トリプルEMA平滑モメンタムと資金フロー総合取引戦略

2

Follow

502

Followers

概要

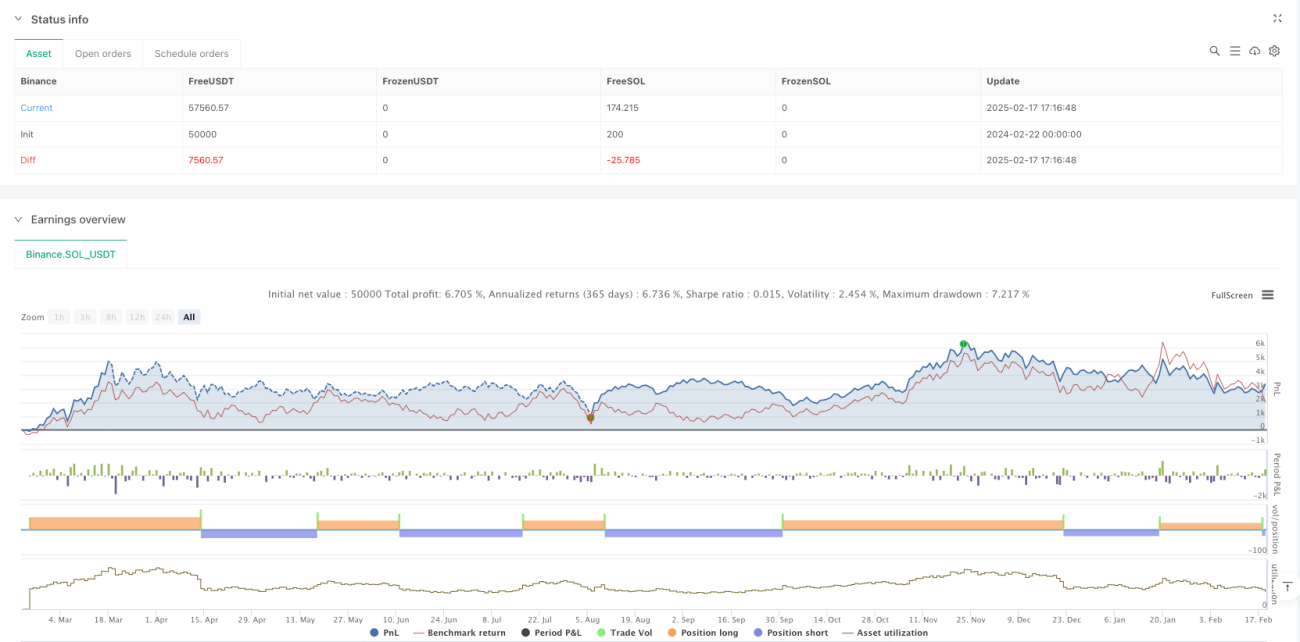

本戦略は、モメンタム指標と資金流量指標を組み合わせた総合取引システムです。三重指数移動平均(EMA)によりモメンタム指標を平滑化し、市場ノイズを効果的に低減します。戦略では変化率(ROC)を用いて元のモメンタムを計算し、マネーフローインデックス(MFI)と組み合わせて取引シグナルを確認することで、様々な時間足の取引に適用できます。

戦略の原理

戦略の核心的な原理は、モメンタム指標とマネーフローインデックス(MFI)の2つの主要なテクニカル指標に基づいています。まずROCで元のモメンタムを計算し、次に三重EMAで平滑化することで、より安定したモメンタムシグナルラインを取得します。取引シグナルの発生には、モメンタムとMFIの両方の条件を同時に満たす必要があります。平滑化されたモメンタムがプラスでMFIが中央値より高い場合に買いシグナル、平滑化されたモメンタムがマイナスでMFIが中央値より低い場合に売りシグナルが生成されます。また、モメンタムとMFIの転換点に基づいたエグジットメカニズムも設計されており、早期の損切りと利益確定に役立ちます。

戦略の優位性

- シグナルの平滑性が高い:三重EMA処理により、偽シグナルが大幅に減少し、取引の信頼性が向上します。

- 二重確認メカニズム:モメンタムと資金流量の2つの次元を組み合わせることで、単一指標の限界を低減します。

- 適応性が広い:様々な時間足に適用可能で、汎用性が高いです。

- リスク管理が充実:明確なエントリーとエグジット条件を備え、ストップロスメカニズムを含みます。

- パラメータ調整の柔軟性が高い:複数の調整可能なパラメータを提供し、市場状況に応じた最適化が可能です。

戦略のリスク

- トレンド転換のリスク:激しい変動市場では、シグナルに遅延が生じる可能性があります。

- パラメータ感度:パラメータ設定の違いにより、戦略のパフォーマンスが大きく異なる可能性があります。

- 市場環境への依存:レンジ相場では、頻繁に偽シグナルが発生する可能性があります。

- 資金管理のリスク:リスクをコントロールするには、適切なポジションサイズ設定が必要です。

- テクニカル指標の限界:テクニカル指標に基づく戦略は、ファンダメンタルズの変化時に無効になる可能性があります。

戦略の最適化方向

- ボラティリティフィルターの導入:ATR指標を追加し、低ボラティリティ期間のシグナルをフィルタリングします。

- エグジットメカニズムの最適化:トレーリングストップと利益目標を追加します。

- 時間フィルターの追加:重要な経済指標発表の時間帯を避けます。

- 出来高確認の追加:出来高分析を組み合わせ、シグナルの信頼性を高めます。

- 適応型パラメータの開発:市場の状態に応じてパラメータを動的に調整します。

まとめ

本戦略は、設計が合理的でロジックが明確な総合取引戦略です。モメンタムと資金流量指標の組み合わせ、および三重EMA平滑化処理により、シグナルの即時性と信頼性を効果的にバランスしています。実用性と拡張性に優れ、さらなる最適化と実取引への応用に適しています。実際の取引では、リスク管理に注意し、適切なパラメータ設定を行い、具体的な市場状況に応じて最適化・調整することを推奨します。

Source

Pine

/*backtest

start: 2024-02-22 00:00:00

end: 2025-02-19 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Momentum & Money Flow Strategy with Triple EMA Smoothing", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input parametersStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1