EMA inFusion Pro Stratégie de fusion de données multi-sources

🎯 Point fort principal de la stratégie : une stratégie EMA qui ne se limite pas au prix

Saviez-vous que la plupart des gens utilisent l'EMA uniquement pour le prix ? Mais ce qui rend cette stratégie puissante, c'est qu'elle peut calculer l'EMA à partir de 6 sources de données différentes ! C'est comme cuisiner : on n'utilise pas seulement du sel, mais aussi du sucre, du vinaigre, de la sauce soja, pour obtenir des signaux de trading plus riches.

À retenir ! Ces 6 sources de données incluent : le prix normal, le volume, le taux de variation, le prix moyen des bougies (Heikin-Ashi), le volume moyen des bougies, le taux de variation moyen des bougies. Chacune offre une perspective de marché différente !

📊 Système de triple filtre : des signaux plus précis

Cette stratégie ne donne pas de signaux au hasard ! Elle dispose de trois niveaux de « contrôle de sécurité » :

1ᵉʳ niveau : Tendance EMA 📈

Comme une météo, on détermine d'abord la tendance générale : beau ou pluvieux.

2ᵉ niveau : Filtre de force ADX 💪

L'ADX est comme un instrument mesurant la force du vent. Le signal n'est émis que si la tendance est suffisamment forte (par défaut au-dessus de 25). Cela évite de se faire piéger dans un marché en range !

3ᵉ niveau : Confirmation par le volume 🔊

Une augmentation soudaine du volume, c'est comme si l'action « parlait fort », preuve que le signal est sérieux, pas une blague.

🎮 Trois modes de sortie : adaptés à différents styles de trading

Le plus agréable, c'est que cette stratégie propose 3 modes de sortie, comme les niveaux de difficulté facile, normal, difficile dans un jeu :

Mode 1 : Sortie sur signal inverse 🔄

Le plus simple : un signal long ferme la position short et ouvre une position long, un signal short ferme la position long et ouvre une position short.

Mode 2 : Stop-Loss/Take-Profit dynamique basé sur l'ATR 📏

Ajustement automatique en fonction de la volatilité du marché : stop plus large quand la volatilité est élevée, plus serré quand elle est faible.

Mode 3 : Stop-Loss/Take-Profit fixe en pourcentage 📊

Le plus compréhensible : prendre profit à 2 %, stop-loss à 1,5 % (paramétrable).

🚀 Conseils pratiques d'application

Périodes adaptées : Trading à court/moyen terme, particulièrement adapté aux marchés avec une certaine volatilité.

Pièges à éviter : Attention dans les marchés en range, il est conseillé d'activer le filtre ADX.

Utilisation avancée : Vous pouvez essayer différentes sources de données ; la source volume est particulièrement efficace lors des cassures avec volume !

Le plus grand avantage de cette stratégie est sa flexibilité : vous pouvez choisir la source de données et le mode de sortie les plus adaptés selon les conditions de marché. Rappelez-vous : il n'existe pas de stratégie parfaite, seulement celle qui est la mieux adaptée au marché actuel !

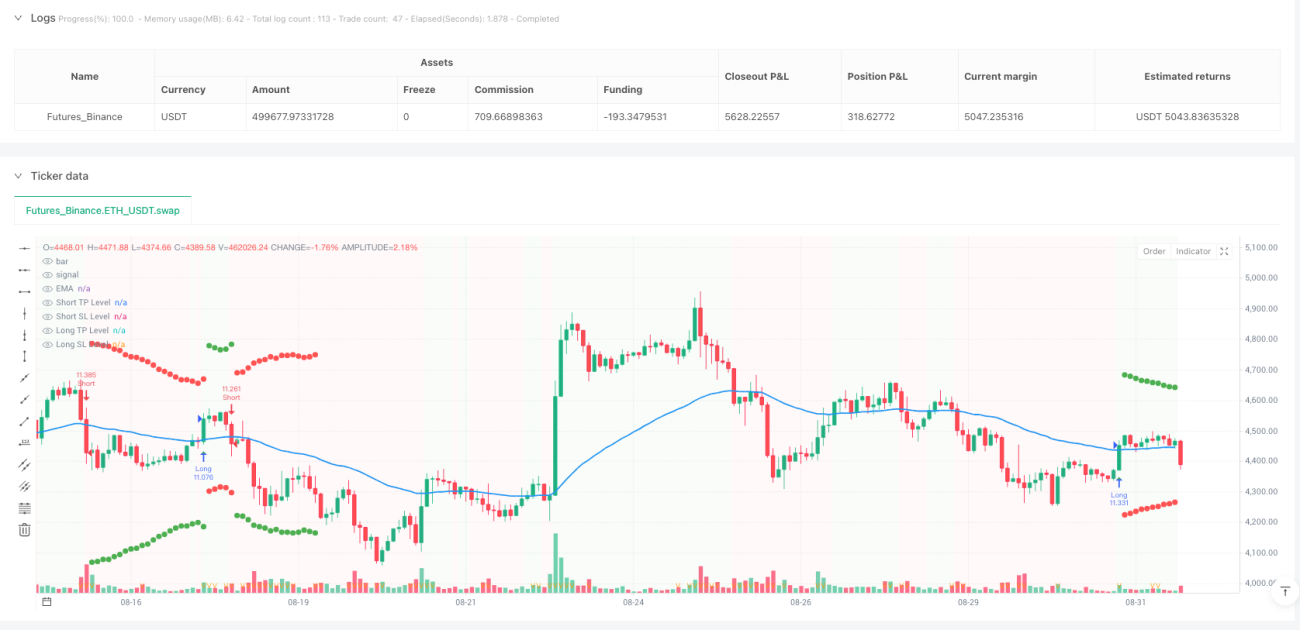

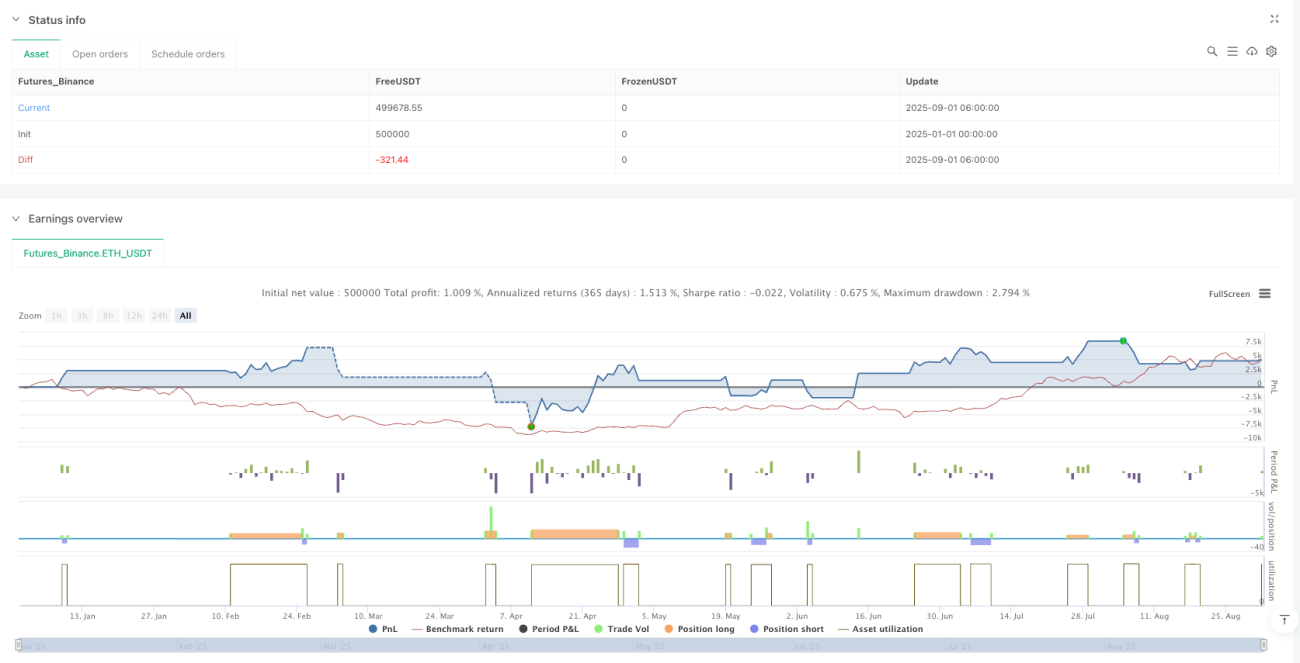

/*backtest

start: 2025-01-01 00:00:00

end: 2025-09-01 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT","balance":500000}]

*/

//@version=5

//@fenyesk

strategy("EMA inFusion Pro - Source Selection", overlay=true, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

- 1