Ikhtisar

Strategi ini adalah sistem trading komposit berdasarkan Keltner Channel dan level support dan resistance dinamis. Dengan menganalisis beberapa kerangka waktu, menggabungkan rata-rata bergerak dan indikator volatilitas, strategi ini membentuk kerangka kerja pengambilan keputusan yang lengkap. Inti dari strategi adalah mengidentifikasi momen ketika harga menembus level teknis kunci, sambil mempertimbangkan tren pasar dan volatilitas, sehingga menangkap peluang trading dengan probabilitas tinggi.

Prinsip Strategi

Strategi menggunakan sistem indikator teknis multi-lapis untuk analisis:

- Menggunakan Keltner Channel periode 21 sebagai alat penentu tren utama, lebar channel ditentukan oleh nilai ATR.

- Menghitung level support dan resistance kunci berdasarkan 21 candle di kiri dan 8 candle di kanan.

- Memasukkan rata-rata bergerak dari kerangka waktu yang lebih tinggi sebagai filter tren.

- Menggabungkan rata-rata bergerak jangka pendek (5 periode) dan jangka panjang (30 periode) untuk menentukan waktu entry.

- Menggunakan ATR untuk menyesuaikan posisi stop loss secara dinamis.

Keunggulan Strategi

- Indikator teknis multi-dimensi saling memvalidasi, secara efektif mengurangi sinyal palsu.

- Level support dan resistance dinamis diperbarui secara real-time, beradaptasi dengan perubahan pasar.

- Melalui analisis kerangka waktu yang lebih tinggi, menyaring pergerakan sekunder.

- Menyesuaikan parameter stop loss secara fleksibel sesuai dengan kerangka waktu yang berbeda.

- Menggunakan manajemen posisi berbasis persentase, mengontrol risiko secara efektif.

Risiko Strategi

- Dapat menghasilkan sinyal trading yang sering dalam pasar sideways (konsolidasi).

- Validasi multi-indikator dapat menyebabkan terlewatnya beberapa peluang trading.

- Optimasi parameter memiliki risiko overfitting.

- Dalam lingkungan volatilitas tinggi, posisi stop loss mungkin terlalu lebar.

- Level support dan resistance dapat gagal saat pasar berubah secara drastis.

Arah Optimasi Strategi

- Memasukkan indikator volume sebagai alat bantu untuk menilai validitas breakout.

- Menambahkan modul analisis volatilitas pasar untuk menyesuaikan parameter secara dinamis.

- Mengoptimalkan metode perhitungan level support dan resistance untuk meningkatkan akurasi.

- Menambahkan penilaian kekuatan tren untuk memperhalus kondisi entry.

- Menyempurnakan sistem manajemen posisi untuk mencapai kontrol risiko yang lebih presisi.

Kesimpulan

Ini adalah strategi trading kuantitatif yang terstruktur dan logis. Melalui penggunaan indikator teknis multi-lapis, strategi ini memastikan keandalan sinyal trading sekaligus mencapai kontrol risiko yang efektif. Strategi ini memiliki skalabilitas yang kuat, dan melalui optimasi serta perbaikan berkelanjutan, diharapkan dapat mempertahankan kinerja yang stabil di berbagai kondisi pasar.

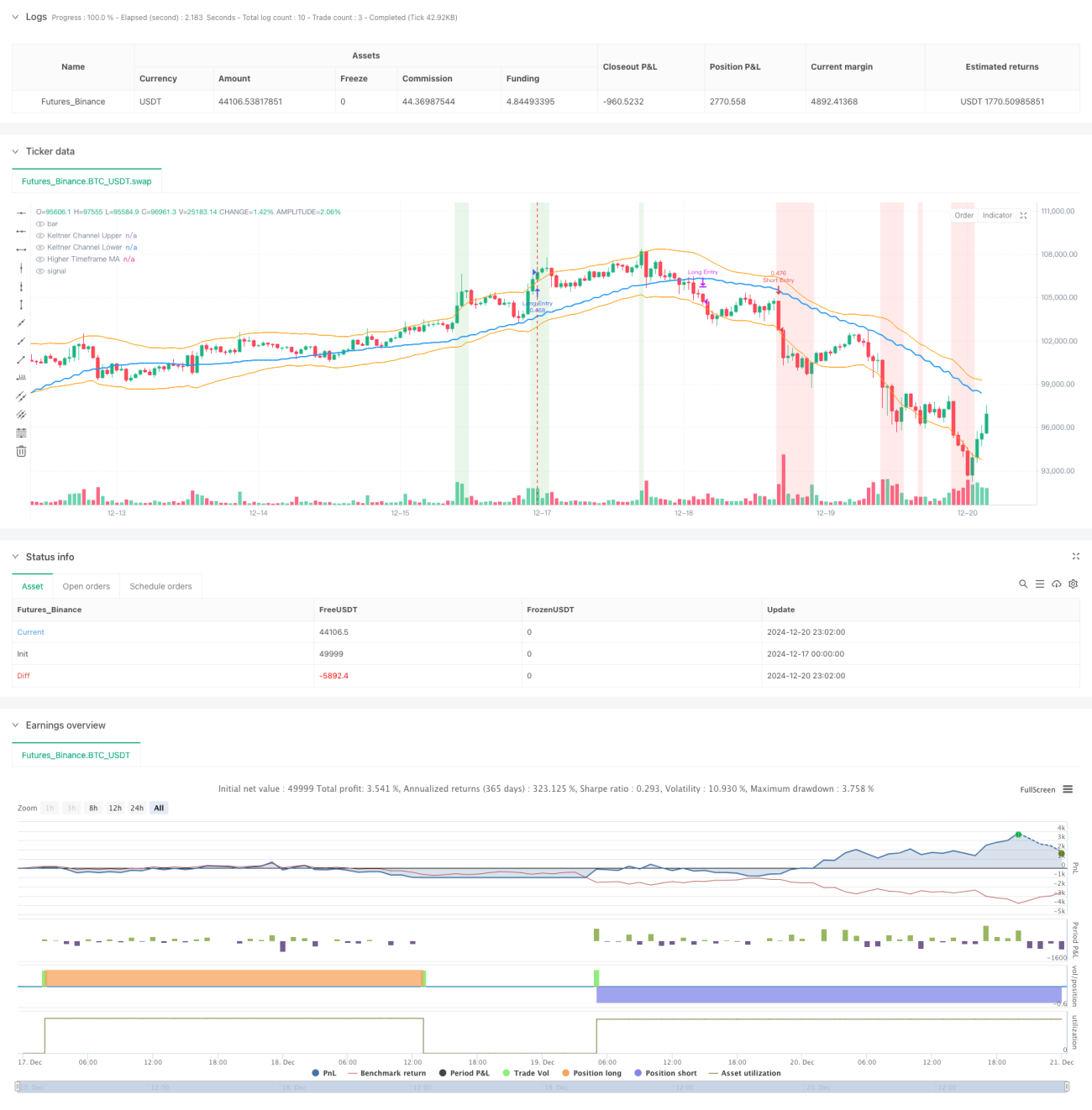

/*backtest

start: 2024-12-17 00:00:00

end: 2024-12-21 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © sathcm

//@version=5

strategy("KMS", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.05, slippage=3)- 1