पैरामीटर गुणक रणनीति: बहु-संकेतक संलयन का बाजार मेट्रोनोम

🎯 यह कैसा जादुई स्ट्रेटजी है?

क्या आप जानते हैं? यह स्ट्रेटजी बाजार पर एक "सुपर रडार" लगाने जैसा है! यह सिर्फ एक-दो इंडिकेटर्स नहीं देखता, बल्कि 9 अलग-अलग तकनीकी इंडिकेटर्स को एक बैंड की तरह जोड़ता है, हर इंडिकेटर एक "संगीत वाद्य" है, और जब ये सब मिलकर सामंजस्यपूर्ण "स्वर" बजाते हैं, तभी स्ट्रेटजी ट्रेडिंग सिग्नल देती है। कल्पना कीजिए, यह ऐसा है जैसे 9 विशेषज्ञ एक साथ आपके कान में सलाह दे रहे हों, और जब उनमें से ज़्यादातर सहमत हों, तभी आप कार्रवाई करें!

📊 मुख्य सिद्धांत का राज खुलासा

ध्यान दें! इस स्ट्रेटजी की जान है "पैरामीटर मल्टीप्लायर" की अवधारणा। यह RSI, ADX, मोमेंटम, चेंज रेट, ATR, वॉल्यूम, एक्सेलेरेशन और स्लोप जैसे इंडिकेटर्स को पहले एक समान पैमाने पर मानकीकृत करता है, फिर उन्हें गुणा करके एक "संयुक्त शक्ति मान" प्राप्त करता है। जैसे खाना पकाने में हर मसाले का एक आदर्श अनुपात होता है, वैसे ही यह स्ट्रेटजी बाजार के विभिन्न "मसालों" का सही मिश्रण ढूंढने में आपकी मदद करता है! जब संयुक्त शक्ति मान अपनी मूविंग एवरेज को पार करता है, तो यह एंट्री का सबसे अच्छा समय होता है।

🔧 अनुकूलन योग्य ट्रेडिंग टूल

इस स्ट्रेटजी की सबसे अच्छी बात क्या है? आप इसे ब्लॉक्स जोड़ने की तरह स्वतंत्र रूप से कॉम्बिनेशन कर सकते हैं! कोई इंडिकेटर इस्तेमाल नहीं करना चाहते? बस उसे बंद कर दें। पीरियड पैरामीटर बदलना चाहते हैं? आपकी मर्जी। इसमें SMA ट्रेंड फिल्टर भी है, जो आपको ट्रेंड के विपरीत ट्रेडिंग के बड़े नुकसान से बचाता है। यह एक "ट्रेडिंग स्ट्रेटजी DIY टूलकिट" जैसा है, जो आपको विभिन्न बाजार स्थितियों के अनुसार कॉन्फ़िगरेशन बदलने की सुविधा देता है।

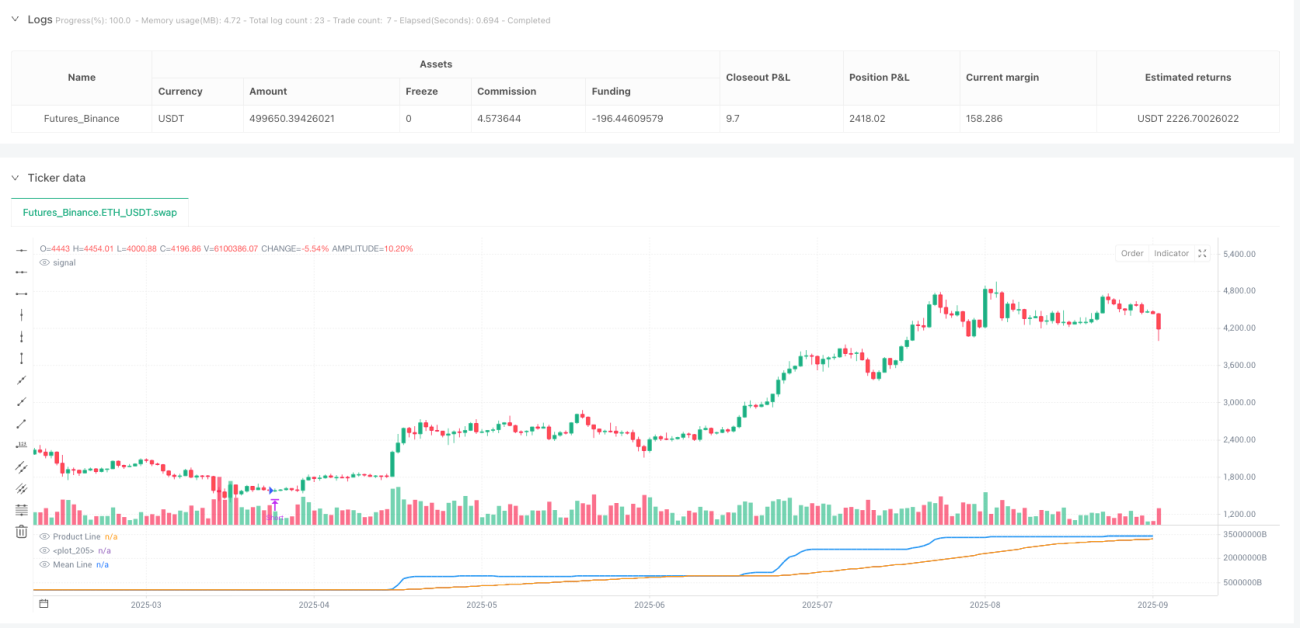

⚡ प्रैक्टिकल एप्लिकेशन गाइड

अब आता है नुकसान से बचने का गाइड! यह स्ट्रेटजी खास तौर पर रेंज और ट्रेंड मिश्रित बाजार स्थितियों के लिए उपयुक्त है। जब नीली प्रोडक्ट लाइन ऊपर की ओर नारंगी मूविंग एवरेज को पार करती है, तो लॉन्ग (खरीदारी) करें, और जब नीचे की ओर पार करती है, तो शॉर्ट (बिक्री) करें। स्ट्रेटजी में एक ऑटोमैटिक पोजीशन क्लोजिंग मैकेनिज्म भी है, जो आपको रिवर्स सिग्नल आने पर बेवजह पोजीशन होल्ड करने से बचाता है। याद रखें, ट्रेंड फिल्टर चालू करने से आप बड़े ट्रेंड में आसानी से चल सकते हैं, और इसे बंद करने से आप ज़्यादा शॉर्ट-टर्म अवसरों को पकड़ सकते हैं!

//@version=5

strategy("Parametric Multiplier Backtester", shorttitle="PMB", overlay=false)

// Author: Script_Algo

// License: MIT

// Permission is hereby granted, free of charge, to any person obtaining a copy

// of this software and associated documentation files (the "Software"), to deal

// in the Software without restriction, including without limitation the rights

// to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

// copies of the Software, subject to the following conditions:

// The above copyright notice and this permission notice shall be included in

// all copies or substantial portions of the Software.- 1