Protocole du moteur de volatilité

Ce n'est pas un simple DCA, c'est un moteur de volatilité intelligent

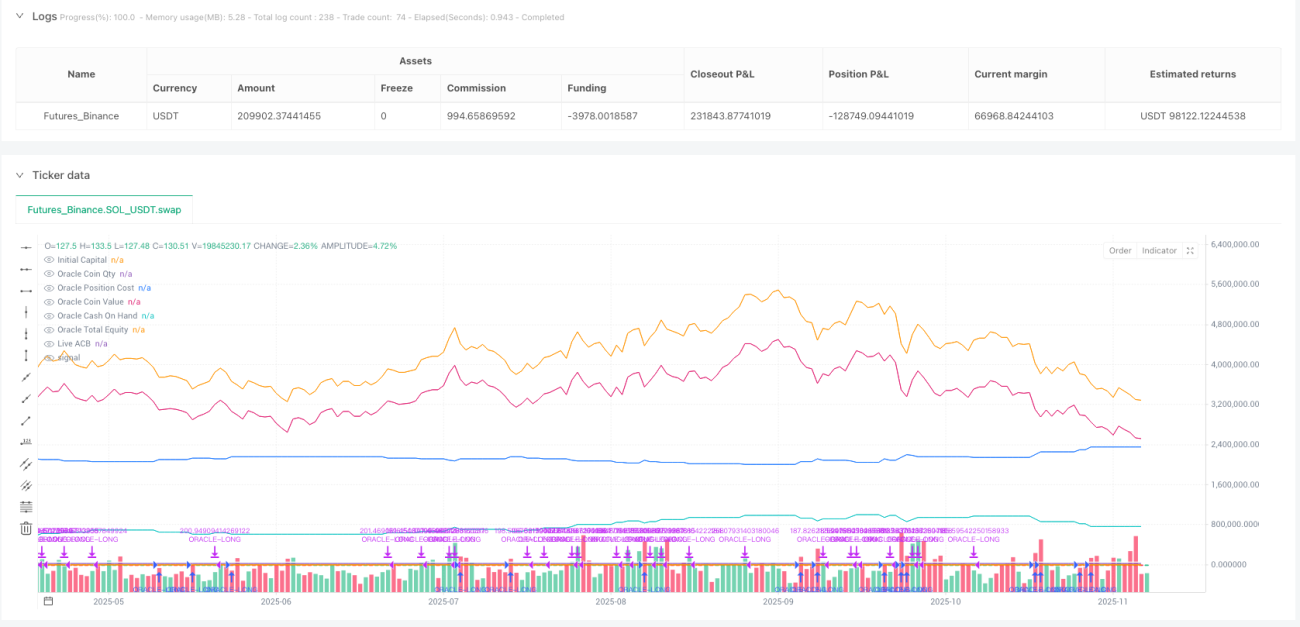

Les données de backtest disqualifient directement le DCA traditionnel : achat déclenché par une baisse de 5 %, vente déclenchée par une hausse de 3,9 %, mais le point clé est que le moteur de volatilité ajuste dynamiquement le seuil d'achat en fonction de l'ATR. Plus la volatilité du marché est élevée, plus le seuil d'achat est élevé, avec un ajustement maximum de 40 %. Cela signifie que pendant les périodes de forte volatilité, la stratégie attend des baisses plus importantes avant d'entrer.

Le problème de la stratégie DCA traditionnelle est qu'elle achète aveuglément, alors que la logique centrale de ce protocole est de ne tirer que dans les fenêtres d'opportunité réelles. Il calcule la volatilité actuelle via l'ATR(14), puis ajuste dynamiquement le paramètre longThreshPct. Par exemple, un achat normal à une baisse de 5 %, mais si la volatilité actuelle atteint 20 %, le seuil d'achat réel sera relevé à 6 %.

8 configurations prédéfinies, chacune avec des objectifs de rendement clairs

Mode d'accumulation cyclique BTC : achat à une baisse de 5 %, position de 6 %, montant fixe de 500 \(, adapté aux détenteurs à long terme.

**Mode d'arbitrage à court terme BTC** : achat à une baisse de 3,1 %, position de 10 %, montant fixe de 6 000 \), seuil de vente à 75 % de profit.

Moissonnage de volatilité ETH : achat à une baisse de 4,5 %, position de 15 %, achat autorisé en dessous du prix de revient, seuil de profit à 30 %.

Chaque configuration a été validée par des backtests, ce ne sont pas des paramètres décidés à l'emporte-pièce. Le seuil de profit de 35 % pour SOL, et de 10 % pour XRP, ces différences reflètent les caractéristiques de volatilité et les écarts de liquidité des différents actifs.

Mécanisme de sceau de cluster : résoudre le plus grand problème du DCA

Le plus grand problème du DCA traditionnel est de ne pas savoir quand arrêter d'acheter. Ce protocole le résout avec le « sceau de cluster » : soit le prix augmente de 3,9 % par rapport au coût moyen, soit après 10 cycles consécutifs sans opportunité d'achat éligible, le cluster d'accumulation actuel est scellé.

La ligne de coût moyen après le sceau devient la référence de base pour la vente. La vente n'est déclenchée que lorsque le prix dépasse la ligne de coût scellée + seuil de profit (de 30 % à 75 %). Cela évite les achats sans fin et les prises de bénéfices prématurées.

Le mécanisme de colonne silencieuse est un coup de génie : si après 10 cycles consécutifs aucune condition d'achat n'est déclenchée, cela signifie que le marché s'est stabilisé et qu'il faut se préparer à moissonner plutôt qu'à continuer d'accumuler.

Effet volant d'inertie : faire en sorte que les profits servent au prochain achat

En activant le mode volant d'inertie, les profits de chaque vente sont réinjectés dans la réserve de liquidités, augmentant les munitions pour le prochain achat. Ce n'est pas un simple intérêt composé, mais une stratégie qui permet d'obtenir une puissance de feu plus forte en période haussière.

Exemple : capital initial de 100 000 \(, premier cycle d'accumulation avec un profit de 20 %, après la vente la réserve passe à 120 000 \). Lors du prochain achat, la position de 6 % correspond à 7 200 \( au lieu de 6 000 \). Au fil du temps, cet effet boule de neige amplifie considérablement les rendements.

Mais le volant d'inertie a aussi un coût : en fin de marché haussier, la réserve de liquidités peut devenir trop importante et entraîner des achats excessifs, d'où la nécessité de limiter strictement le montant maximum d'achat par transaction.

Contrôle des risques : triple mécanisme de sécurité

Première barrière : contrôle des achats au-dessus du prix de revient. Possibilité de n'acheter qu'en dessous du coût moyen, pour éviter de courir après les hausses.

Deuxième barrière : montant minimum. Chaque achat/vente a un montant minimum en dollars pour éviter les transactions insignifiantes.

Troisième barrière : régulation du moteur de volatilité. Augmentation automatique du seuil d'achat en période de forte volatilité, baisse en période de faible volatilité.

Mais cette stratégie donne des résultats moyens dans un marché en range. Si le marché stagne horizontalement sur une longue période, il est impossible de déclencher des achats sur forte baisse ni d'atteindre le seuil de profit pour vendre, et les fonds restent bloqués à long terme.

Conseils pratiques : bien choisir son marché est crucial

Ce protocole est le plus adapté aux marchés avec une tendance claire, en particulier les cycles des crypto-monnaies. Il est optimal pour accumuler en fin de marché baissier et moissonner en milieu de marché haussier.

Ne pas l'utiliser dans les cas suivants : 1) marchés actions à forte volatilité en range, 2) marchés des changes sans tendance claire, 3) petites crypto-monnaies à très faible liquidité.

Les backtests historiques montrent un rendement ajusté au risque supérieur au DCA simple, mais cela ne garantit pas une rentabilité future. Toute stratégie quantitative comporte un risque de défaillance et nécessite une surveillance et un ajustement continus.

//@version=6

// ============================================================================

// ORACLE PROTOCOL — ARCH PUBLIC clone (Standalone) — CLEAN-PUB STYLE (derived)

// Variant: v1.9v-standalone (publish-ready) 25/11/2025

// Notes:

// - Keeps your v1.9v canonical script intact (this is a separate modified copy).

// - Single exit mode: ProfitGate + Candle (per-candle) — no selector.

// - Live ACB plot toggle only (sealed ACB still operates internally but is not shown).

// - No freeze-point markers plotted.

// - Sizing: flywheel dynamic sizing remains the primary source but fixed-dollar entry

// and min-$ overrides remain available (as in Arch public PDFs/screenshots).

// - Volatility Engine (VE) applies ONLY to entries; exit-side VE removed.- 1