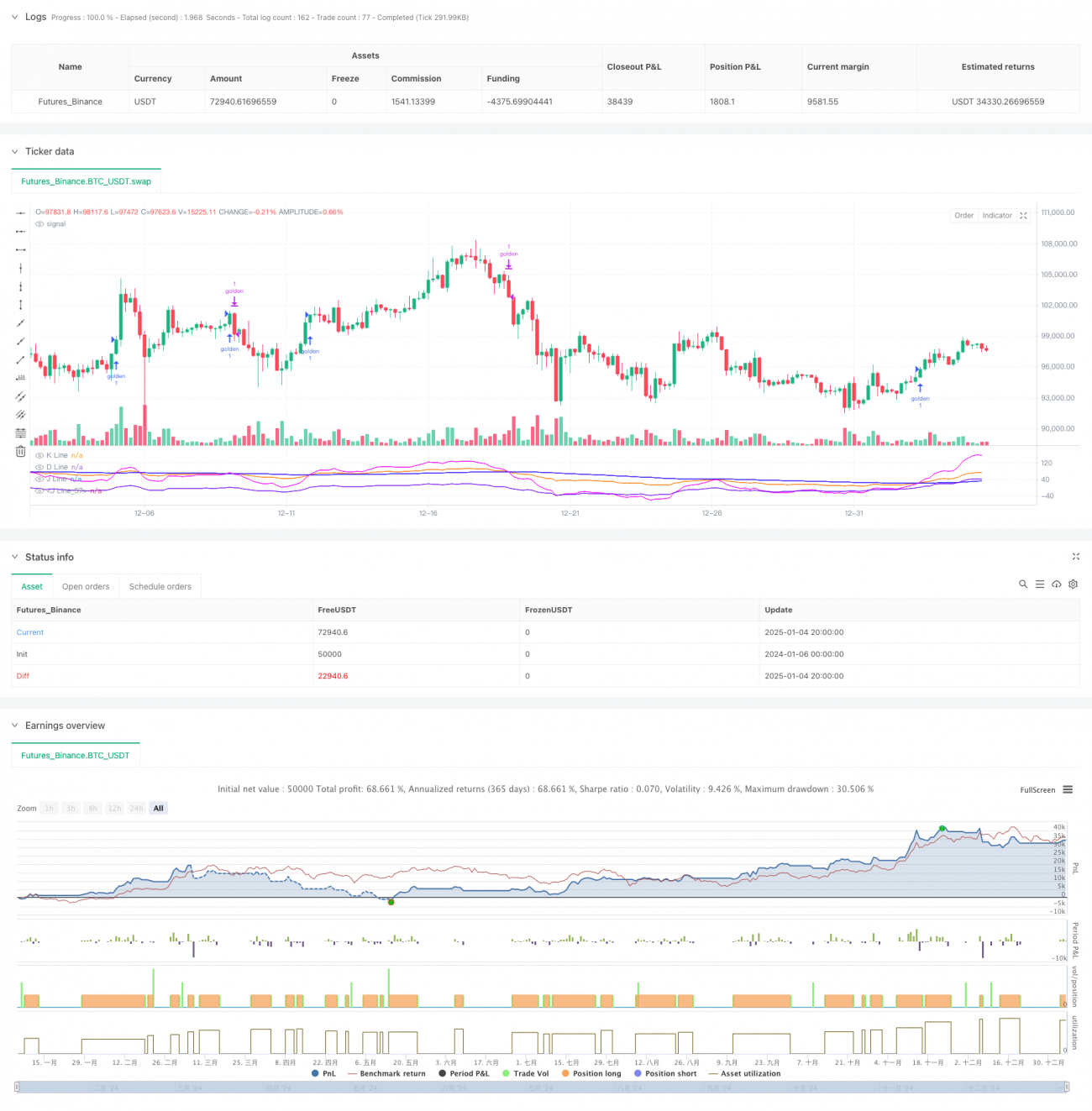

Overview

This strategy is an advanced trading system based on the KDJ indicator, which captures market trends through in-depth analysis of K-line, D-line, and J-line crossover patterns. The strategy integrates a custom BCWSMA smoothing algorithm, improving signal reliability through optimized calculation of stochastic indicators. The system employs strict risk control mechanisms, including stop-loss and trailing stop features, to achieve robust money management.

Strategy Principles

The core logic of the strategy is based on several key elements:

- Uses custom BCWSMA (Weighted Moving Average) algorithm to calculate KDJ indicators, improving indicator smoothness and stability

- Converts prices to 0-100 range through RSV (Raw Stochastic Value) calculation, better reflecting price position between highs and lows

- Designs unique J-line and J5-line (derivative indicator) cross-validation mechanism, improving trade signal accuracy through multiple confirmations

- Establishes trend confirmation mechanism based on continuity, requiring J-line to remain above D-line for 3 consecutive days to confirm trend validity

- Integrates composite risk control system with percentage stop-loss and trailing stop-loss

Strategy Advantages

- Advanced Signal Generation: Significantly reduces false signals through multiple technical indicator cross-validation

- Comprehensive Risk Control: Employs multi-level risk control mechanisms, including fixed and trailing stops, effectively controlling downside risk

- Strong Parameter Adaptability: Key parameters like KDJ period and signal smoothing coefficients can be flexibly adjusted based on market conditions

- High Computational Efficiency: Uses optimized BCWSMA algorithm, reducing computational complexity and improving strategy execution efficiency

- Good Adaptability: Can adapt to different market environments through parameter adjustment optimization

Strategy Risks

- Oscillation Market Risk: May generate frequent false breakout signals in sideways markets, increasing trading costs

- Lag Risk: Signals may experience some delay due to moving average smoothing

- Parameter Sensitivity: Strategy effectiveness is sensitive to parameter settings, improper settings may significantly reduce strategy performance

- Market Environment Dependency: Strategy performance may not be ideal in certain specific market environments

Strategy Optimization Directions

- Signal Filter Mechanism Optimization: Can introduce auxiliary indicators like volume and volatility to improve signal reliability

- Dynamic Parameter Adjustment: Dynamically adjust KDJ parameters and stop-loss parameters based on market volatility

- Market Environment Recognition: Add market environment judgment module to adopt different trading strategies in different market environments

- Risk Control Enhancement: Can add additional risk control measures like maximum drawdown control and position time limits

- Performance Optimization: Further optimize BCWSMA algorithm to improve computational efficiency

Summary

The strategy builds a complete trading system through innovative technical indicator combinations and strict risk control. The core advantages lie in multiple signal confirmation mechanisms and comprehensive risk control systems, but attention needs to be paid to parameter optimization and market environment adaptability. Through continuous optimization and improvement, the strategy has the potential to maintain stable performance across different market environments.

- 1