Überblick

Diese Strategie ist ein trendfolgendes System, das auf Volumen- und Preisbewegungen basiert und durch die Berechnung des Net-Volume-Oszillators (NVO) die Marktrichtung vorhersagt. Die Strategie kombiniert verschiedene Arten von gleitenden Durchschnitten (EMA, WMA, SMA, HMA), indem sie die Lagebeziehung zwischen dem Oszillator und seiner EMA-Überlagerungslinie vergleicht, um Markttrends zu beurteilen und zu geeigneten Zeitpunkten zu handeln. Die Strategie enthält auch Stop-Loss- und Take-Profit-Mechanismen, um Risiken zu kontrollieren und Gewinne zu sichern.

Strategieprinzip

Der Kern der Strategie besteht darin, die tägliche Netto-Volume-Oszillation zu berechnen, um die Marktstimmung zu beurteilen. Die spezifischen Berechnungsschritte sind wie folgt:

- Berechnung des Preisbereichsmultiplikators: Basierend auf dem Tageshoch, -tief und -schlusskurs wird ein Multiplikator zwischen 0 und 1 berechnet.

- Berechnung der effektiven Aufwärts- und Abwärtsvolumina: Gewichtung des Volumens basierend auf der Preisbewegungsrichtung und dem Multiplikator.

- Berechnung des Netto-Volumens: Subtraktion des effektiven Abwärtsvolumens vom effektiven Aufwärtsvolumen.

- Anwendung des ausgewählten gleitenden Durchschnitts: Glättung der Netto-Volumendaten.

- Berechnung der EMA-Überlagerungslinie: Dient als Referenzlinie für die Trendbeurteilung.

- Berechnung der Veränderungsrate (ROC): Zur Beurteilung von Trendstärkeänderungen.

Die Generierung von Handelssignalen basiert auf folgenden Regeln:

- Long-Bedingung: Der Oszillator kreuzt die EMA-Überlagerungslinie von unten nach oben.

- Short-Bedingung: Der Oszillator kreuzt die EMA-Überlagerungslinie von oben nach unten.

- Stop-Loss: Prozentualer Preis-Stop-Loss.

- Take-Profit: Prozentualer Preis-Take-Profit.

Strategievorteile

- Mehrdimensionale Analyse: Kombiniert Marktinformationen aus den drei Dimensionen Preis, Volumen und Änderungsrate des Trends.

- Hohe Flexibilität: Unterstützt mehrere Arten von gleitenden Durchschnitten, die an verschiedene Marktmerkmale angepasst werden können.

- Vollständiges Risikomanagement: Enthält Stop-Loss- und Take-Profit-Mechanismen, die eine effektive Risikokontrolle ermöglichen.

- Starke Visualisierung: Zeigt Trendstärkeänderungen durch Histogramme an, erleichtert das Verständnis der Marktsituation.

- Hohe Anpassungsfähigkeit: Durch parametrisiertes Design kann es an verschiedene Marktumgebungen und Handelsinstrumente angepasst werden.

Strategierisiken

- Trendumkehrrisiko: In Seitwärtsmärkten können häufige Fehlsignale auftreten.

- Verzögerungsrisiko: Gleitende Durchschnitte haben eine inhärente Verzögerung, die zu suboptimalen Ein- und Ausstiegszeitpunkten führen kann.

- Parameterempfindlichkeit: Unterschiedliche Parametersätze können zu stark abweichenden Strategieleistungen führen.

- Abhängigkeit vom Marktumfeld: In bestimmten Marktumgebungen kann die Strategie schlecht abschneiden.

- Technische Limitierung: Verlässt sich nur auf technische Indikatoren, ohne fundamentale Faktoren zu berücksichtigen.

Risikomanagement-Empfehlungen:

- Parameteroptimierung unter verschiedenen Marktumgebungen wird empfohlen.

- Kann mit anderen technischen Indikatoren zur Signalbestätigung kombiniert werden.

- Stop-Loss- und Take-Profit-Parameter sollten an die jeweilige Marktvolatilität angepasst werden.

Strategieoptimierungsrichtungen

-

Optimierung der Signalbestätigungsmechanismen:

- Hinzufügen von Volumenbestätigungsbedingungen

- Einführung eines Trendstärkefilters

- Implementierung eines volatilitätsadaptiven Mechanismus

-

Optimierung des Risikomanagements:

- Implementierung eines dynamischen Stop-Loss-Mechanismus

- Hinzufügen eines Money-Management-Moduls

- Einführung von schrittweisem Aufbau und Abbau von Positionen

-

Parameteroptimierung:

- Entwicklung eines adaptiven Parameteranpassungsmechanismus

- Implementierung eines parameterwechsels basierend auf dem Marktumfeld

- Hinzufügen von maschinellem Lernen zur Parameteroptimierung

Zusammenfassung

Diese Strategie konstruiert durch die umfassende Analyse von Volumen- und Preisdaten ein relativ vollständiges Trendfolge-Handelssystem. Das Hauptmerkmal der Strategie ist die Kombination mehrerer technischer Indikatoren und die Bereitstellung flexibler Parameterkonfigurationsoptionen. Obwohl gewisse Risiken bestehen, kann die Strategie durch angemessenes Risikomanagement und kontinuierliche Optimierung voraussichtlich stabile Erträge im praktischen Handel erzielen. Händlern wird empfohlen, vor dem Einsatz im Live-Handel ausreichende Backtests durchzuführen und die Parameter entsprechend den spezifischen Marktbedingungen anzupassen.

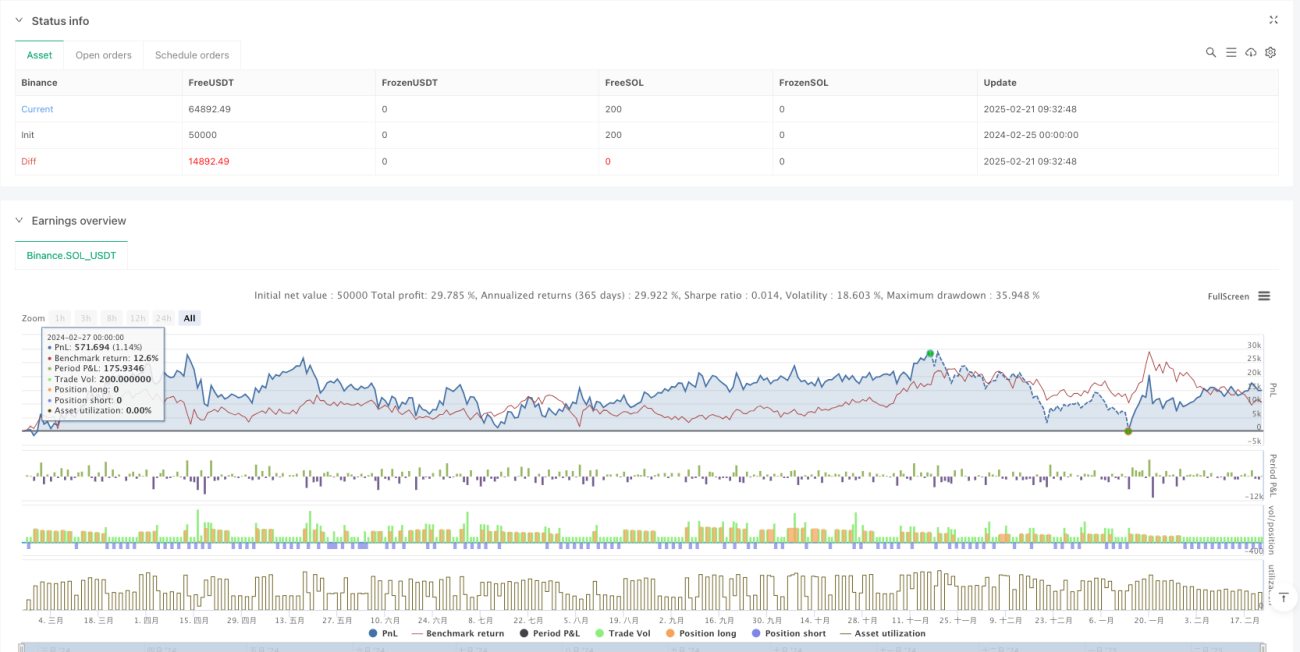

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("EMA-Based Net Volume Oscillator with Trend Change", shorttitle="NVO Trend Change", overlay=false, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input parameters- 1