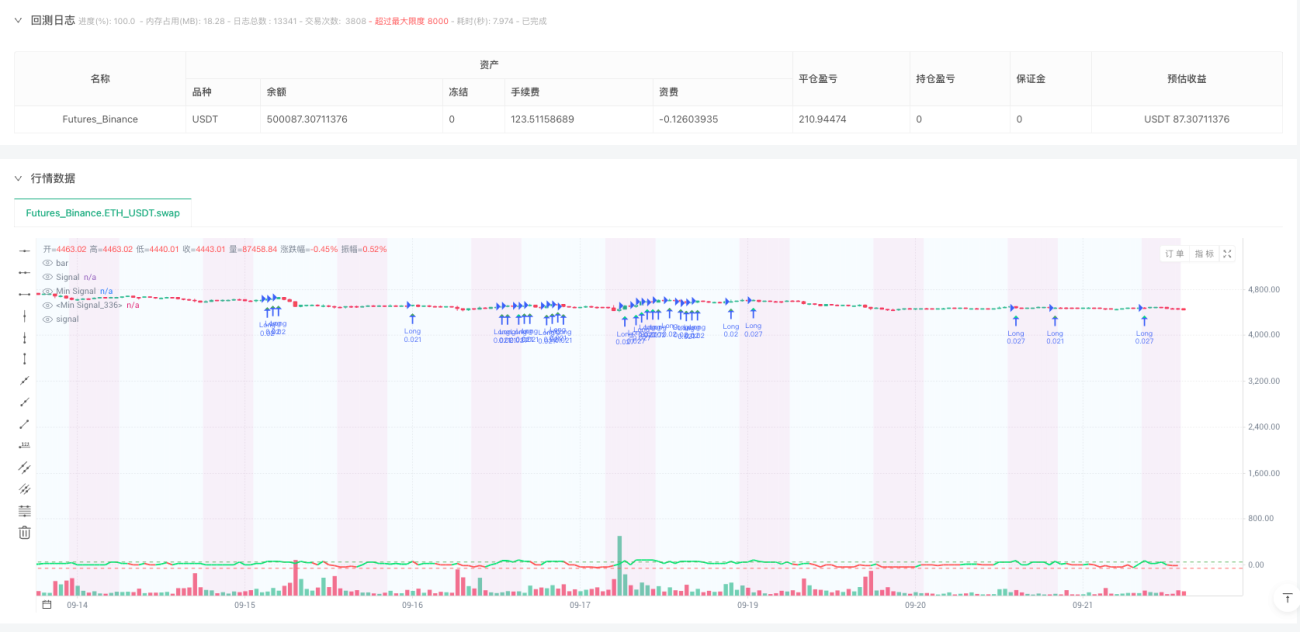

🎯 Núcleo de la estrategia: atacar el mercado de fin de semana con dinero inteligente

¿Sabías que mientras los grandes tiburones de Wall Street están de vacaciones los fines de semana, el mercado cripto esconde secretos? ¡Esta estrategia funciona como un guardia nocturno, saliendo a aprovechar las oportunidades justo cuando los inversores institucionales "se retiran"!

¡Punto clave! Esta estrategia solo opera los sábados y domingos, especialmente en el período UTC de 0 a 8 horas del domingo. ¿Por qué? Porque en ese momento la liquidez es relativamente baja y la eficacia del análisis técnico es mayor, como cuando es más fácil escuchar sonidos sutiles en una biblioteca silenciosa.

📊 Fusión de múltiples indicadores: no es un esfuerzo individual

Esta estrategia es como armar a los Vengadores:

- RSI (período 8): captura rápidamente señales de sobrecompra/sobreventa

- MACD (8,17,9): confirma el momentum de la tendencia

- Bandas de Bollinger (20, 2.5): identifica zonas de precios extremos

- Divergencia CVD: descubre la verdadera intención del dinero inteligente

Guía para evitar errores: un solo indicador es como ver una película solo, es fácil dejarse engañar por la trama. ¡Confirmar con múltiples indicadores es como verla con amigos, ¡puedes escuchar diferentes puntos de vista!

💰 Gestión inteligente de capital: hasta 500 dólares pueden funcionar

¡Aquí viene la parte más interesante! Este sistema está diseñado para capitales pequeños:

- Mínimo 120 dólares por operación: no te hará apostar todo

- Máximo 4 posiciones concurrentes: diversifica el riesgo, no pongas todos los huevos en una canasta

- Apalancamiento dinámico de 5-20x: se ajusta automáticamente según la volatilidad del mercado

Es como conducir: en una autopista se puede ir más rápido, en calles estrechas hay que ir despacio. El sistema ajusta el tamaño de las posiciones según las características de riesgo de cada criptomoneda.

🛡️ Control de riesgos: más preocupado que tu madre

Mecanismo de triple protección:

- Límite de pérdida diaria del 5%: ¿perdiste mucho hoy? Vuelve mañana

- Límite de pérdida del fin de semana del 15%: incluso si te excedes el fin de semana, hay un límite

- Detenerse tras 4 pérdidas consecutivas: evita el trading emocional

Sistema de freno de emergencia: si las pérdidas de la cuenta superan el 30%, se detienen inmediatamente todas las operaciones. Es como el sistema ABS de un coche, ¡puede salvar vidas en momentos críticos!

- 1