2

关注

502

关注者

🎯 这是什么神仙策略?20个指标齐上阵!

你知道吗?这个策略就像是给你的交易配了一个超级智能的AI助手!它同时监控20个不同的市场信号,只有当大部分指标都说"可以"的时候,才会给你交易建议。就像买房要看地段、价格、户型、交通...只有各方面都满意才下手一样!

划重点!这不是普通的单一指标策略,而是一个"多维度共振系统"。想象一下,如果只有一个朋友说某只股票好,你可能半信半疑;但如果20个专业朋友都说好,你是不是更有信心?

📊 核心武器库大揭秘

趋势识别三剑客 🗡️

- 快速EMA(5) vs 慢速EMA(13):抓住短期趋势转折

- 趋势过滤EMA(34):确认中期方向

- 主趋势EMA(89):把握大方向,不被小波动迷惑

多时间框架分析 ⏰

这个功能太赞了!策略会同时看1小时和4小时的趋势,就像你开车既要看前方路况,也要看导航的整体路线。避免了"小时间框架看涨,大时间框架看跌"的尴尬局面!

智能风险管理 🛡️

- 动态仓位调整:根据市场波动自动调整下注大小

- 分批止盈:不贪心,见好就收一部分

- 移动止损:利润保护神器

🔥 20重保险的交易逻辑

做多信号需要满足:

- 趋势向上:所有EMA呈多头排列

- 动量充足:RSI、MACD、随机RSI都给绿灯

- 成交量配合:放量上涨才是真上涨

- 市场结构健康:高点不断抬高

- 流动性支撑:关键支撑位完好

做空信号正好相反!

避坑指南 ⚠️:策略还有"布林带挤压检测",当市场过于平静时会暂停交易,避免在震荡市中被来回打脸!

💰 利润最大化的秘密武器

分批止盈策略 📈

- 第一次止盈:2倍风险回报时卖出30%仓位

- 第二次止盈:3.5倍时再卖40%仓位

- 剩余仓位:用移动止损保护,让利润奔跑

智能止损升级 🎯

达到2.5倍盈利后,止损会自动移到成本价,确保这笔交易至少不亏钱。就像给你的利润买了保险!

动态追踪止损 🏃♂️

当利润达到一定程度,止损会像影子一样跟着价格走,既保护利润又给上涨留空间。

🚀 为什么这个策略这么牛?

- 全方位覆盖:技术分析、资金管理、风险控制一个都不少

- 智能过滤:20个条件层层筛选,大大提高成功率

- 适应性强:多时间框架分析,适合不同市场环境

- 人性化设计:自动化执行,避免情绪化交易

这个策略就像是把一个经验丰富的交易团队装进了代码里,24小时不休息地为你寻找最佳交易机会!

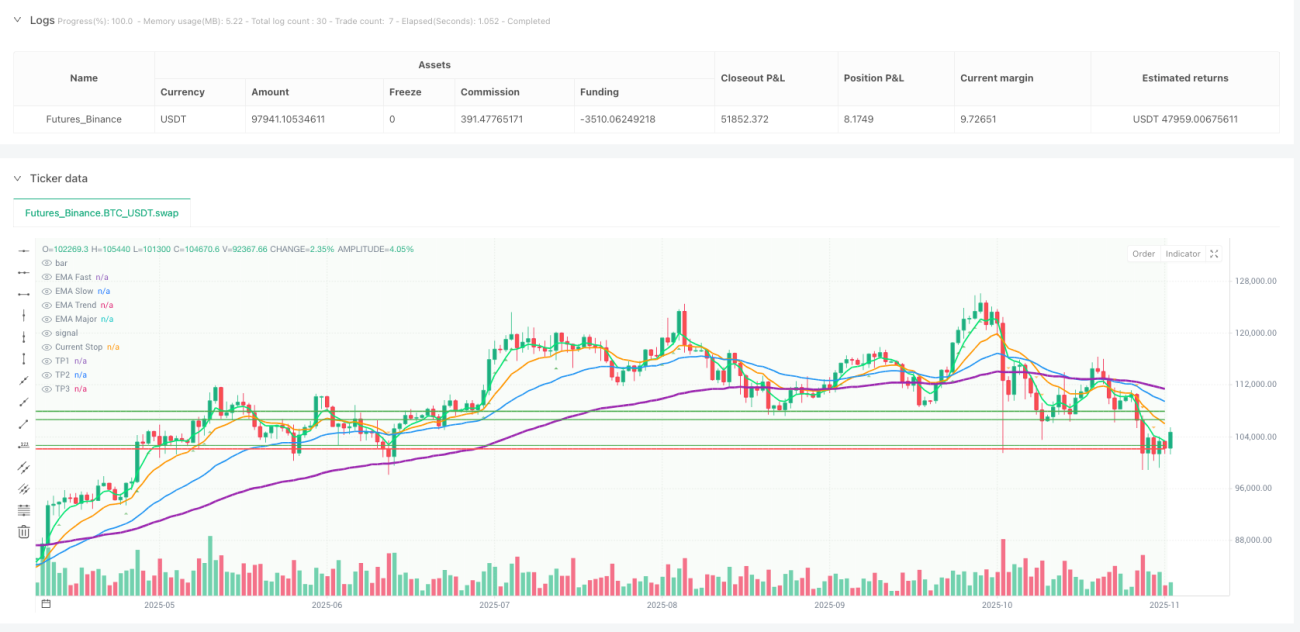

策略源码

Pine

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1