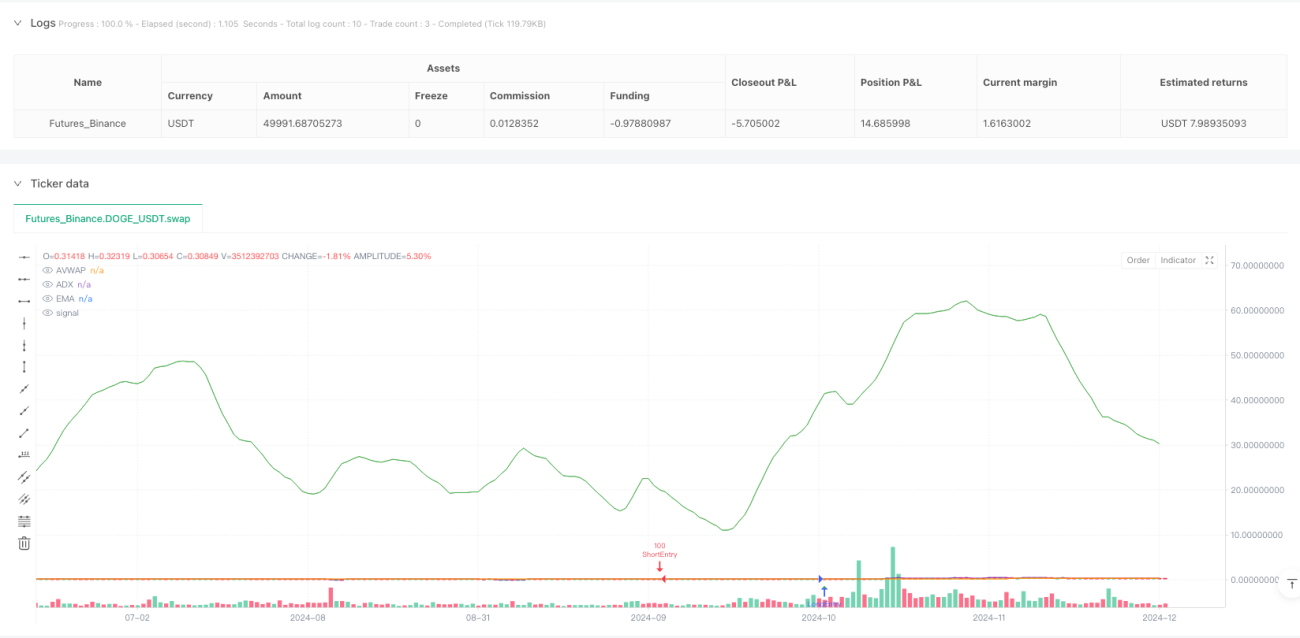

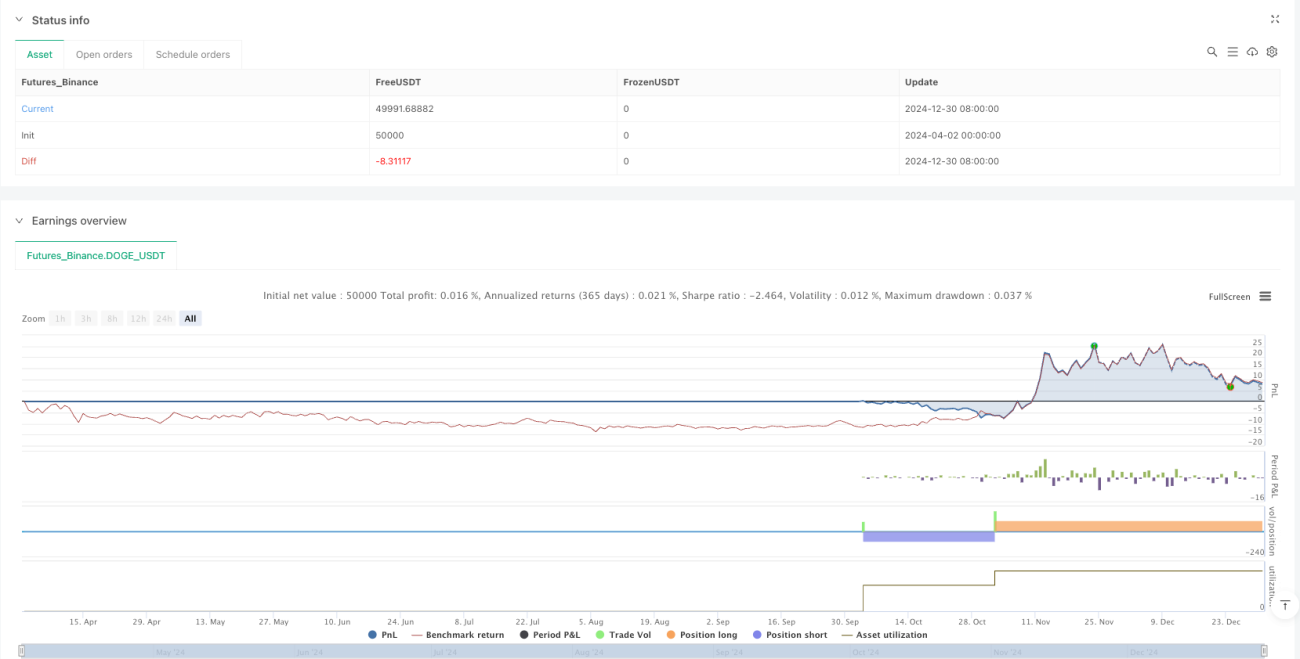

Overview

This is a complex multi-indicator trading strategy that combines Volume Weighted Average Price (AVWAP), Fixed Range Volume Profile (FRVP), Exponential Moving Average (EMA), Relative Strength Index (RSI), Average Directional Index (ADX), and Moving Average Convergence Divergence (MACD) to identify high-probability trading opportunities through indicator confluence.

Strategy Principle

The strategy determines entry signals through multiple conditions:

- Price crossing with AVWAP

- Price position relative to EMA

- RSI strength assessment

- MACD trend momentum

- ADX trend strength confirmation

- Volume filter

The strategy focuses on Asian, London, and New York trading sessions, which typically have better liquidity and more reliable trading signals. Entry logic includes both long and short modes, with a gradient take-profit and stop-loss mechanism.

Strategy Advantages

- Multi-indicator combination improving signal accuracy

- Dynamic volume filtering to avoid low-liquidity trades

- Flexible take-profit and stop-loss strategy

- Optimization based on different trading sessions

- Dynamic risk management mechanism

- Visualization signals to assist decision-making

Strategy Risks

- Increased signal complexity due to multiple indicators

- Potential overfitting in backtesting data

- Potential performance instability under different market conditions

- Trading costs and slippage may affect actual returns

Strategy Optimization Directions

- Introduce machine learning algorithms for dynamic parameter adjustment

- Increase trading session adaptability

- Optimize take-profit and stop-loss strategies

- Add more filtering conditions

- Develop a universal strategy model across different instruments

Summary

This is a highly customized and multi-dimensional trading strategy that attempts to improve trading signal quality and accuracy by integrating multiple technical indicators and trading session characteristics. The strategy demonstrates the complexity of indicator confluence and dynamic risk management in quantitative trading.

/*backtest

start: 2024-04-02 00:00:00

end: 2024-12-31 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=6

strategy("FRVP + AVWAP by Grok", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// User Inputs- 1