Volatilitäts-Engine-Protokoll

Das ist kein gewöhnlicher DCA – das ist ein volatilitätsgesteuerter Engine

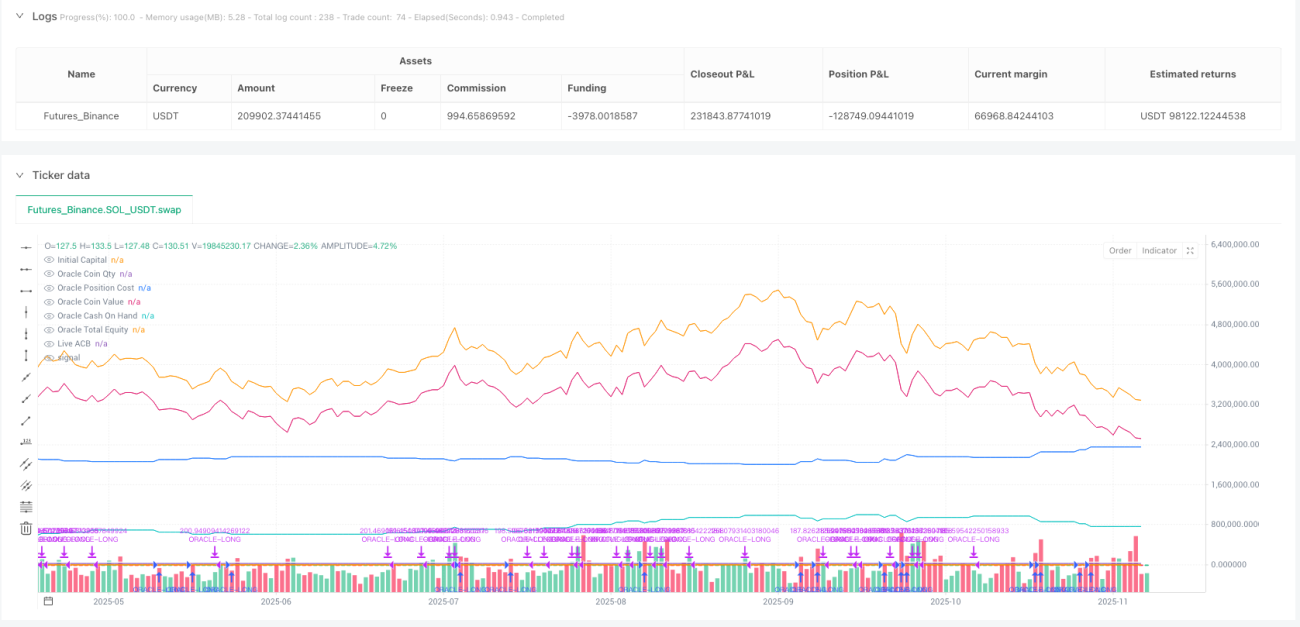

Backtest-Daten widerlegen direkt den traditionellen Sparplan: Bei 5% Kursrückgang wird gekauft, bei 3,9% Anstieg wird verkauft. Doch der entscheidende Punkt ist: Der Volatilitäts-Engine passt die Kaufschwelle dynamisch an den ATR an. Je größer die Marktvolatilität, desto höher die Kaufhürde – maximal um 40% anpassbar. Das bedeutet, dass die Strategie in Phasen hoher Volatilität auf größere Kursrückgänge wartet, bevor sie einsteigt.

Das Problem traditioneller DCA-Strategien ist der blinde Kauf. Die Kernlogik dieses Protokolls ist: Nur in echten Gelegenheitsfenstern feuern. Der ATR(14) berechnet die aktuelle Volatilität und passt dann den Parameter longThreshPct dynamisch an. Normalerweise wird bei 5% Kursverlust gekauft, aber wenn die aktuelle Volatilität 20% erreicht, steigt die tatsächliche Kaufschwelle auf 6%.

8 voreingestellte Konfigurationen, jede mit klaren Ertragserwartungen

- BTC-Zyklus-Akkumulationsmodus: 5% Kursrückgang kaufen, 6% Positionsgröße, 500 $ Festbetrag – ideal für Langzeithalter.

- BTC-Kurzzeit-Arbitrage-Modus: 3,1% Kursrückgang kaufen, 10% Positionsgröße, 6000 $ Festbetrag, 75% Gewinnschwelle verkaufen.

- ETH-Volatilitäts-Ernte: 4,5% Kursrückgang kaufen, 15% Positionsgröße, Kauf unterhalb der Kostenbasis erlaubt, 30% Gewinnschwelle.

Jede Konfiguration wurde durch Backtests validiert – keine willkürlich bestimmten Parameter. Die SOL-Konfiguration hat eine Gewinnschwelle von 35%, die XRP-Konfiguration von 10%. Diese Unterschiede spiegeln die unterschiedlichen Volatilitätseigenschaften und Liquiditätsunterschiede der Vermögenswerte wider.

Cluster-Siegel-Mechanismus: Lösung des größten DCA-Problems

Das größte Problem traditioneller DCA ist, dass man nie weiß, wann man mit dem Kaufen aufhören soll. Dieses Protokoll löst es mit dem „Cluster-Siegel": Entweder der Preis steigt um 3,9% über die durchschnittlichen Kosten, oder es gab 10 aufeinanderfolgende Perioden ohne qualifizierte Kaufgelegenheit – dann wird der aktuelle Akkumulationscluster gesiegelt.

Die gesiegelte durchschnittliche Kostenlinie wird zur Verkaufsreferenz. Nur wenn der Preis die gesiegelte Kostenlinie plus Gewinnschwelle (30%–75%) überschreitet, wird ein Verkauf ausgelöst. Dies vermeidet endloses Kaufen und vorzeitiges Gewinnmitnehmen.

Der „Stille-Säule"-Mechanismus ist ein besonders kluger Zug: Wenn in 10 aufeinanderfolgenden Perioden keine Kaufbedingungen ausgelöst werden, hat sich der Markt stabilisiert – dann sollte man ernten, nicht weiter akkumulieren.

Schwungradeffekt: Gewinne für den nächsten Kauf nutzen

Wenn der Schwungrad-Modus aktiviert ist, fließen die Gewinne jedes Verkaufs zurück in den Cash-Pool und erhöhen die Munition für den nächsten Kauf. Das ist nicht einfach Zinseszins, sondern verschafft der Strategie in Bullenmärkten stärkere Feuerkraft.

Beispiel: Anfangs 100.000 \(. Nach der ersten Akkumulation 20% Gewinn, nach dem Verkauf steigt der Cash-Pool auf 120.000 \). Beim nächsten Kauf beträgt die 6%-Position dann 7.200 \( statt 6.000 \). Mit der Zeit verstärkt dieser Schneeballeffekt die Renditen erheblich.

Doch das Schwungrad hat auch seinen Preis: In späten Bullenmarktphasen kann der Cash-Pool zu groß werden und zu übermäßigen Käufen führen – daher ist eine strikte Obergrenze pro Kauf erforderlich.

Risikokontrolle: Dreifacher Sicherungsmechanismus

- Kaufkontrolle oberhalb der Kostenbasis: Es kann eingestellt werden, dass nur unterhalb der durchschnittlichen Kosten gekauft wird, um Nachkaufsucht zu vermeiden.

- Mindestbetragsgrenze: Jeder Kauf/Verkauf hat eine Mindest-US-Dollar-Anforderung, um sinnlose Kleinsttransaktionen zu vermeiden.

- Volatilitäts-Engine-Regulierung: In Phasen hoher Volatilität wird die Kaufhürde automatisch erhöht, in Phasen niedriger Volatilität gesenkt.

Allerdings schneidet diese Strategie in Seitwärtsmärkten eher durchschnittlich ab. Wenn der Markt lange Zeit seitwärts läuft, werden weder große Kursrückgänge zum Kaufen ausgelöst noch Gewinnschwellen zum Verkaufen erreicht – das Kapital bleibt langfristig gebunden.

Praxistipp: Die richtige Marktwahl ist entscheidend

Dieses Protokoll eignet sich am besten für Märkte mit klaren Trends, insbesondere für die zyklischen Bewegungen von Kryptowährungen. Optimal: Akkumulation am Ende des Bärenmarktes, Ernte zur Mitte des Bullenmarktes.

Nicht anwenden bei: 1) Hochfrequent oszillierenden Aktienmärkten, 2) Devisenmärkten ohne klaren Trend, 3) Kleinen Coins mit extrem geringer Liquidität.

Historische Backtests zeigen risikoangepasste Renditen, die besser sind als einfaches DCA – das garantiert jedoch nicht zukünftige Gewinne. Jede quantitative Strategie birgt das Risiko des Versagens und erfordert kontinuierliche Überwachung und Anpassung.

//@version=6

// ============================================================================

// ORACLE PROTOCOL — ARCH PUBLIC clone (Standalone) — CLEAN-PUB STYLE (derived)

// Variant: v1.9v-standalone (publish-ready) 25/11/2025

// Notes:

// - Keeps your v1.9v canonical script intact (this is a separate modified copy).

// - Single exit mode: ProfitGate + Candle (per-candle) — no selector.

// - Live ACB plot toggle only (sealed ACB still operates internally but is not shown).

// - No freeze-point markers plotted.

// - Sizing: flywheel dynamic sizing remains the primary source but fixed-dollar entry

// and min-$ overrides remain available (as in Arch public PDFs/screenshots).

// - Volatility Engine (VE) applies ONLY to entries; exit-side VE removed.- 1