अवलोकन

बहु-संकेतक भारित स्मार्ट ट्रेडिंग रणनीति एक व्यापक मात्रात्मक ट्रेडिंग सिस्टम है जो कई तकनीकी संकेतकों के संकेतों को एकीकृत करके और विभिन्न भार देकर ट्रेडिंग निर्णय उत्पन्न करती है। यह रणनीति MACD, स्टोकेस्टिक RSI, EMA, सुपर ट्रेंड और मूविंग एवरेज क्रॉसओवर जैसे विभिन्न तकनीकी विश्लेषण उपकरणों को जोड़कर एक व्यापक ट्रेडिंग ढांचा बनाती है। सिस्टम न केवल बहु-स्तरीय लाभ-लक्ष्य और गतिशील स्टॉप-लॉस तंत्र का समर्थन करता है, बल्कि बाजार की स्थितियों के अनुसार ट्रेडिंग पैरामीटर को स्वचालित रूप से समायोजित भी कर सकता है, जिससे यह विभिन्न बाजार वातावरणों में उच्च अनुकूलनशीलता बनाए रखता है। यह रणनीति विशेष रूप से मध्यम से दीर्घकालिक व्यापारियों के लिए उपयुक्त है, और भार वितरण प्रणाली के माध्यम से ट्रेडिंग निर्णयों को अधिक मजबूत और विश्वसनीय बनाती है।

रणनीति सिद्धांत

इस रणनीति का मूल इसकी भारित संकेत प्रणाली है, जो पांच अलग-अलग उप-रणनीतियों के माध्यम से ट्रेडिंग संकेत उत्पन्न करती है:

-

MACD रणनीति: MACD लाइन और सिग्नल लाइन के क्रॉसओवर का उपयोग करके बाजार की प्रवृत्ति दिशा निर्धारित करती है। जब MACD लाइन सिग्नल लाइन को ऊपर पार करती है तो खरीद संकेत उत्पन्न होता है, और नीचे पार करने पर बिक्री संकेत उत्पन्न होता है।

-

स्टोकेस्टिक RSI रणनीति: RSI और स्टोकेस्टिक संकेतकों के लाभों को मिलाकर बाजार की ओवरबॉट/ओवरसोल्ड स्थिति की निगरानी करती है। जब स्टोकेस्टिक RSI निर्धारित ओवरसोल्ड सीमा से नीचे होता है तो खरीद संकेत उत्पन्न होता है, और ओवरबॉट सीमा से ऊपर होने पर बिक्री संकेत उत्पन्न होता है।

-

EMA ओवरबॉट/ओवरसोल्ड रणनीति: कीमत के औसत से विचलन की डिग्री की पहचान करने के लिए EMA का उपयोग करती है। जब RSI निर्धारित ओवरसोल्ड सीमा से नीचे होता है तो खरीद संकेत उत्पन्न होता है, और ओवरबॉट सीमा से ऊपर होने पर बिक्री संकेत उत्पन्न होता है।

-

सुपर ट्रेंड रणनीति: ATR गुणक के आधार पर मूल्य चैनल सेट करती है और प्रवृत्ति परिवर्तन के माध्यम से ट्रेडिंग दिशा निर्धारित करती है। जब सुपर ट्रेंड संकेतक नकारात्मक से सकारात्मक में बदलता है तो खरीद संकेत उत्पन्न होता है, और सकारात्मक से नकारात्मक में बदलने पर बिक्री संकेत उत्पन्न होता है।

-

मूविंग एवरेज क्रॉसओवर रणनीति: दो अलग-अलग अवधियों की मूविंग एवरेज के क्रॉसओवर का उपयोग करके बाजार की प्रवृत्ति निर्धारित करती है। जब अल्पकालिक एवरेज दीर्घकालिक एवरेज को ऊपर पार करती है तो खरीद संकेत उत्पन्न होता है, और नीचे पार करने पर बिक्री संकेत उत्पन्न होता है।

रणनीति प्रत्येक उप-रणनीति के संकेतों की भारित गणना अनुकूलन योग्य भार प्रणाली के माध्यम से करती है, और केवल तभी ट्रेड ट्रिगर करती है जब भारित योग निर्धारित सीमा से अधिक हो। साथ ही, रणनीति में एक संभावित शीर्ष और तल पहचान तंत्र भी शामिल है, जो बाजार के संभावित उलटाव के समय स्थिति को समायोजित कर सकता है।

यह बहु-स्तरीय संकेत पुष्टि तंत्र प्रभावी रूप से गलत संकेतों को कम करता है और ट्रेडिंग सिस्टम की विश्वसनीयता बढ़ाता है, साथ ही लचीली पैरामीटर सेटिंग्स रणनीति को विभिन्न ट्रेडिंग इंस्ट्रूमेंट्स और समय सीमाओं के अनुकूल बनने में सक्षम बनाती हैं।

रणनीति के लाभ

-

संकेतों की बहु-पुष्टि: पांच स्वतंत्र तकनीकी संकेतकों द्वारा उत्पन्न संकेतों की भारित गणना एकल संकेतक के संभावित भ्रामक प्रभाव को कम करती है, जिससे ट्रेडिंग संकेतों की गुणवत्ता और विश्वसनीयता बढ़ती है।

-

अनुकूली भार प्रणाली: प्रत्येक उप-रणनीति को अलग-अलग भार दिए जा सकते हैं, जिससे व्यापारी अपने विभिन्न संकेतकों में विश्वास की डिग्री और ऐतिहासिक प्रदर्शन के आधार पर रणनीति के फोकस को समायोजित कर सकते हैं, जिससे लचीलापन बढ़ता है।

-

पूर्ण जोखिम प्रबंधन: रणनीति में बहु-स्तरीय जोखिम नियंत्रण तंत्र शामिल हैं, जिसमें स्टॉप-लॉस, बहु-स्तरीय लाभ-लक्ष्य और गतिशील स्टॉप-लॉस समायोजन शामिल है, जो बाजार के प्रतिकूल उतार-चढ़ाव की स्थिति में तुरंत जोखिम को नियंत्रित करने में सक्षम बनाता है।

-

स्वचालित संभावित शीर्ष और तल पहचान: RSI, ट्रेडिंग वॉल्यूम और मूल्य आंदोलनों के व्यापक विश्लेषण के माध्यम से, रणनीति संभावित बाजार शीर्ष और तल की पहचान कर सकती है और उपयुक्त अवसरों पर आंशिक रूप से स्थिति बंद करके लाभ को लॉक कर सकती है या नुकसान को कम कर सकती है।

-

उच्च अनुकूलन क्षमता: लगभग सभी पैरामीटर समायोजित किए जा सकते हैं, जिसमें प्रत्येक संकेतक की गणना अवधि, भार मान, लाभ-लक्ष्य और स्टॉप-लॉस प्रतिशत आदि शामिल हैं, जिससे व्यापारी अपनी व्यक्तिगत शैली और विभिन्न बाजार स्थितियों के अनुसार रणनीति को अनुकूलित कर सकते हैं।

-

अंतर्निहित विलंब तंत्र: समय से पहले ट्रेड में प्रवेश करने या शोर संकेतों पर ट्रेड करने से बचने के लिए, रणनीति एक विलंब पुष्टि तंत्र का उपयोग करती है, जो सुनिश्चित करती है कि केवल निरंतर संकेत ही ट्रेड को ट्रिगर करें, जिससे अल्पकालिक उतार-चढ़ाव का प्रभाव कम होता है।

-

समय फ़िल्टर फ़ंक्शन: रणनीति ट्रेडिंग शुरू और समाप्ति तिथियों को सेट करने की अनुमति देती है, जिससे व्यापारी विशिष्ट समय अवधि के लिए ऐतिहासिक डेटा पर बैकटेस्ट कर सकते हैं या ज्ञात असामान्य बाजार उतार-चढ़ाव की अवधि से बच सकते हैं।

रणनीति के जोखिम

-

पैरामीटर अतिअनुकूलन जोखिम: कई पैरामीटर होने के कारण, ऐतिहासिक डेटा के लिए अत्यधिक फिटिंग का जोखिम होता है, जिससे रणनीति वास्तविक ट्रेडिंग में खराब प्रदर्शन कर सकती है। समाधान कई समय सीमाओं और इंस्ट्रूमेंट्स पर बैकटेस्ट करना, अपेक्षाकृत मजबूत पैरामीटर सेटिंग्स का उपयोग करना और विशिष्ट ऐतिहासिक डेटा के लिए अत्यधिक अनुकूलन से बचना है।

-

बाजार की स्थितियों में बदलाव का जोखिम: रणनीति का प्रदर्शन ट्रेंडिंग बाजार और साइडवे बाजार में भिन्न हो सकता है, और बाजार की स्थिति में अचानक बदलाव से रणनीति की प्रभावशीलता कम हो सकती है। समाधान बाजार वातावरण पहचान तंत्र को शामिल करना, विभिन्न बाजार स्थितियों में पैरामीटर समायोजित करना या ट्रेडिंग को रोकना है।

-

संकेत विरोध जोखिम: एक साथ कई संकेतकों का उपयोग करने से परस्पर विरोधी संकेत उत्पन्न हो सकते हैं, जिससे निर्णय में भ्रम हो सकता है। समाधान प्रत्येक संकेतक के भार को उचित रूप से सेट करना, अधिक विश्वसनीय संकेतकों पर जोर देना और संकेत सीमाओं को तर्कसंगत रूप से सेट करके विरोध की संभावना को कम करना है।

-

अनुचित पूंजी प्रबंधन जोखिम: हालांकि रणनीति में स्टॉप-लॉस तंत्र शामिल है, फिर भी अनुचित पूंजी प्रबंधन तेजी से पूंजी को खत्म कर सकता है। समाधान प्रत्येक ट्रेड के लिए पूंजी के अनुपात को कड़ाई से नियंत्रित करना, यह सुनिश्चित करना है कि एकल ट्रेड का अधिकतम जोखिम सहनीय सीमा के भीतर हो।

-

तकनीकी विफलता जोखिम: स्वचालित ट्रेडिंग सिस्टम नेटवर्क डिस्कनेक्शन, डेटा विलंब आदि जैसी तकनीकी समस्याओं का सामना कर सकता है। समाधान मैन्युअल हस्तक्षेप तंत्र स्थापित करना, नियमित रूप से सिस्टम संचालन स्थिति की निगरानी करना और समय पर असामान्य स्थितियों को संभालना है।

रणनीति अनुकूलन दिशाएँ

-

बाजार वातावरण फ़िल्टर जोड़ना: एक संकेतक विकसित करना जो यह पहचान सके कि वर्तमान बाजार ट्रेंडिंग है या साइडवे, और बाजार की स्थिति के अनुसार प्रत्येक उप-रणनीति के भार को गतिशील रूप से समायोजित कर सके, ट्रेंडिंग बाजार में ट्रेंड-फॉलोइंग रणनीतियों को मजबूत कर सके और साइडवे बाजार में स्विंग रणनीतियों को मजबूत कर सके।

-

मशीन लर्निंग ऑप्टिमाइज़ेशन शामिल करना: मशीन लर्निंग तकनीकों का उपयोग करके प्रत्येक संकेतक के पैरामीटर और भार को स्वचालित रूप से समायोजित करना, ताकि रणनीति नवीनतम बाजार डेटा के अनुसार लगातार सीख और अनुकूलित हो सके, जिससे गतिशील अनुकूलन क्षमता बढ़े।

-

ट्रेडिंग वॉल्यूम विश्लेषण जोड़ना: ट्रेडिंग वॉल्यूम में बदलाव को एक अतिरिक्त पुष्टि संकेत के रूप में शामिल करना, केवल तभी ट्रेड निष्पादित करना जब अपेक्षित वॉल्यूम समर्थन हो, जिससे संकेतों की विश्वसनीयता बढ़े।

-

संभावित शीर्ष और तल पहचान एल्गोरिदम को अनुकूलित करना: मौजूदा शीर्ष और तल पहचान तर्क में सुधार करना, अतिरिक्त पुष्टि कारकों जैसे मूल्य पैटर्न, बहु-अवधि पुष्टि आदि को शामिल करना, ताकि पहचान सटीकता बढ़े।

-

भावना संकेतक शामिल करना: बाजार भावना संकेतकों जैसे VIX (फियर इंडेक्स), कॉल/पुट अनुपात आदि को एकीकृत करना, चरम बाजार भावना की स्थिति में ट्रेडिंग रणनीति को समायोजित करना या ट्रेडिंग को रोकना, उच्च अस्थिरता अवधि में अत्यधिक ट्रेडिंग से बचना।

-

गतिशील लाभ-लक्ष्य और स्टॉप-लॉस तंत्र विकसित करना: बाजार अस्थिरता के अनुसार स्वचालित रूप से लाभ-लक्ष्य और स्टॉप-लॉस स्तरों को समायोजित करना, उच्च अस्थिरता बाजार में स्टॉप-लॉस सीमा को चौड़ा करना और कम अस्थिरता बाजार में इसे संकीर्ण करना, ताकि जोखिम प्रबंधन अधिक लचीला और प्रभावी हो सके।

-

समय सीमा अनुकूलन: बहु-समय सीमा विश्लेषण फ़ंक्शन जोड़ना, उच्च और निम्न समय सीमाओं से एक साथ संकेत पुष्टि की आवश्यकता, गलत ब्रेकआउट और गलत संकेतों को कम करना।

सारांश

बहु-संकेतक भारित स्मार्ट ट्रेडिंग रणनीति कई तकनीकी विश्लेषण उपकरणों को एकीकृत करके और विभिन्न भार देकर एक व्यापक और लचीला ट्रेडिंग सिस्टम बनाती है। इस रणनीति में न केवल संकेतों की बहु-पुष्टि, अनुकूली भार प्रणाली और पूर्ण जोखिम प्रबंधन कार्य शामिल हैं, बल्कि एक स्वचालित संभावित शीर्ष और तल पहचान तंत्र भी है, जो इसे जटिल और परिवर्तनशील बाजार वातावरण में मजबूत अनुकूलन क्षमता प्रदर्शित करने में सक्षम बनाता है।

हालांकि पैरामीटर अतिअनुकूलन, बाजार की स्थितियों में बदलाव और संकेत विरोध जैसे संभावित जोखिम हैं, लेकिन उचित पैरामीटर सेटिंग्स, बाजार वातावरण पहचान और सख्त पूंजी प्रबंधन के माध्यम से इन जोखिमों को प्रभावी ढंग से नियंत्रित किया जा सकता है। भविष्य के अनुकूलन दिशाओं में बाजार वातावरण फ़िल्टर जोड़ना, मशीन लर्निंग तकनीकों को शामिल करना, ट्रेडिंग वॉल्यूम विश्लेषण बढ़ाना और संभावित शीर्ष और तल पहचान एल्गोरिदम को अनुकूलित करना शामिल है, ये सुधार रणनीति की स्थिरता और लाभप्रदता को और बढ़ाएंगे।

व्यवस्थित ट्रेडिंग विधियों की तलाश करने वाले निवेशकों के लिए, यह बहु-संकेतक भारित स्मार्ट ट्रेडिंग रणनीति एक विचारणीय ढांचा प्रदान करती है, जो न केवल ट्रेडिंग निर्णयों पर भावनात्मक कारकों के प्रभाव को कम कर सकती है, बल्कि डेटा-संचालित तरीके से ट्रेडिंग प्रदर्शन को लगातार अनुकूलित भी कर सकती है। इस रणनीति को लागू करते समय, रूढ़िवादी पैरामीटर सेटिंग्स से शुरू करने, धीरे-धीरे समायोजित करने और रणनीति के प्रदर्शन की बारीकी से निगरानी करने की सलाह दी जाती है, ताकि व्यक्तिगत जोखिम सहनशीलता और बाजार की स्थितियों के लिए सबसे उपयुक्त कॉन्फ़िगरेशन पाया जा सके।

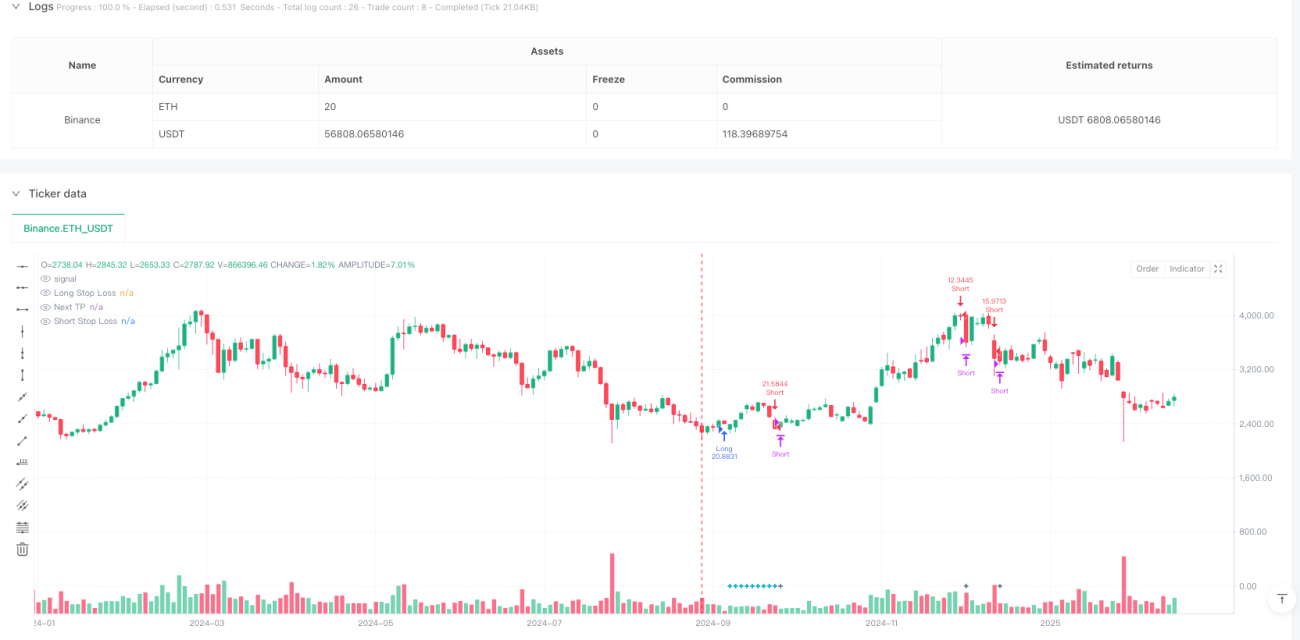

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1