एकाधिक समय ढाँचे में ट्रेंड अनुसरण एवं ATR स्टॉप-लॉस एवं टेक-प्रॉफिट रणनीति

अवलोकन

यह एक ट्रेंड-फॉलोइंग ट्रेडिंग रणनीति है जो यूटी बॉट और 50-अवधि एक्सपोनेंशियल मूविंग एवरेज (ईएमए) को जोड़ती है। यह रणनीति मुख्य रूप से 1 मिनट के टाइमफ्रेम पर अल्पकालिक ट्रेडिंग करती है, साथ ही दिशा फ़िल्टर के रूप में 5 मिनट के टाइमफ्रेम की ट्रेंड लाइन का उपयोग करती है। रणनीति स्टॉप लॉस की स्थिति की गतिशील गणना के लिए एटीआर इंडिकेटर का उपयोग करती है और लाभ को अनुकूलित करने के लिए दोहरे टेक-प्रॉफिट लक्ष्य निर्धारित करती है।

रणनीति सिद्धांत

रणनीति का मुख्य तर्क निम्नलिखित प्रमुख घटकों पर आधारित है:

- गतिशील सपोर्ट और रेजिस्टेंस लेवल की गणना के लिए यूटी बॉट का उपयोग करना

- 5 मिनट के टाइमफ्रेम पर 50-अवधि के ईएमए का उपयोग करके समग्र ट्रेंड दिशा निर्धारित करना

- विशिष्ट एंट्री पॉइंट निर्धारित करने के लिए 21-अवधि के ईएमए और यूटी बॉट सिग्नल को जोड़ना

- एटीआर गुणकों के माध्यम से गतिशील ट्रेलिंग स्टॉप लॉस सेट करना

- 0.5% और 1% पर दो टेक-प्रॉफिट लक्ष्य निर्धारित करना, प्रत्येक पर 50% पोजीशन बंद करना

जब कीमत यूटी बॉट द्वारा गणना किए गए सपोर्ट/रेजिस्टेंस लेवल को तोड़ती है और 21-अवधि का ईएमए यूटी बॉट के साथ क्रॉस करता है, और यदि कीमत 5 मिनट के 50-अवधि के ईएमए की सही दिशा में है, तो ट्रेडिंग सिग्नल ट्रिगर होता है।

रणनीति लाभ

- कई टाइमफ्रेम का संयोजन ट्रेडिंग विश्वसनीयता बढ़ाता है

- गतिशील एटीआर स्टॉप लॉस बाजार की अस्थिरता के अनुसार अनुकूलित हो सकता है

- दोहरे टेक-प्रॉफिट लक्ष्य लाभ और जीत दर को संतुलित करते हैं

- हीकिन आशी कैंडलस्टिक का उपयोग कुछ झूठे ब्रेकआउट को फ़िल्टर कर सकता है

- लचीली ट्रेडिंग दिशा विकल्पों का समर्थन करता है (केवल लॉन्ग, केवल शॉर्ट या द्विदिश ट्रेडिंग)

रणनीति जोखिम

- अल्पकालिक ट्रेडिंग में उच्च स्प्रेड और कमीशन लागत का सामना करना पड़ सकता है

- साइडवे मार्केट में बार-बार झूठे सिग्नल उत्पन्न हो सकते हैं

- कई शर्तों की सीमाएं कुछ संभावित ट्रेडिंग अवसरों को चूक सकती हैं

- एटीआर पैरामीटर को विभिन्न बाजारों के लिए अनुकूलित करने की आवश्यकता है

रणनीति अनुकूलन दिशाएं

- सहायक पुष्टि के रूप में वॉल्यूम इंडिकेटर जोड़ा जा सकता है

- अधिक बाजार भावना संकेतकों को शामिल करने पर विचार करें

- विभिन्न बाजार अस्थिरता विशेषताओं के लिए अनुकूली पैरामीटर विकसित करें

- ट्रेडिंग समय सत्रों के लिए फ़िल्टर जोड़ें

- अधिक बुद्धिमान पोजीशन प्रबंधन प्रणाली विकसित करें

सारांश

यह रणनीति कई तकनीकी संकेतकों और टाइमफ्रेम को मिलाकर एक पूर्ण ट्रेडिंग सिस्टम बनाती है। इसमें न केवल स्पष्ट एंट्री और एग्जिट की शर्तें शामिल हैं, बल्कि एक मजबूत जोखिम प्रबंधन तंत्र भी प्रदान करता है। हालांकि वास्तविक अनुप्रयोग में विशिष्ट बाजार स्थितियों के अनुसार पैरामीटर अनुकूलन की अभी भी आवश्यकता है, समग्र ढांचे में अच्छी व्यावहारिकता और विस्तारशीलता है।

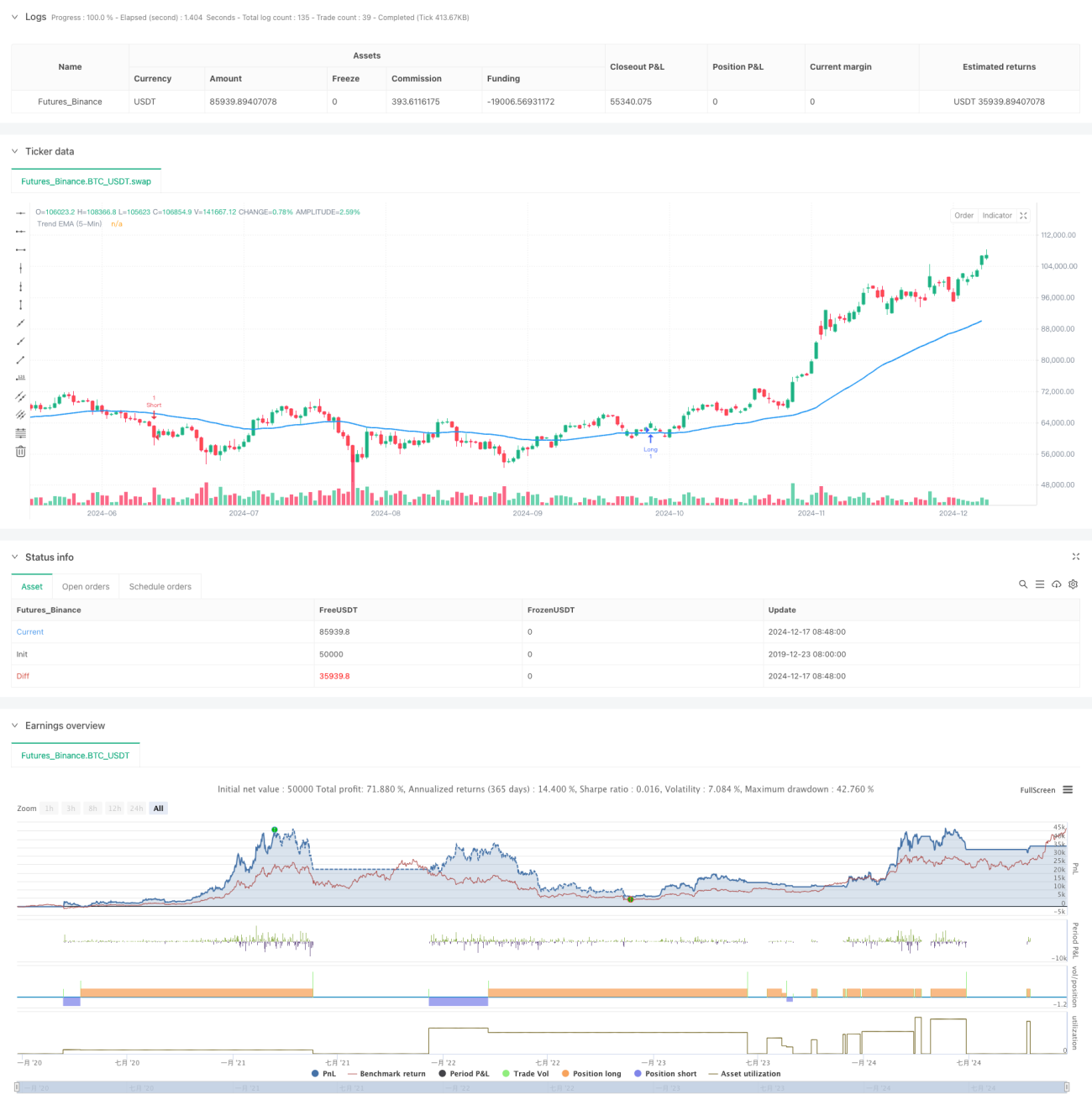

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

- 1