Adaptive Trend Following Strategy Based on Kernel Regression and ATR Dynamic Bands

Overview

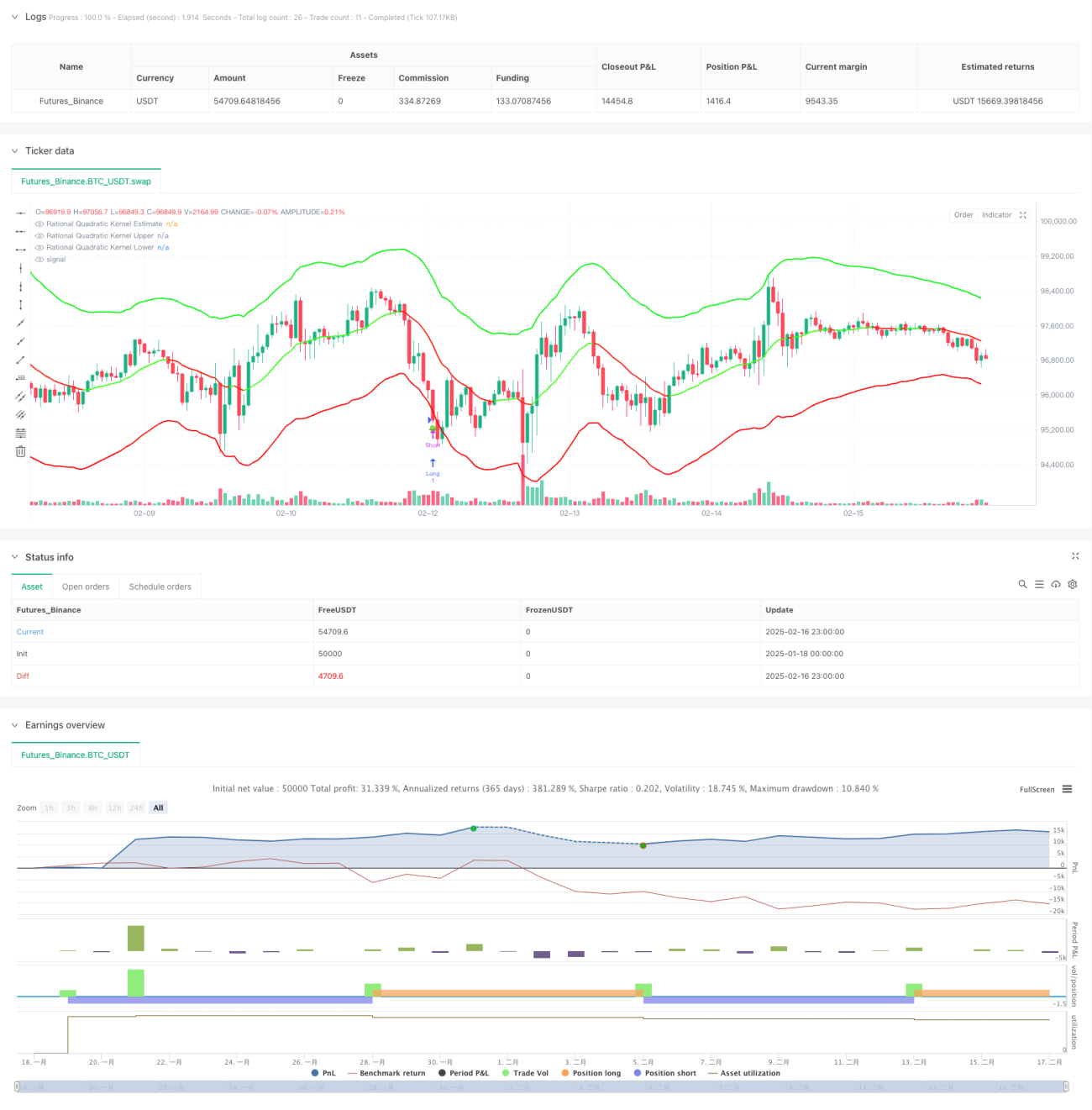

This strategy is an adaptive trend following system that combines Nadaraya-Watson kernel regression with ATR dynamic bands. It predicts price trends using rational quadratic kernel function and identifies trading opportunities through ATR-based dynamic support and resistance bands. The system achieves precise market modeling through configurable lookback window and weighting parameters.

Strategy Principle

The core of the strategy is non-parametric kernel regression based on the Nadaraya-Watson method, using a rational quadratic kernel function to smooth price series. The regression calculation starts from a specified bar, controlled by two key parameters: lookback window (h) and relative weighting (r). Dynamic bands are constructed using ATR indicator, with upper and lower bands being regression estimates plus/minus ATR multiples. Trading signals are triggered by price crossovers with the bands - long when price breaks below the lower band, short when it breaks above the upper band. Trend determination can be based on either rate of change or crossover mechanism, visualized through color changes.

Strategy Advantages

- Kernel regression has solid mathematical foundation, effectively capturing price trends without overfitting

- Dynamic bands adapt to market volatility, providing more reasonable support and resistance levels

- Strong parameter configurability, flexible adjustment for different market characteristics

- Flexible trend identification mechanism, choice between smooth or sensitive modes

- Intuitive visualization, clear trading signals

Strategy Risks

- Improper parameter selection may lead to overfitting or lag

- May generate excessive trading signals in ranging markets

- Unreasonable ATR multiplier settings can result in stop-loss being too wide or too narrow

- False signals may occur during trend transitions

It is recommended to optimize parameters through historical backtesting and combine with other indicators for confirmation.

Strategy Optimization Directions

- Incorporate volume indicators for trend confirmation

- Develop adaptive parameter optimization mechanism

- Add trend strength filter to reduce false signals in ranging markets

- Optimize stop-loss and take-profit mechanism to improve risk-reward ratio

- Consider adding market environment classification to use different parameters in different markets

Summary

This strategy combines statistical learning methods with technical analysis to build a trading system with solid theoretical foundation and strong practicality. Its adaptive features and configurability enable it to adapt to different market environments, but attention needs to be paid to parameter optimization and risk control when using it. Through continuous improvement and optimization, this strategy has the potential to play an important role in practical trading.

- 1