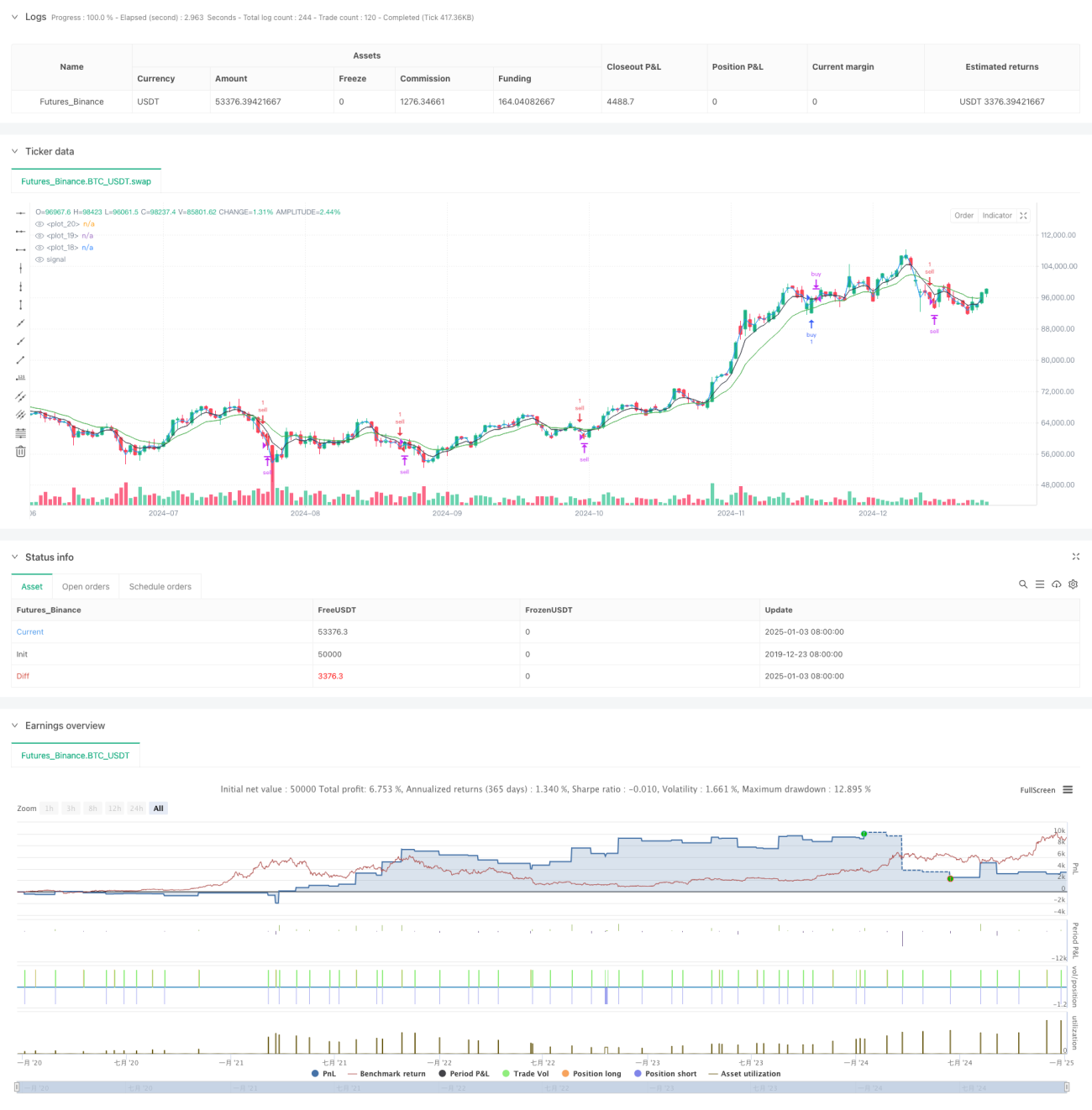

Dies ist eine umfassende Momentum-Handelsstrategie, die auf mehreren gleitenden Durchschnittskreuzungen und Volumen-Preis-Indikatoren basiert. Die Strategie generiert Handelssignale durch das Zusammenspiel mehrerer Indikatoren wie dem schnellen und langsamen exponentiellen gleitenden Durchschnitt (EMA), dem volumengewichteten Durchschnittspreis (VWAP) und dem SuperTrend, und nutzt zusätzlich intraday-Handelszeitfenster und Kursänderungsbereiche zur Steuerung von Ein- und Ausstiegen.

Strategieprinzip

Die Strategie verwendet den 5-Tage- und 13-Tage-EMA als primären Trendindikator. Ein Long-Signal wird ausgelöst, wenn der schnelle EMA den langsamen EMA von unten kreuzt und der Schlusskurs über dem VWAP liegt; ein Short-Signal wird ausgelöst, wenn der schnelle EMA den langsamen EMA von oben kreuzt und der Schlusskurs unter dem VWAP liegt. Gleichzeitig wird der SuperTrend-Indikator als Trendbestätigung und zur Stop-Loss-Setzung integriert. Die Strategie legt für verschiedene Handelstage unterschiedliche Einstiegsbedingungen fest, darunter die Preisänderung relativ zum Schlusskurs des vorherigen Handelstages, die Spanne zwischen Tageshoch und Tagestief sowie die Preisbewegungsspanne.

Vorteile der Strategie

- Die Kombination mehrerer technischer Indikatoren erhöht die Zuverlässigkeit der Handelssignale.

- Unterschiedliche Einstiegsbedingungen für verschiedene Handelstage passen sich besser den Markteigenschaften an.

- Dynamische Take-Profit- und Stop-Loss-Mechanismen ermöglichen eine effektive Risikokontrolle.

- Die Begrenzung auf intraday-Handelszeitfenster vermeidet Risiken in Phasen hoher Volatilität.

- Die Einschränkung durch vorherige Hochs/Tiefs und Preisbewegungsspannen reduziert das Risiko, zu hoch zu kaufen oder zu niedrig zu verkaufen.

Risiken der Strategie

- In schnelllebigen Märkten können falsche Signale auftreten.

- Zu Beginn von Trendumkehrungen kann es zu Verzögerungen kommen.

- Die Parameteroptimierung birgt das Risiko einer Überanpassung.

- Transaktionskosten können die Strategieerträge beeinträchtigen.

- In Phasen hoher Marktvolatilität sind größere Drawdowns möglich.

Optimierungsrichtungen der Strategie

- Die Einführung von Volumenanalyse-Indikatoren zur weiteren Bestätigung der Trendstärke könnte in Betracht gezogen werden.

- Optimierung der Parametereinstellungen für verschiedene Handelstage zur Verbesserung der Anpassungsfähigkeit.

- Hinzufügen weiterer Marktstimmungsindikatoren zur Steigerung der Prognosegenauigkeit.

- Verbesserung der Take-Profit- und Stop-Loss-Mechanismen zur effizienteren Kapitalnutzung.

- Berücksichtigung von Volatilitätsindikatoren zur Optimierung des Positionsmanagements.

Zusammenfassung

Die Strategie vereint Trendfolge und Momentum-Handel durch den kombinierten Einsatz mehrerer technischer Indikatoren. Das Strategiedesign berücksichtigt die Vielfalt des Marktes und wendet unterschiedliche Handelsregeln für verschiedene Handelstage an. Durch strenge Risikokontrolle und flexible Take-Profit-/Stop-Loss-Mechanismen zeigt die Strategie einen guten praktischen Anwendungswert. Zukünftig könnten weitere technische Indikatoren und optimierte Parametereinstellungen eingeführt werden, um die Stabilität und Rentabilität der Strategie zu verbessern.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=6

strategy("S1", overlay=true)

fastEMA = ta.ema(close, 5)- 1