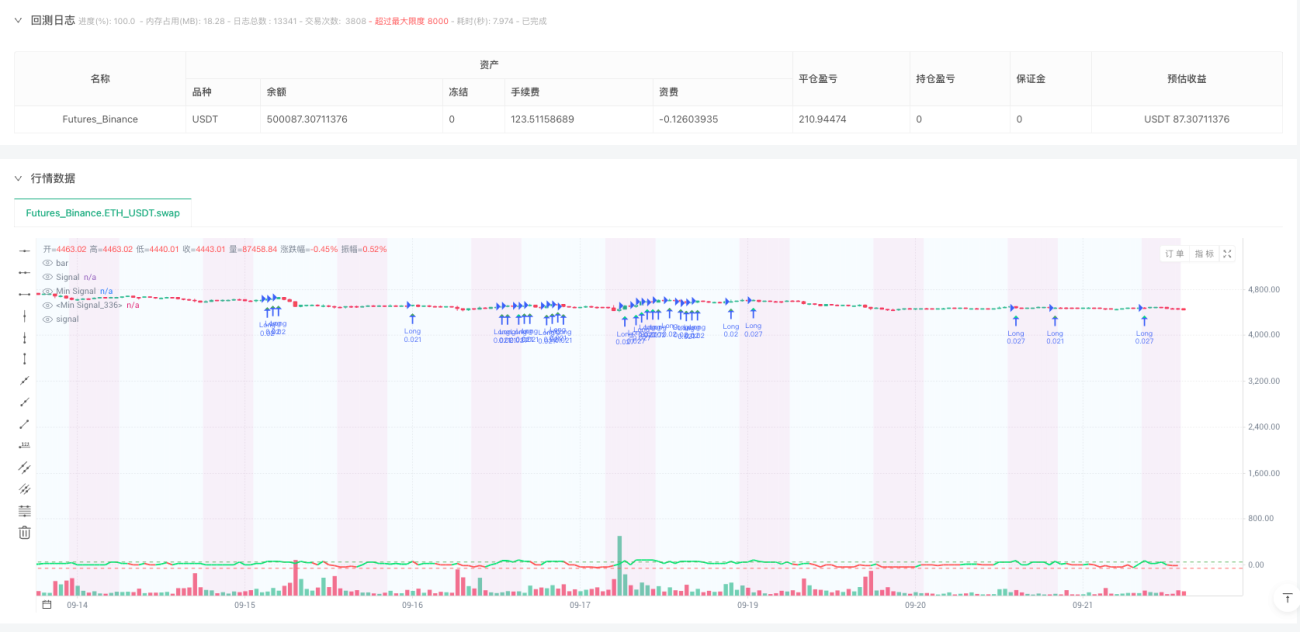

🎯 रणनीति का मूल: सप्ताहांत बाजार पर विशेषज्ञ स्मार्ट मनी

क्या आप जानते हैं? जब वॉल स्ट्रीट के बड़े खिलाड़ी सप्ताहांत में छुट्टी पर होते हैं, तो क्रिप्टो बाजार में गुप्त मौके छिपे होते हैं! यह रणनीति एक रात की पाली के चौकीदार की तरह काम करती है, जो संस्थागत निवेशकों के "ऑफिस छोड़ने" पर मौके ढूंढती है।

मुख्य बात! यह रणनीति केवल शनिवार और रविवार को कारोबार करती है, विशेषकर रविवार 0-8 UTC समयावधि में। क्यों? क्योंकि इस समय तरलता अपेक्षाकृत कम होती है, जबकि तकनीकी विश्लेषण की प्रभावशीलता अधिक होती है, ठीक वैसे ही जैसे किसी शांत पुस्तकालय में बारीक आवाज़ को सुनना आसान होता है।

📊 एकाधिक संकेतकों का संयोजन: अकेले नहीं, टीम के साथ

यह रणनीति एक एवेंजर्स टीम की तरह है:

- RSI (8 कालावधि) : ओवरबॉट/ओवरसोल्ड संकेतों को तेजी से पकड़ता है

- MACD (8,17,9) : प्रवृत्ति गति की पुष्टि करता है

- बोलिंगर बैंड (20,2.5) : मूल्य चरम क्षेत्रों की पहचान करता है

- CVD डाइवर्जेंस : स्मार्ट मनी के वास्तविक इरादे का पता लगाता है

खतरे से बचने की गाइड : एकल संकेतक अकेले फिल्म देखने जैसा है, कहानी से गुमराह होने की संभावना अधिक है। कई संकेतकों से पुष्टि लेना दोस्तों के साथ देखने जैसा है, जहाँ अलग-अलग दृष्टिकोण सुनने को मिलते हैं!

💰 स्मार्ट मनी प्रबंधन: 500 डॉलर से भी खेल सकते हैं

सबसे दिलचस्प भाग! यह प्रणाली छोटी पूंजी के लिए डिज़ाइन की गई है:

- न्यूनतम 120 डॉलर प्रति ऑर्डर : आपको एक बार में सब कुछ दांव पर नहीं लगाना पड़ता

- अधिकतम 4 समवर्ती पोजीशन : जोखिम का फैलाव, एक टोकरी में सभी अंडे नहीं

- 5-20 गुना गतिशील लीवरेज : बाजार की अस्थिरता के अनुसार स्वचालित रूप से समायोजित

जैसे गाड़ी चलाना - हाईवे पर तेज चल सकते हैं, लेकिन गलियों में धीरे चलना पड़ता है। सिस्टम विभिन्न क्रिप्टो के जोखिम प्रोफाइल के अनुसार पोजीशन आकार को समायोजित करता है।

🛡️ जोखिम नियंत्रण: आपकी माँ से भी ज्यादा परवाह

त्रिगुण सुरक्षा तंत्र :

- दैनिक हानि सीमा 5% : आज बहुत नुकसान हुआ? कल फिर आना

- सप्ताहांत हानि सीमा 15% : सप्ताहांत में मौज-मस्ती की भी सीमा होती है

- लगातार 4 बार हानि पर रुकें : भावनात्मक व्यापार को रोकें

आपातकालीन ब्रेक सिस्टम : यदि खाते की हानि 30% से अधिक हो जाए, तो तुरंत सभी ट्रेड बंद कर दें। यह कार के ABS सिस्टम की तरह है, जो महत्वपूर्ण क्षण में जान बचा सकता है!

- 1