動的二重スーパートレンド出来高価格戦略

1

Follow

1802

Followers

概要

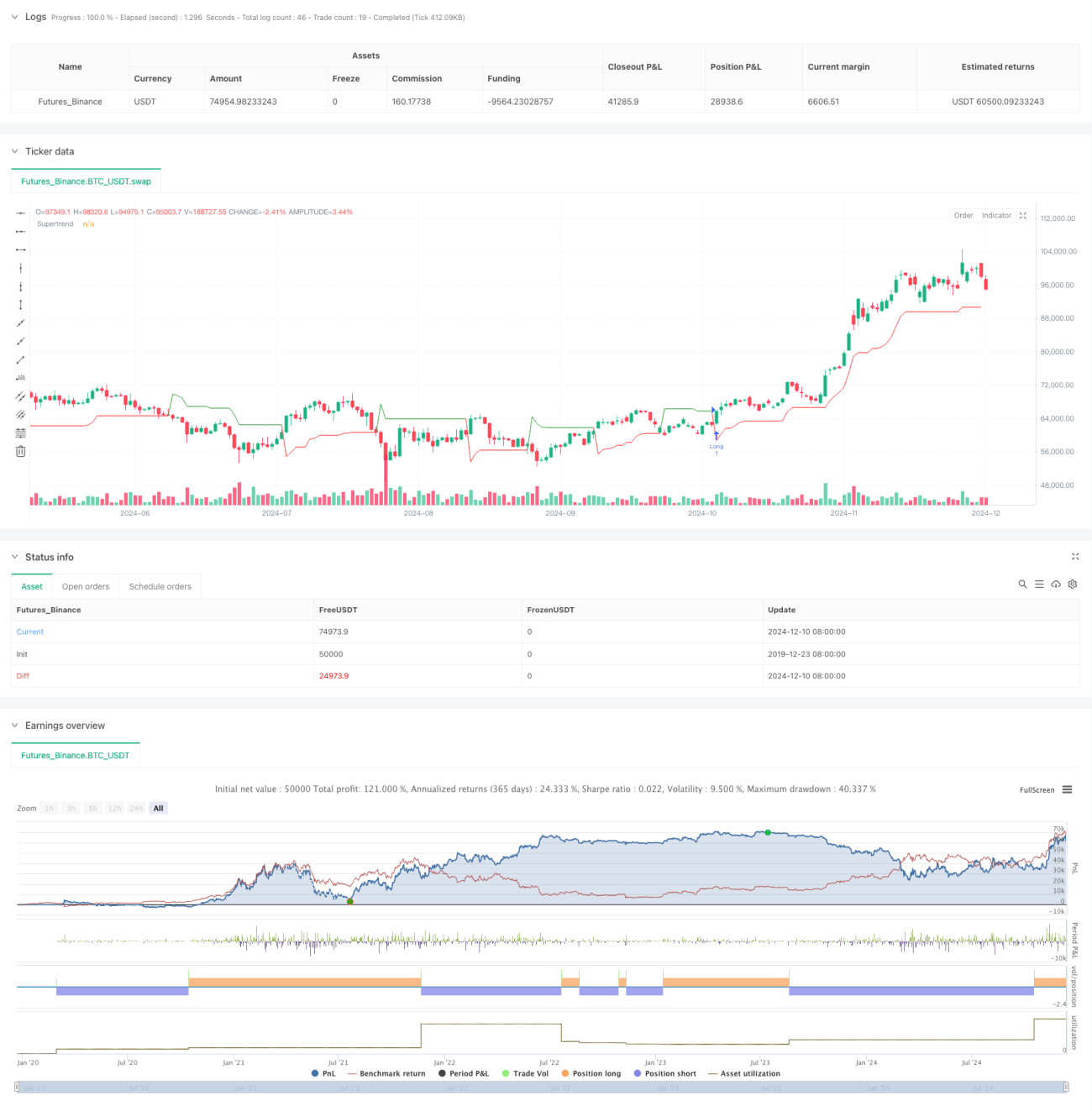

これは、スーパートレンド指標と出来高分析を組み合わせた高度な定量取引戦略です。この戦略は、価格とスーパートレンドラインのクロス、および出来高の異常な動きを動的に監視することで、潜在的なトレンド転換点を特定します。戦略では、真のレンジ(ATR)に基づく動的なストップロスと利益確定設定を採用し、取引の柔軟性を確保しつつ、リスク管理の信頼性を提供します。

戦略の原理

戦略の中核ロジックは、以下の主要な要素に基づいています。

- スーパートレンド指標を主なトレンド判断ツールとして使用。この指標はATRに基づいて計算され、市場のボラティリティに動的に適応します。

- 20期間の移動平均出来高を基準とし、1.5倍の閾値を設定して出来高の異常を判断します。

- 価格がスーパートレンドラインを突破し、かつ出来高が異常条件を満たした場合に取引シグナルを発生させます。

- ATRに基づく動的なストップロス(1.5倍ATR)と利益確定(3倍ATR)設定を採用し、リスクリターン比を最適化します。

戦略の利点

- シグナルの信頼性が高い:トレンドと出来高の2つの次元で確認を行うため、誤ったシグナルの確率が大幅に低下します。

- リスク管理が充実:動的なストップロスと利益確定設定により、市場のボラティリティに応じてリスクパラメータを自動調整できます。

- 適応性が高い:戦略パラメータは、異なる市場環境や取引商品に応じて柔軟に調整可能です。

- 実行が明確:取引ルールが明確であり、主観的判断要素がなく、自動取引に適しています。

戦略のリスク

- レンジ相場のリスク:横ばいのレンジ相場では、頻繁な誤ったシグナルが発生する可能性があります。

- スリッページリスク:出来高が異常な時期には、大きなスリッページ損失が発生する可能性があります。

- パラメータ感応度:戦略効果はパラメータ設定に敏感であり、継続的な最適化が必要です。

- システミックリスク:市場が急激に変動する時期には、ストップロス設定が機能しない可能性があります。

戦略の最適化方向

- トレンド強度フィルターの導入:ADX指標を追加してトレンドの強さを判断し、強いトレンド時のみポジションを保有する。

- 出来高指標の最適化:単純な倍数判断ではなく、相対的出来高変化率(ROC)を検討する。

- ストップロスメカニズムの改善:トレーリングストップロス機能を導入し、利益をより確実に確保する。

- 時間フィルターの追加:取引時間帯の設定を追加し、高ボラティリティ時間帯を避ける。

まとめ

本戦略は、スーパートレンド指標と出来高分析を組み合わせることで、信頼性と適応性を兼ね備えた取引システムを構築しています。戦略の利点は、シグナル確認の多次元性とリスク管理の動的な性質にありますが、市場環境が戦略パフォーマンスに与える影響に留意する必要があります。継続的な最適化と改善により、本戦略は様々な市場環境で安定したパフォーマンスを維持することが期待されます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1