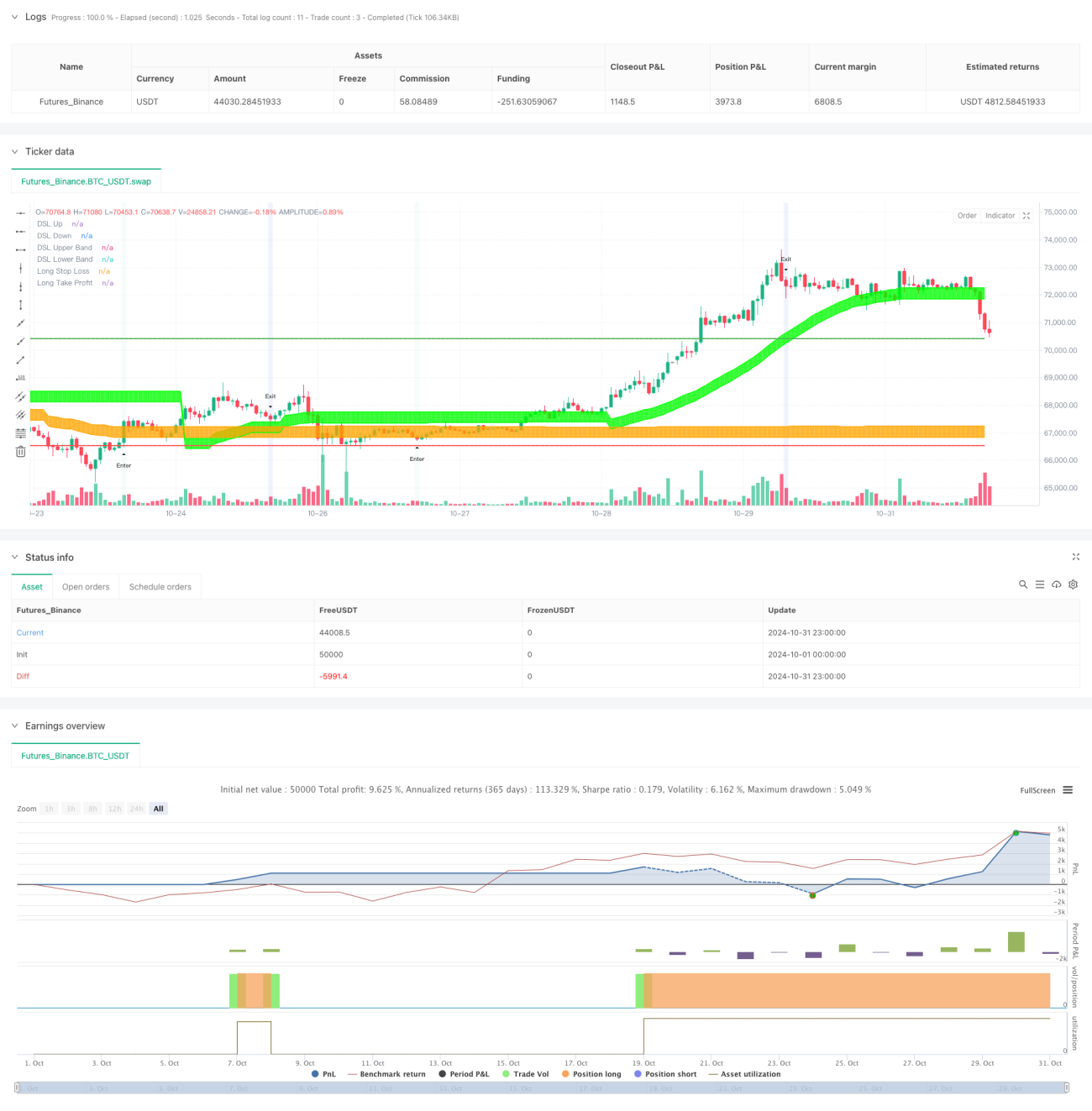

Ikhtisar

Strategi ini adalah sistem perdagangan komprehensif yang menggabungkan Dynamic Signal Line (DSL), volatilitas, dan indikator momentum. Dengan menggunakan ambang batas dinamis dan pita volatilitas adaptif, strategi ini secara efektif mengidentifikasi tren pasar dan memanfaatkan indikator momentum untuk menyaring sinyal, memungkinkan penentuan waktu perdagangan yang presisi. Sistem ini dilengkapi dengan mekanisme manajemen risiko yang lengkap, termasuk stop loss dinamis dan penetapan target profit berdasarkan rasio risiko-imbal hasil.

Prinsip Strategi

Logika inti strategi didasarkan pada tiga komponen utama:

Pertama adalah sistem Dynamic Signal Line, yang menghitung pita atas dan bawah dinamis berdasarkan moving average. Pita-pita ini secara otomatis menyesuaikan posisinya sesuai dengan titik tertinggi dan terendah pasar terbaru, memungkinkan pelacakan tren yang adaptif. Sistem ini juga menggabungkan indikator ATR untuk membangun pita volatilitas dinamis guna mengonfirmasi kekuatan tren dan menetapkan posisi stop loss.

Kedua adalah sistem analisis momentum, yang menggunakan indikator RSI yang dioptimalkan dengan Zero-Lag Exponential Moving Average (ZLEMA). Dengan menerapkan konsep Dynamic Signal Line pada RSI, sistem dapat mengidentifikasi area overbought dan oversold dengan lebih akurat, serta menghasilkan sinyal breakout momentum.

Ketiga adalah mekanisme integrasi sinyal. Sinyal perdagangan hanya akan dipicu jika kondisi konfirmasi tren dan breakout momentum terpenuhi secara bersamaan. Untuk posisi long, harga harus menembus pita atas dan bertahan di atasnya, sementara RSI menembus Dynamic Signal Line bawah. Untuk sinyal short, kondisi sebaliknya harus terpenuhi.

Keunggulan Strategi

- Adaptif Tinggi: Dynamic Signal Line dan pita volatilitas menyesuaikan secara otomatis dengan kondisi pasar, memungkinkan strategi beradaptasi dengan berbagai lingkungan pasar.

- Penyaringan Sinyal Palsu: Dengan memerlukan konfirmasi ganda dari tren dan momentum, probabilitas sinyal palsu berkurang secara signifikan.

- Manajemen Risiko Lengkap: Terintegrasi dengan stop loss dinamis berdasarkan ATR dan penetapan target profit berdasarkan rasio risiko-imbal hasil, memungkinkan pengendalian risiko yang sistematis.

- Fleksibel dan Dapat Disesuaikan: Parameter strategi dapat dioptimalkan dan disesuaikan sesuai dengan pasar dan kerangka waktu yang berbeda.

Risiko Strategi

- Risiko Pembalikan Tren: Dalam pembalikan pasar yang tajam, penyesuaian Dynamic Signal Line mungkin tidak cukup cepat, menyebabkan drawdown yang besar.

- Risiko Pasar Sideways: Dalam pasar yang bergerak di kisaran (sideways), breakout yang sering dapat menyebabkan beberapa kali stop loss.

- Sensitivitas Parameter: Kinerja strategi cukup sensitif terhadap pengaturan parameter; parameter yang tidak tepat dapat memengaruhi efektivitas strategi.

Arah Optimasi Strategi

- Identifikasi Lingkungan Pasar: Dapat menambahkan mekanisme klasifikasi lingkungan pasar, menggunakan pengaturan parameter yang berbeda dalam kondisi pasar yang berbeda.

- Optimasi Parameter Dinamis: Memperkenalkan mekanisme penyesuaian parameter adaptif yang secara otomatis mengoptimalkan parameter Dynamic Signal Line dan pita volatilitas berdasarkan volatilitas pasar.

- Analisis Multi-Timeframe: Mengintegrasikan sinyal dari beberapa kerangka waktu untuk meningkatkan keandalan keputusan perdagangan.

- Adaptasi Volatilitas: Menyesuaikan lebar stop loss dan rasio risiko-imbal hasil selama periode volatilitas tinggi untuk meningkatkan imbal hasil yang disesuaikan dengan risiko.

Kesimpulan

Strategi ini mencapai penangkapan tren pasar yang efektif melalui kombinasi inovatif Dynamic Signal Line dan indikator momentum. Mekanisme manajemen risiko yang lengkap dan sistem penyaringan sinyal memberikan nilai aplikasi praktis yang kuat. Dengan optimasi berkelanjutan dan penyesuaian parameter, strategi ini diharapkan dapat mempertahankan kinerja yang stabil di berbagai lingkungan pasar. Meskipun terdapat beberapa titik risiko, risiko ini dapat dikelola dengan pengaturan parameter yang tepat dan langkah-langkah pengendalian risiko.

- 1