Stratégie de suivi de tendance adaptative basée sur la régression par noyau et les bandes dynamiques ATR

Aperçu

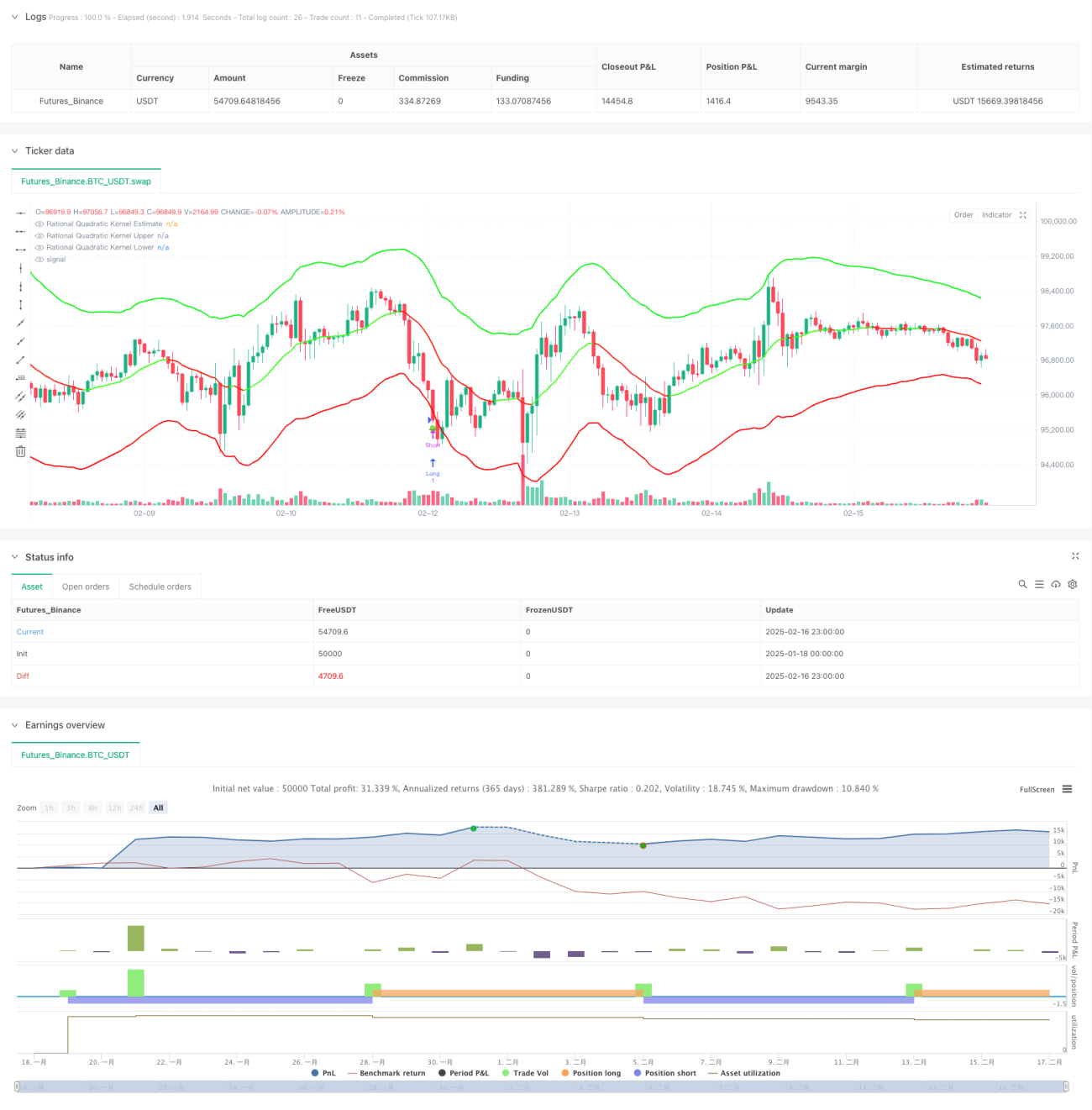

Cette stratégie est un système de suivi de tendance adaptatif combinant la régression à noyau de Nadaraya-Watson avec des bandes dynamiques basées sur l'ATR. Elle prédit la tendance des prix à l'aide d'une fonction de noyau quadratique rationnel et utilise des bandes de support et de résistance dynamiques fondées sur l'ATR pour identifier les opportunités de trading. Le système modélise le marché avec précision grâce à des paramètres configurables de fenêtre de rétrospection et de pondération.

Principe de la stratégie

Le cœur de la stratégie repose sur la régression à noyau non paramétrique de Nadaraya-Watson, qui lisse la série de prix à l'aide d'une fonction de noyau quadratique rationnel. La régression commence à partir d'une barre de départ définie et utilise deux paramètres clés – la fenêtre de rétrospection (h) et la pondération relative (r) – pour contrôler le degré d'ajustement. En parallèle, des bandes dynamiques sont construites à partir de l'indicateur ATR : les bandes supérieure et inférieure correspondent à la valeur estimée de la régression plus ou moins un multiple de l'ATR. Le système génère des signaux de transaction lors du croisement du prix avec les bandes – lorsque le prix franchit la bande inférieure, on prend une position longue ; lorsqu'il franchit la bande supérieure, on prend une position courte. L'identification de la tendance peut être basée sur le taux de variation du prix ou sur un mécanisme de croisement, et est visualisée par un changement de couleur.

Avantages de la stratégie

- La méthode de régression à noyau possède une base mathématique solide, permettant de capter efficacement la tendance des prix sans surajustement.

- Les bandes dynamiques s'adaptent automatiquement à la volatilité du marché, offrant des niveaux de support et de résistance plus pertinents.

- Les paramètres sont hautement configurables, ce qui permet de s'adapter facilement aux différentes caractéristiques du marché.

- Le mécanisme d'identification de tendance est flexible : on peut choisir entre un mode lissé et un mode sensible.

- La visualisation est intuitive et les signaux de trading sont clairs.

Risques de la stratégie

- Un choix inapproprié des paramètres peut entraîner un surajustement ou un retard.

- Sur un marché en range (volatile), la stratégie peut générer un excès de signaux.

- Un mauvais réglage du multiple de l'ATR peut conduire à un stop-loss trop large ou trop étroit.

- Pendant les périodes de retournement de tendance, des signaux trompeurs peuvent apparaître.

Il est recommandé d'optimiser les paramètres par un backtest historique et d'utiliser d'autres indicateurs comme confirmation auxiliaire.

Orientations d'optimisation

- Introduire un indicateur de volume comme confirmation de tendance.

- Développer un mécanisme d'optimisation adaptative des paramètres.

- Ajouter un filtre de force de tendance pour réduire les faux signaux sur les marchés en range.

- Améliorer les mécanismes de stop-loss et de take-profit pour améliorer le rapport risque/récompense.

- Envisager d'intégrer une classification des conditions de marché afin d'utiliser différents paramètres selon l'environnement.

Conclusion

Cette stratégie combine les méthodes d'apprentissage statistique avec l'analyse technique pour construire un système de trading doté de fondations théoriques solides et d'une grande utilité pratique. Ses propriétés adaptatives et sa configurabilité lui permettent de s'adapter à différents environnements de marché, mais il convient de prêter attention à l'optimisation des paramètres et à la gestion des risques lors de son utilisation. Grâce à des améliorations et des optimisations continues, cette stratégie a le potentiel de jouer un rôle important dans le trading réel.

- 1