Parametric Multiplier Strategy: Multi-Indicator Market Rhythm Tracker

🎯 What Makes This Strategy Special?

You know what? This strategy is like installing a "super radar" for the market! Instead of simply looking at one or two indicators, it combines 9 different technical indicators like a band, where each indicator is an "instrument." The strategy only generates trading signals when they play harmonious "notes" together. Imagine having 9 experts whispering advice in your ear simultaneously, and you only act when most of them agree!

📊 Core Mechanism Revealed

Here's the key point! The essence of this strategy lies in the "parametric multiplier" concept. It first normalizes indicators like RSI, ADX, momentum, ROC, ATR, volume, acceleration, and slope to the same scale, then multiplies them together to get a "comprehensive strength value." It's like cooking - every seasoning has its optimal proportion, and this strategy helps you find the perfect recipe for various market "seasonings"! When the comprehensive strength value crosses its moving average, that's the optimal entry timing.

🔧 Customizable Trading Weapon

What's the coolest feature of this strategy? You can combine components like building blocks! Don't want to use a certain indicator? Just turn it off. Want to adjust period parameters? It's up to you. There's even an SMA trend filter to help you avoid the pitfall of counter-trend trading. This is like a "trading strategy DIY toolkit" that lets you adjust configurations based on different market environments.

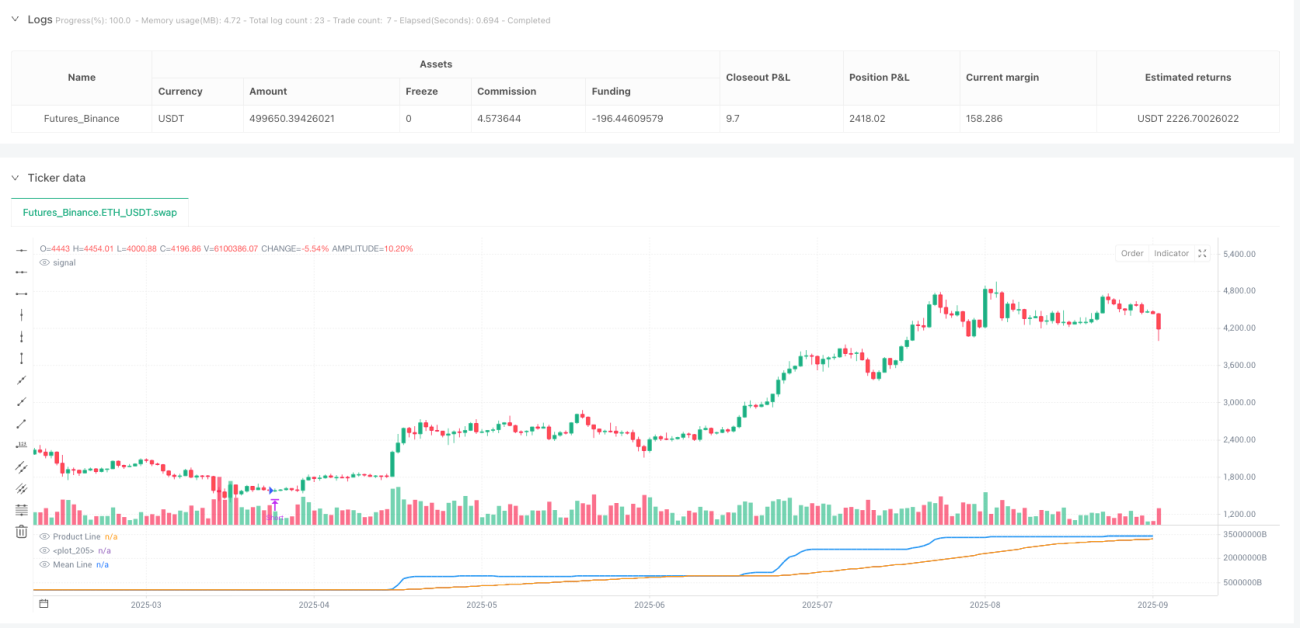

⚡ Practical Application Guide

Here's your pitfall avoidance guide! This strategy is particularly suitable for mixed oscillating and trending market environments. Go long when the blue product line crosses above the orange mean line, and go short when it crosses below. The strategy thoughtfully includes automatic position closing mechanisms to prevent you from stubbornly holding positions when reverse signals appear. Remember, enabling the trend filter helps you navigate major trends with ease, while disabling it captures more short-term opportunities!

//@version=5

strategy("Parametric Multiplier Backtester", shorttitle="PMB", overlay=false)

// Author: Script_Algo

// License: MIT

// Permission is hereby granted, free of charge, to any person obtaining a copy

// of this software and associated documentation files (the "Software"), to deal

// in the Software without restriction, including without limitation the rights

// to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

// copies of the Software, subject to the following conditions:

// The above copyright notice and this permission notice shall be included in

// all copies or substantial portions of the Software.- 1