Teaches you to design a template library for obtaining specified K-length line data

Author: The Little Dream, Created: 2023-06-27 13:37:01, Updated: 2023-09-18 19:34:23

Teaches you to design a template library for obtaining specified K-length line data

When designing some trend strategies, the calculation of indicators often requires a sufficient number of K-line bars.exchange.GetRecords()The data quantity given by the function.exchange.GetRecords()The K-line interface is a wrapper for the exchange's K-line interface. There were no page-splitting queries in the early design of the cryptocurrency exchange's API interface, and the exchange's K-line interface was only available for a limited amount of data, so some developers could not meet the needs for the calculation of indicators with larger parameters.

Since the Binance Contract API's K-line interface supports page-splitting queries, this article will teach you how to implement a page-splitting query using the Binance K-line API as an example and specify how to access the FMZ platform template library for the number of bars.

Binance's K-line interface

The first thing to do is to look at the API documentation of the exchange and see the specific parameters of the interface. We can see that this K-line interface calls need to specify the variety, K-line cycle, data range (start, end time), number of pages, etc.

Since our design requirement is to query a specified amount of K-line data, for example, to query a 1-hour K-line, from the current moment to the past moment, the number of bars is 5000. So you only call an exchange API query once and obviously you don't get the data you want.

Then we split the page and process the query from the current moment to a certain moment in the history. The cycle of K-line data that we know we need is good for calculating the start and end times of each segment. Just use the segmentation to the historical moment direction until you have a sufficient number of bars.

Designing the "JavaScript version of the K-line history data template for page queries"

Interface functions for the design template:$.GetRecordsByLength(e, period, length)。

/**

* desc: $.GetRecordsByLength 是该模板类库的接口函数,该函数用于获取指定K线长度的K线数据

* @param {Object} e - 交易所对象

* @param {Int} period - K线周期,秒数为单位

* @param {Int} length - 指定获取的K线数据的长度,具体和交易所接口限制有关

* @returns {Array<Object>} - K线数据

*/

Design$.GetRecordsByLengthThis function, which is normally used in scenarios where a long K-line is required to perform calculations at the beginning of a strategy run. Once the function is executed, it takes enough data to update the new K-line data. It is no longer necessary to call this function to get the very long K-line data, which will cause unnecessary interface calls.

So we also need to design an interface for the subsequent data updates:$.UpdataRecords(e, records, period)。

/**

* desc: $.UpdataRecords 是该模板类库的接口函数,该函数用于更新K线数据

* @param {Object} e - 交易所对象

* @param {Array<Object>} records - 需要更新的K线数据源

* @param {Int} period - K线周期,需要和records参数传入的K线数据周期一致

* @returns {Bool} - 是否更新成功

*/

The next step is to implement these interface functions.

/**

* desc: $.GetRecordsByLength 是该模板类库的接口函数,该函数用于获取指定K线长度的K线数据

* @param {Object} e - 交易所对象

* @param {Int} period - K线周期,秒数为单位

* @param {Int} length - 指定获取的K线数据的长度,具体和交易所接口限制有关

* @returns {Array<Object>} - K线数据

*/

$.GetRecordsByLength = function(e, period, length) {

if (!Number.isInteger(period) || !Number.isInteger(length)) {

throw "params error!"

}

var exchangeName = e.GetName()

if (exchangeName == "Futures_Binance") {

return getRecordsForFuturesBinance(e, period, length)

} else {

throw "not support!"

}

}

/**

* desc: getRecordsForFuturesBinance 币安期货交易所获取K线数据函数的具体实现

* @param {Object} e - 交易所对象

* @param {Int} period - K线周期,秒数为单位

* @param {Int} length - 指定获取的K线数据的长度,具体和交易所接口限制有关

* @returns {Array<Object>} - K线数据

*/

function getRecordsForFuturesBinance(e, period, length) {

var contractType = e.GetContractType()

var currency = e.GetCurrency()

var strPeriod = String(period)

var symbols = currency.split("_")

var baseCurrency = ""

var quoteCurrency = ""

if (symbols.length == 2) {

baseCurrency = symbols[0]

quoteCurrency = symbols[1]

} else {

throw "currency error!"

}

var realCt = e.SetContractType(contractType)["instrument"]

if (!realCt) {

throw "realCt error"

}

// m -> 分钟; h -> 小时; d -> 天; w -> 周; M -> 月

var periodMap = {}

periodMap[(60).toString()] = "1m"

periodMap[(60 * 3).toString()] = "3m"

periodMap[(60 * 5).toString()] = "5m"

periodMap[(60 * 15).toString()] = "15m"

periodMap[(60 * 30).toString()] = "30m"

periodMap[(60 * 60).toString()] = "1h"

periodMap[(60 * 60 * 2).toString()] = "2h"

periodMap[(60 * 60 * 4).toString()] = "4h"

periodMap[(60 * 60 * 6).toString()] = "6h"

periodMap[(60 * 60 * 8).toString()] = "8h"

periodMap[(60 * 60 * 12).toString()] = "12h"

periodMap[(60 * 60 * 24).toString()] = "1d"

periodMap[(60 * 60 * 24 * 3).toString()] = "3d"

periodMap[(60 * 60 * 24 * 7).toString()] = "1w"

periodMap[(60 * 60 * 24 * 30).toString()] = "1M"

var records = []

var url = ""

if (quoteCurrency == "USDT") {

// GET https://fapi.binance.com /fapi/v1/klines symbol , interval , startTime , endTime , limit

// limit 最大值:1500

url = "https://fapi.binance.com/fapi/v1/klines"

} else if (quoteCurrency == "USD") {

// GET https://dapi.binance.com /dapi/v1/klines symbol , interval , startTime , endTime , limit

// startTime 与 endTime 之间最多只可以相差200天

// limit 最大值:1500

url = "https://dapi.binance.com/dapi/v1/klines"

} else {

throw "not support!"

}

var maxLimit = 1500

var interval = periodMap[strPeriod]

if (typeof(interval) !== "string") {

throw "period error!"

}

var symbol = realCt

var currentTS = new Date().getTime()

while (true) {

// 计算limit

var limit = Math.min(maxLimit, length - records.length)

var barPeriodMillis = period * 1000

var rangeMillis = barPeriodMillis * limit

var twoHundredDaysMillis = 200 * 60 * 60 * 24 * 1000

if (rangeMillis > twoHundredDaysMillis) {

limit = Math.floor(twoHundredDaysMillis / barPeriodMillis)

rangeMillis = barPeriodMillis * limit

}

var query = `symbol=${symbol}&interval=${interval}&endTime=${currentTS}&limit=${limit}`

var retHttpQuery = HttpQuery(url + "?" + query)

var ret = null

try {

ret = JSON.parse(retHttpQuery)

} catch(e) {

Log(e)

}

if (!ret || !Array.isArray(ret)) {

return null

}

// 超出交易所可查询范围,查询不到数据时

if (ret.length == 0 || currentTS <= 0) {

break

}

for (var i = ret.length - 1; i >= 0; i--) {

var ele = ret[i]

var bar = {

Time : parseInt(ele[0]),

Open : parseFloat(ele[1]),

High : parseFloat(ele[2]),

Low : parseFloat(ele[3]),

Close : parseFloat(ele[4]),

Volume : parseFloat(ele[5])

}

records.unshift(bar)

}

if (records.length >= length) {

break

}

currentTS -= rangeMillis

Sleep(1000)

}

return records

}

/**

* desc: $.UpdataRecords 是该模板类库的接口函数,该函数用于更新K线数据

* @param {Object} e - 交易所对象

* @param {Array<Object>} records - 需要更新的K线数据源

* @param {Int} period - K线周期,需要和records参数传入的K线数据周期一致

* @returns {Bool} - 是否更新成功

*/

$.UpdataRecords = function(e, records, period) {

var r = e.GetRecords(period)

if (!r) {

return false

}

for (var i = 0; i < r.length; i++) {

if (r[i].Time > records[records.length - 1].Time) {

// 添加新Bar

records.push(r[i])

// 更新上一个Bar

if (records.length - 2 >= 0 && i - 1 >= 0 && records[records.length - 2].Time == r[i - 1].Time) {

records[records.length - 2] = r[i - 1]

}

} else if (r[i].Time == records[records.length - 1].Time) {

// 更新Bar

records[records.length - 1] = r[i]

}

}

return true

}

In the template, we implemented only support for the Binance Contract K-line interface, which is thegetRecordsForFuturesBinanceThe function can also extend the K-line interface to support other cryptocurrency exchanges.

The test link

As you can see, there is not much code in the template to implement these functions, probably less than 200 lines. Once the template code is written, there is absolutely no shortage of testing. And for such data acquisition, we also need to test as strictly as possible.

The test requires copying the "JavaScript version page-query K-line history template" and "Draw line library" templates to its own policy library (see below).Strategy SquareWe then created a new policy to check out these two templates:

Using the "Draw Line Library" is because we need to draw the obtained K-line data out for observation.

function main() {

LogReset(1)

var testPeriod = PERIOD_M5

Log("当前测试的交易所:", exchange.GetName())

// 如果是期货则需要设置合约

exchange.SetContractType("swap")

// 使用$.GetRecordsByLength获取指定长度的K线数据

var r = $.GetRecordsByLength(exchange, testPeriod, 8000)

Log(r)

// 使用画图测试,方便观察

$.PlotRecords(r, "k")

// 检测数据

var diffTime = r[1].Time - r[0].Time

Log("diffTime:", diffTime, " ms")

for (var i = 0; i < r.length; i++) {

for (var j = 0; j < r.length; j++) {

// 检查重复Bar

if (i != j && r[i].Time == r[j].Time) {

Log(r[i].Time, i, r[j].Time, j)

throw "有重复Bar"

}

}

// 检查Bar连续性

if (i < r.length - 1) {

if (r[i + 1].Time - r[i].Time != diffTime) {

Log("i:", i, ", diff:", r[i + 1].Time - r[i].Time, ", r[i].Time:", r[i].Time, ", r[i + 1].Time:", r[i + 1].Time)

throw "Bar不连续"

}

}

}

Log("检测通过")

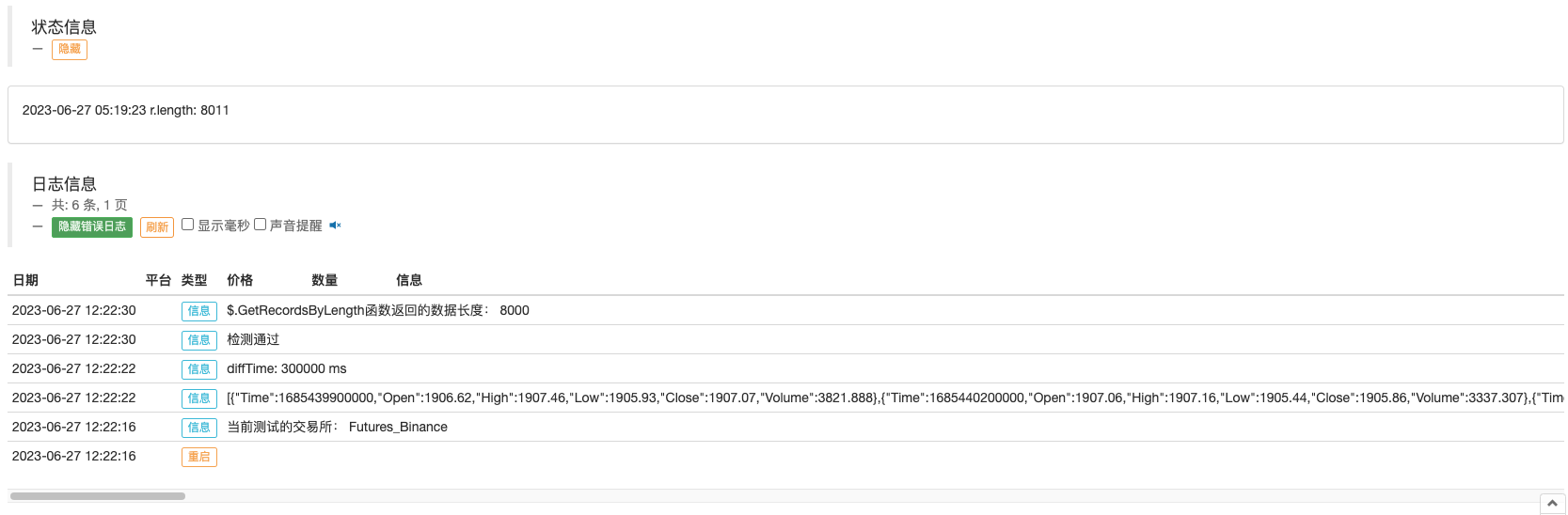

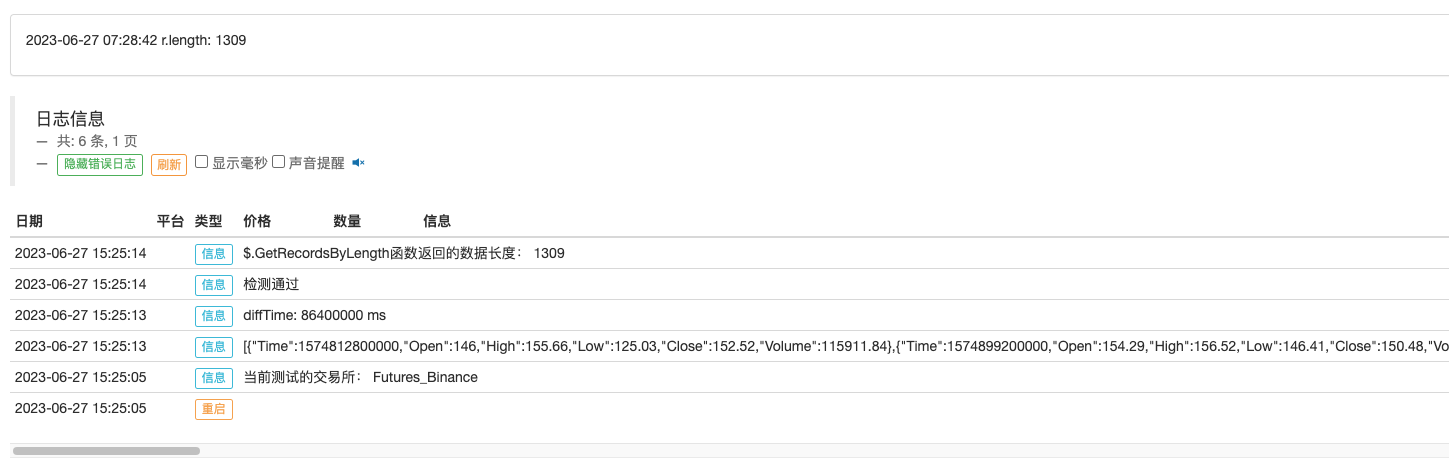

Log("$.GetRecordsByLength函数返回的数据长度:", r.length)

// 更新数据

while (true) {

$.UpdataRecords(exchange, r, testPeriod)

LogStatus(_D(), "r.length:", r.length)

$.PlotRecords(r, "k")

Sleep(5000)

}

}

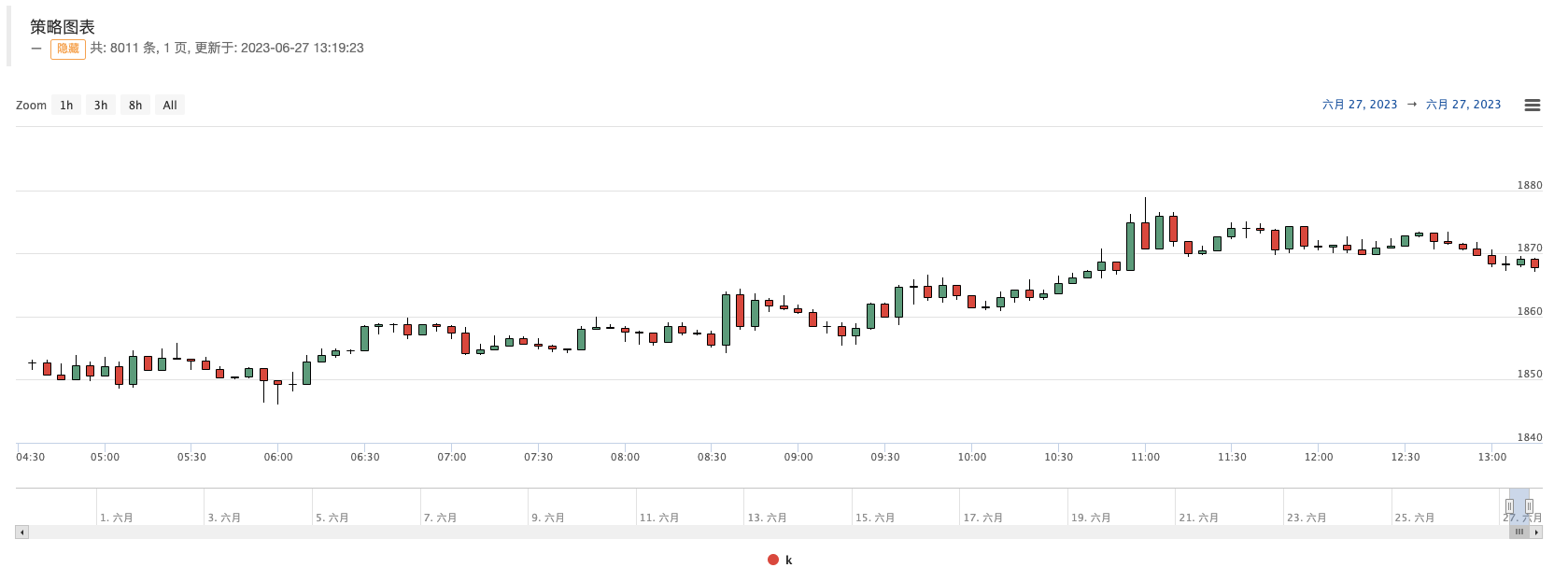

Here we usevar testPeriod = PERIOD_M5This sentence, set a 5-minute K-line cycle, specify get 8000 bars.var r = $.GetRecordsByLength(exchange, testPeriod, 8000)The long K-line data returned by the interface is used for graph testing:

// 使用画图测试,方便观察

$.PlotRecords(r, "k")

The following is a test of this long K-line data:

// 检测数据

var diffTime = r[1].Time - r[0].Time

Log("diffTime:", diffTime, " ms")

for (var i = 0; i < r.length; i++) {

for (var j = 0; j < r.length; j++) {

// 检查重复Bar

if (i != j && r[i].Time == r[j].Time) {

Log(r[i].Time, i, r[j].Time, j)

throw "有重复Bar"

}

}

// 检查Bar连续性

if (i < r.length - 1) {

if (r[i + 1].Time - r[i].Time != diffTime) {

Log("i:", i, ", diff:", r[i + 1].Time - r[i].Time, ", r[i].Time:", r[i].Time, ", r[i + 1].Time:", r[i + 1].Time)

throw "Bar不连续"

}

}

}

Log("检测通过")

1, check if there are any repetitions in K lineBar. 2, check the consistency of the K line Bar (whether the time deviation of the adjacent Bar is equal)

After these checks pass, check the interface used to update the K-line$.UpdataRecords(exchange, r, testPeriod)Is it normal:

// 更新数据

while (true) {

$.UpdataRecords(exchange, r, testPeriod)

LogStatus(_D(), "r.length:", r.length)

$.PlotRecords(r, "k")

Sleep(5000)

}

This code continues to output K-lines on the policy chart while running on the hard disk, so we check if the K-lineBar data is being updated or added correctly.

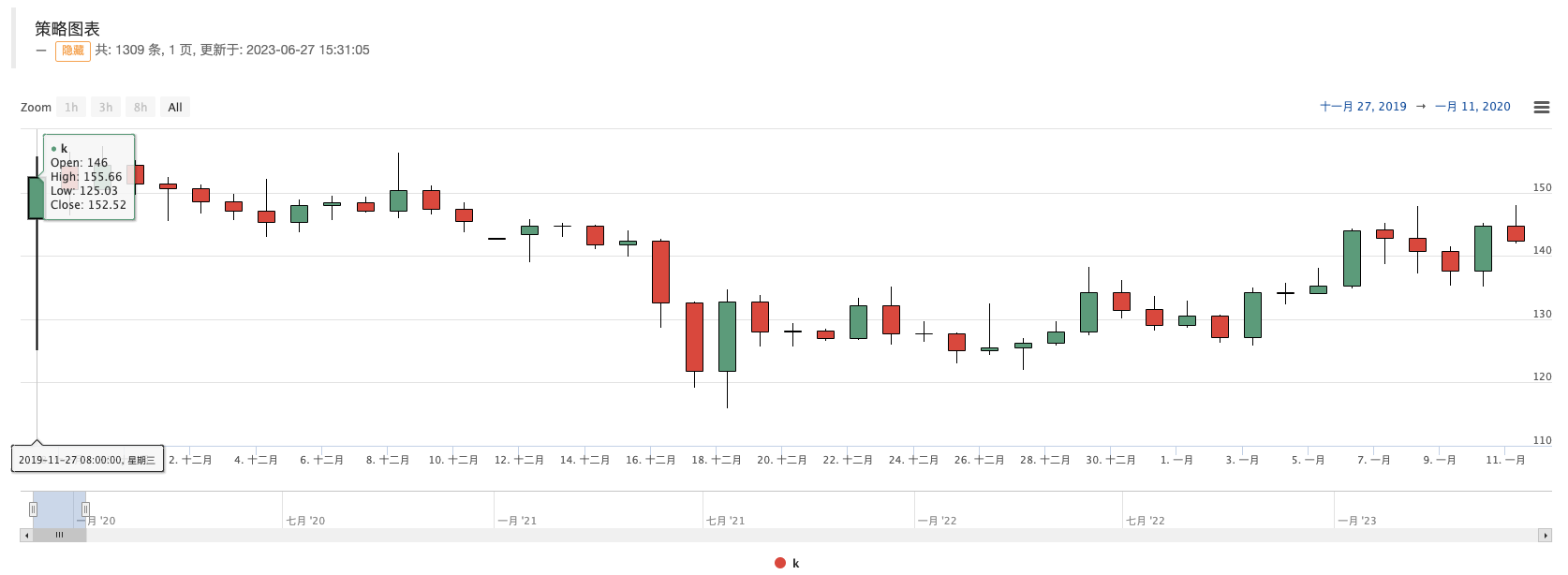

Using the Access Day K line, set the access to 8000 roots (knowing that there is no market data before 8000 days) to the following:

Seeing only 1309 roots in the dayline, compared to the data on the stock exchange chart:

You can see that the data also match.

END

The template address is:"JavaScript version of page search for K-line history template"The template address is:"Drawing class library"

The above templates, policy code are for teaching, learning and use only, please optimize or modify them according to your needs.