マルチタイムフレーム平均回帰トレンドブレイク取引システム

戦略概要

マルチサイクル平均回帰トレンドブレイクアウトシステムは、総合的な定量取引戦略であり、ウィコフ市場サイクル理論、プライスプロファイル分析、平均回帰、トレンドフォローという4つの強力な取引手法を巧みに融合させている。本戦略は中長期のスイングトレーダー向けに設計されており、リスク選好や市場状況に応じて柔軟に調整できる広範なカスタマイズオプションを提供する。

戦略の中核コンポーネントは、市場サイクルフェーズを識別するウィコフ分析、主要支持・抵抗レベルの特定を行うプライスプロファイル分析、買われすぎ・売られすぎ状況を捉える平均回帰コンポーネント、そして中長期的な価格変動を捕捉するトレンドフォローシステムから構成される。これらのコンポーネントが連携し、高い確率の取引シグナルを提供する包括的な取引システムを形成する。

戦略の原理

本戦略の中心的原理は、4つの主要な取引手法の相乗効果に基づく。

-

ウィコフ分析: リチャード・D・ウィコフの市場サイクル理論に基づき、蓄積段階、上昇段階、分配段階、下降段階の4つの主要フェーズを識別する。また、「スプリング」(偽ブレイク後の急反転)や「アップスラスト」(偽ブレイク)といった特殊パターンも検出する。これらのフェーズは価格と出来高の関係によって定義され、機関投資家の資金フローを追跡するのに役立つ。

-

プライスプロファイル分析: 市場プロファイル/ボリュームプロファイルの簡略版を実装し、コントロールポイント、高バリューエリア、低バリューエリアを計算し、主要な価格活動が発生するレンジを確立する。これらのキーレベルの可視化は、潜在的な支持・抵抗ゾーンの特定に寄与する。

-

平均回帰: 価格が極端な領域に達した際に、潜在的な反転ポイントを識別する。ボリンジャーバンドを用いて買われすぎ・売られすぎの価格領域を定義し、RSIダイバージェンスを組み合わせて反転を確認する。強いトレンドでの偽シグナルを避けるため、複数の確認シグナルを要求する。

-

トレンドフォロー: 中長期的な方向性のある価格変動を捕捉し、複数の移動平均線(9、21、50、200EMA)でトレンド方向と強度を確認、MACD分析でモメンタム確認とトレンド強度を評価、そして直近の価格構造分析による高時間枠でのトレンド一貫性を実現する。

これら4つのコンポーネントは相互に補完し合い、取引シグナルの生成に共同で作用する。システムは複雑なシグナル合成手法を採用し、複数のシステムの確認を経て初めて最終的な取引シグナルを生成することで、偽シグナルの可能性を効果的に低減する。

戦略のメリット

マルチサイクル平均回帰トレンドブレイクアウトシステムには、以下の顕著な利点がある。

-

総合的な分析フレームワーク: 4つの異なるが相補的な取引手法を統合することで、市場を多角的に分析でき、取引シグナルの質と信頼性が向上する。この多次元分析により、単一指標に起因するバイアスや誤シグナルが減少する。

-

異なる市場環境への適応性: 戦略の柔軟性により、さまざまな市場環境で良好に機能する。トレンド相場ではトレンドフォローコンポーネントが優勢となり、レンジ相場では平均回帰とプライスプロファイル分析がより有効に働く。

-

機関投資家の資金フローとの整合: ウィコフ分析を通じて、戦略は機関投資家の資金フローと一致するように設計されており、長期にわたる取引成功に不可欠である。このコンポーネントは、大口資金の蓄積段階と分配段階を識別し、取引成功率を高める。

-

強力なリスク管理: 戦略には、ATRベースの自動損切り・利確、トレーリングストップ、ポジション保有時間に基づくエグジット戦略、そしてエクイティ比率に基づくポジションサイジングなど、複数のリスク管理機能が組み込まれている。これらの機能により、堅牢な資金管理が確保される。

-

高度なカスタマイズ性: 取引スタイル、市場選好、リスク許容度に応じて調整できる広範なパラメータ設定が提供される。主要コンポーネントは個別に有効化・無効化でき、様々な取引手法に対応可能である。

戦略のリスク

本戦略には多くの利点がある一方で、以下の潜在的なリスクと課題も存在する。

-

パラメータ過剰最適化リスク: 調整可能なパラメータが多数含まれており、過去データへの過剰適合リスクが生じる。過剰最適化を避け、実際の取引前に堅牢なフォワードテストを実施することが推奨される。

-

複雑性の管理: 戦略の総合性は同時に複雑性をもたらす。特に初心者トレーダーにとって、すべてのコンポーネントの相互作用を理解・管理することは困難な場合がある。まず各コンポーネントを個別に理解し、その後段階的に統合して使用することが推奨される。

-

市場環境の変化: 特定の市場環境では、一部のコンポーネントのパフォーマンスが低下する可能性がある。例えば、急激なトレンド転換期には平均回帰シグナルが損失を生むことがある。トレーダーは市場環境を監視し、それに応じて戦略コンポーネントのウェイトを調整する必要がある。

-

執行遅延の影響: 複数の確認を要求する本戦略は、特に急変動する市場においてエントリーポイントの遅延を招く可能性がある。これにより、トレンドの一部を逃したり、最適でない価格でエントリーするリスクが生じる。

-

テクニカル指標への依存: 戦略は移動平均線、RSI、MACDなどのテクニカル指標に大きく依存している。特定の市場条件下では、これらの指標が機能しなくなったり、誤ったシグナルを発する可能性がある。ファンダメンタル分析やその他の非テクニカル要因を補完として組み合わせることが推奨される。

これらのリスクを軽減する方法としては、小ポジションから始める段階的導入、定期的なバックテストと最適化、サンプル外テストによる戦略有効性の検証、そして1取引あたりの最大損失や日次最大損失制限などの厳格なリスク管理ルールの設定が挙げられる。

戦略の最適化方向性

コードの詳細分析に基づき、本戦略は以下の方向で最適化が可能である。

-

適応的パラメータ設定: 現在の戦略ではRSI期間やボリンジャーバンドの標準偏差など固定パラメータを使用している。ボラティリティや市場状態に基づく適応的パラメータを導入することで、異なる市場環境でのパフォーマンスを向上できる。例えば、高ボラティリティ時には広いボリンジャーバンド、低ボラティリティ時には狭いバンドを使用する。

-

機械学習の統合: 機械学習アルゴリズムを導入してシグナル生成とフィルタリングプロセスを最適化する。例えば、分類アルゴリズムでシグナルの成功確率を予測したり、強化学習で最適なパラメータ組み合わせを探索する。これにより、戦略は新しい市場パターンに継続的に適応・学習できる。

-

時間枠分析の強化: 現在の戦略は主に単一時間枠で動作する。真のマルチタイムフレーム分析機能を追加することでシグナル品質を向上できる。例えば、日足、週足、月足のトレンド方向が一致した場合のみ取引を行うことで、逆張り取引のリスクを低減する。

-

ウィコフ識別アルゴリズムの改良: 現在のウィコフフェーズ識別は比較的単純である。出来高分布、出来高加重平均価格、相対力指標の組み合わせを使用するなど、より高度なアルゴリズムを開発してウィコフの蓄積・分配パターンを正確に識別できるようにする。

-

複数銘柄の相関分析: 複数銘柄の相関分析を追加することで、関連市場の動向を考慮できる。例えば、商品取引におけるドルインデックスの動きや、株式取引におけるセクターインデックスのパフォーマンスなどが考慮される。これにより、より包括的な市場視点が得られる。

-

エグジット戦略の最適化: 現在のエグジットメカニズムは主に時間とRSIに基づいている。動的支持・抵抗レベルに基づく部分利益確定や、ボラティリティ収縮パターンをエグジットトリガーとするなど、より複雑なエグジット戦略を実装することで収益性を向上できる。

-

リスク管理の強化: ドローダウンに基づくポジション調整、相関加重ポートフォリオ管理、市場流動性とスリッページを考慮した注文執行ロジックなど、より高度なリスク管理機能を追加する。

まとめ

マルチサイクル平均回帰トレンドブレイクアウトシステムは、中長期のスイングトレーダーに適した、包括的で柔軟な定量取引戦略である。その中核的優位性は、複数の相補的な取引手法の融合にあり、堅牢なシグナル生成メカニズムと広範なリスク管理機能を提供する。

本戦略は、ウィコフ市場サイクル理論、プライスプロファイル分析、平均回帰、トレンドフォローを統合することで、様々な市場環境に適応可能な取引システムを構築する。設計は機関投資家の資金フローと整合するようになっており、複数の確認を要求することで偽シグナルを低減し、柔軟な出入りメカニズムで取引結果を最適化する。

パラメータ最適化、複雑性管理、市場環境変化などの課題は存在するが、慎重な実装と継続的な最適化により、本戦略はトレーダーのツールボックスにおける強力な武器となる。適応的パラメータ、機械学習技術、強化されたマルチタイムフレーム分析、改良されたエグジット戦略を導入することで、将来的にさらなるパフォーマンス向上と適応性拡大が期待できる。

堅牢でシステム化された取引手法を求めるトレーダーにとって、マルチサイクル平均回帰トレンドブレイクアウトシステムは、個人の選好や市場経験に基づいてカスタマイズ・拡張可能な強固な基盤を提供する。

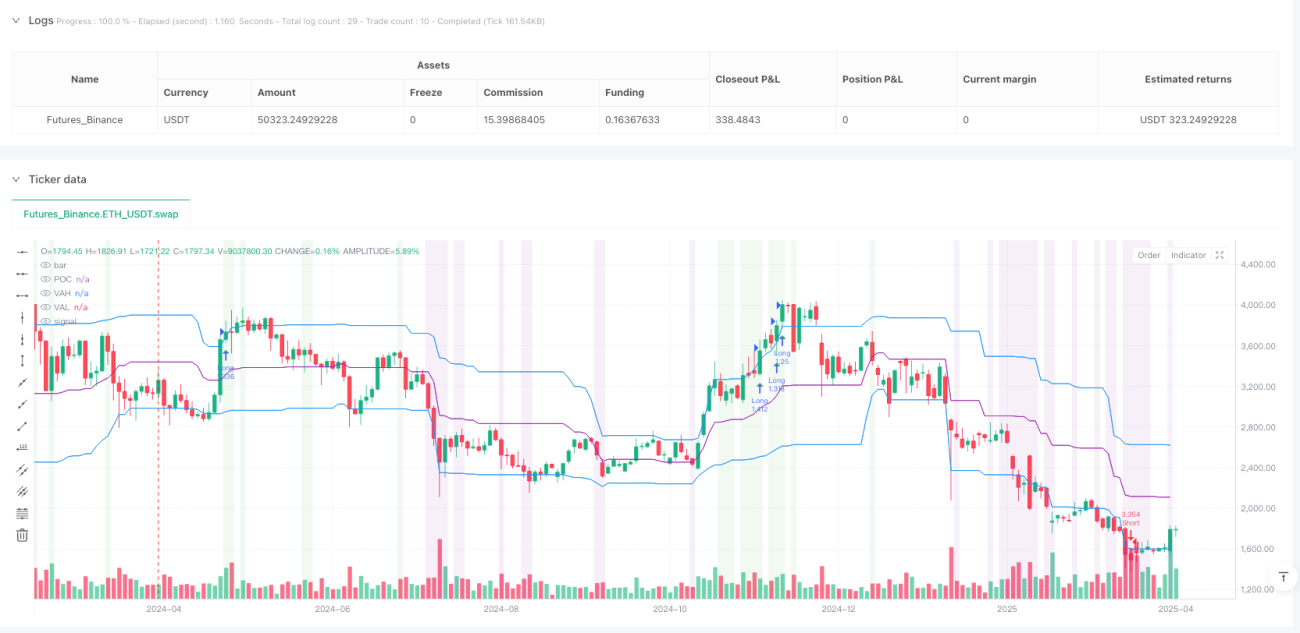

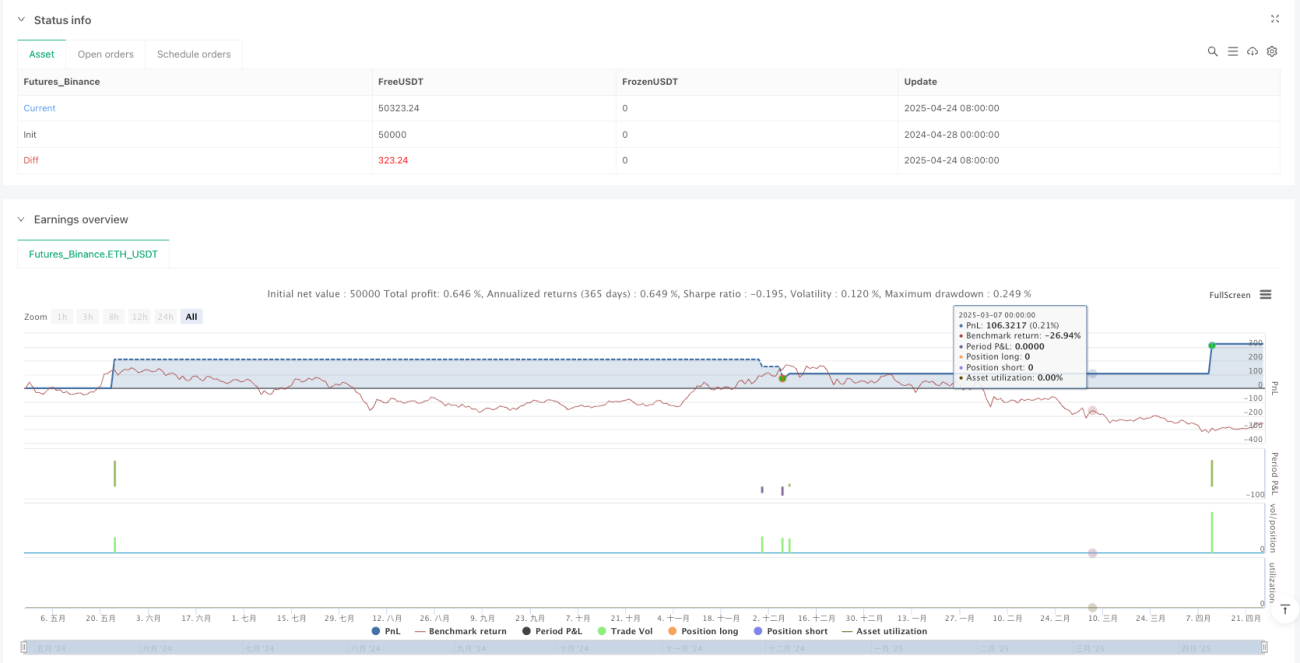

/*backtest

start: 2024-04-28 00:00:00

end: 2025-04-26 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Wyckoff Advanced Swing Strategy by TIAMATCRYPTO", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Main strategy settings- 1