Estrategia de multiplicador de parámetros: metrónomo de mercado con fusión de múltiples indicadores

🎯 ¿Qué estrategia mágica es esta?

¿Sabías? ¡Esta estrategia es como instalarle un "súper radar" al mercado! No se limita a mirar uno o dos indicadores, sino que combina 9 indicadores técnicos diferentes como si fueran una orquesta. Cada indicador es un "instrumento", y solo cuando tocan una "nota" armoniosa, la estrategia emite una señal de trading. Imagina que tienes 9 expertos dándote consejos al mismo tiempo, ¡y solo actúas cuando la mayoría está de acuerdo!

📊 El gran secreto del principio fundamental

¡Atención a esto! La esencia de esta estrategia reside en el concepto de "multiplicador de parámetros". Estandariza indicadores como RSI, ADX, Momentum, ROC, ATR, Volumen, Aceleración y Pendiente a una misma escala, y luego los multiplica para obtener un "valor de fuerza combinada". Es como cocinar: cada especia tiene su proporción óptima, ¡y esta estrategia encuentra la combinación perfecta de todas las "especias" del mercado! Cuando el valor de fuerza combinada cruza su media móvil, es el mejor momento para entrar.

🔧 Una herramienta de trading personalizable

¿Lo más genial de esta estrategia? ¡Puedes combinarla libremente como si fueran bloques de construcción! ¿No quieres usar un indicador? Simplemente desactívalo. ¿Quieres ajustar el período de los parámetros? Como prefieras. Incluso tiene un filtro de tendencia SMA para ayudarte a evitar las grandes trampas de operar en contra de la tendencia. Es como un "kit de herramientas de bricolaje para estrategias de trading" que te permite ajustar la configuración según las diferentes condiciones del mercado.

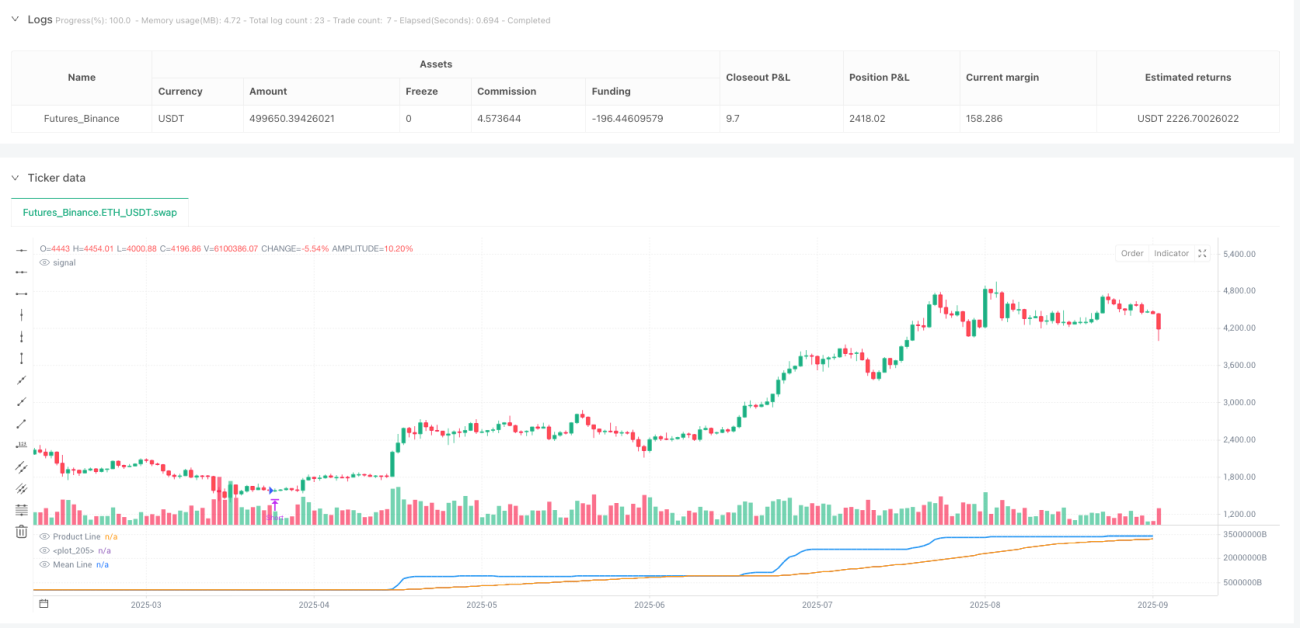

⚡ Guía práctica de aplicación

¡Aquí vienen los consejos para evitar errores! Esta estrategia es especialmente adecuada para mercados mixtos de rango y tendencia. Cuando la línea azul del producto cruza hacia arriba la línea naranja de la media móvil, se abre una posición larga; cuando cruza hacia abajo, se abre una posición corta. La estrategia también incluye un mecanismo de cierre automático para evitar que te quedes atrapado en una posición cuando aparece una señal contraria. Recuerda: activar el filtro de tendencia te permite navegar con soltura en las grandes tendencias, mientras que desactivarlo te permite capturar más oportunidades a corto plazo.

//@version=5

strategy("Parametric Multiplier Backtester", shorttitle="PMB", overlay=false)

// Author: Script_Algo

// License: MIT

// Permission is hereby granted, free of charge, to any person obtaining a copy

// of this software and associated documentation files (the "Software"), to deal

// in the Software without restriction, including without limitation the rights

// to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

// copies of the Software, subject to the following conditions:

// The above copyright notice and this permission notice shall be included in

// all copies or substantial portions of the Software.- 1