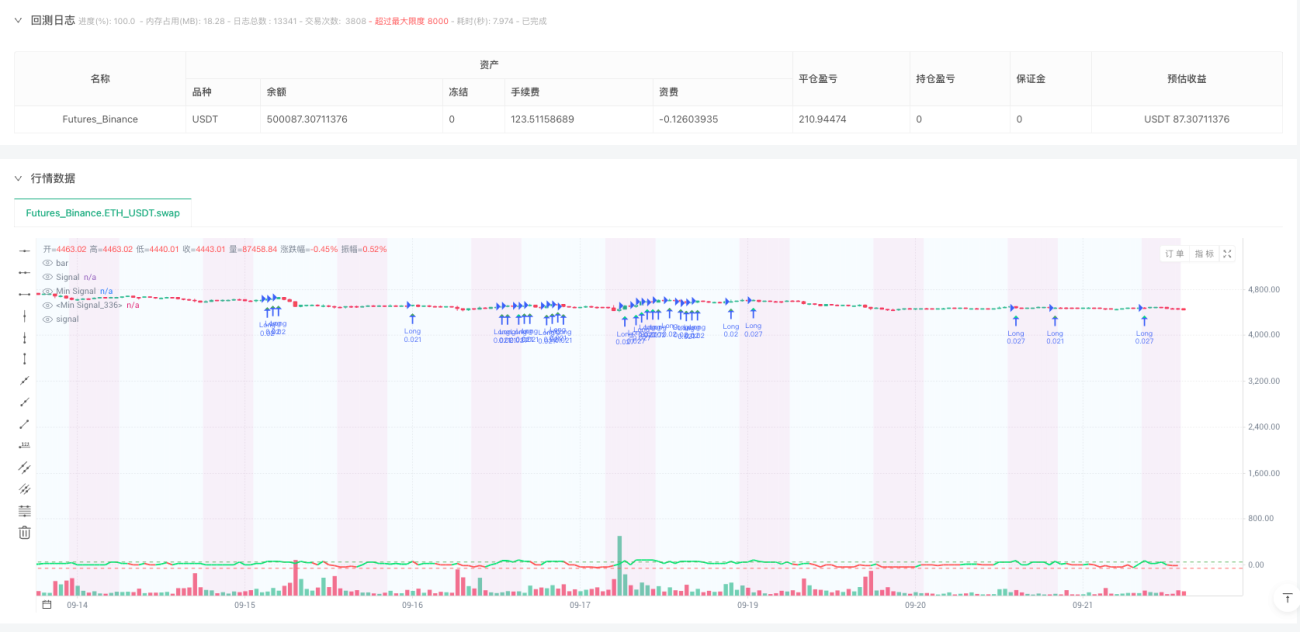

🎯 Strategy Core: Smart Money Weekend Hunting

You know what? While Wall Street bigshots are enjoying their weekends, the crypto market is full of hidden opportunities! This strategy works like a night security guard, specifically hunting for profits when institutional investors are "off duty."

Key Point! This strategy only trades on weekends, especially during Sunday 0-8 UTC. Why? Because liquidity is relatively lower during these times, making technical analysis more effective - like hearing subtle sounds more clearly in a quiet library.

📊 Multi-Indicator Fusion: Not Fighting Alone

This strategy assembles like an Avengers team:

- RSI(8-period): Quickly captures overbought/oversold signals

- MACD(8,17,9): Confirms trend momentum

- Bollinger Bands(20,2.5): Identifies price extreme zones

- CVD Divergence: Discovers smart money's true intentions

Pitfall Guide: Single indicators are like watching movies alone - easy to be misled by the plot. Multi-indicator confirmation is like watching with friends, hearing different perspectives!

💰 Smart Capital Management: $500 Can Play Big

Here's the most interesting part! This system is designed for small capital:

- Minimum $120 per trade: Won't let you go all-in

- Maximum 4 concurrent positions: Risk diversification, not putting all eggs in one basket

- 5-20x dynamic leverage: Auto-adjusts based on market volatility

Like driving a car - you can go faster on highways, but need to slow down in alleys. The system adjusts position sizes based on different coins' risk characteristics.

🛡️ Risk Control: More Caring Than Your Mom

Triple Protection Mechanism:

- Daily loss limit 5%: Lost too much today? Try again tomorrow

- Weekend loss limit 15%: Even weekend disasters have boundaries

- Stop after 4 consecutive losses: Prevents emotional trading

Emergency Brake System: If account loses over 30%, immediately stops all trading. This is like a car's ABS system - can save your life at critical moments!

- 1