パラメータ乗数戦略:複数指標融合のマーケットメトロノーム

🎯 これはどんな神戦略?

ご存知ですか?この戦略は、まるで市場に「スーパーレーダー」を取り付けたようなものです!単純に1つや2つの指標を見るのではなく、9つの異なるテクニカル指標をバンドのように組み合わせ、各指標が「楽器」となり、それらが調和のとれた「音符」を奏でたときにのみ、戦略は取引シグナルを発します。想像してみてください。まるで9人の専門家が同時にあなたの耳元でアドバイスをし、大多数が同意したときだけ行動するようなものです!

📊 核心原理を大公開

ここがポイント!この戦略の真髄は「パラメータ乗数」の概念にあります。RSI、ADX、モメンタム、変化率、ATR、出来高、加速度、傾きなどの指標をまず同じ尺度に標準化し、それらを掛け合わせて「総合力値」を算出します。料理と同じで、各スパイスに最適な割合があり、この戦略は市場の様々な「スパイス」の完璧な配合を見つける手助けをします!総合力値がその移動平均線を越えたときが、エントリーの絶好のタイミングです。

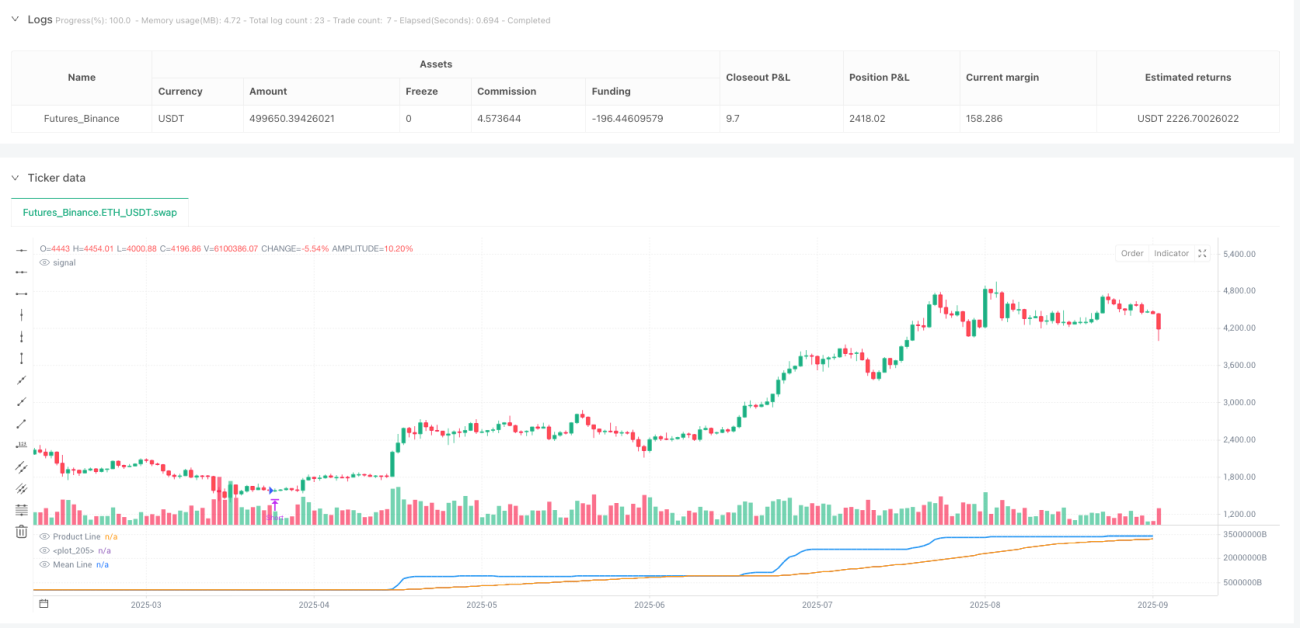

🔧 カスタマイズ可能な取引ツール

この戦略の最もクールな点は何でしょうか?レゴブロックのように自由に組み合わせられることです!特定の指標を使いたくない?直接オフにできます。期間パラメータを調整したい?お好きなように。さらに、SMAトレンドフィルターもあり、逆張りの落とし穴を回避するのに役立ちます。これはまるで「取引戦略DIYツールキット」であり、異なる市場環境に応じて設定を調整できます。

⚡ 実践応用ガイド

注意点ガイドをお届けします!この戦略は、レンジ相場とトレンド相場が混在する環境に特に適しています。青いプロダクトラインがオレンジの移動平均線を上抜けたら買い、下抜けたら売りです。戦略には自動的にポジションをクローズするメカニズムも組み込まれており、逆シグナルが発生した際にポジションを持ち続けてしまうことを防ぎます。トレンドフィルターをオンにすると大きなトレンドで有利に立ち回れ、オフにするとより多くの短期チャンスを捉えられることを覚えておいてください!

//@version=5

strategy("Parametric Multiplier Backtester", shorttitle="PMB", overlay=false)

// Author: Script_Algo

// License: MIT

// Permission is hereby granted, free of charge, to any person obtaining a copy

// of this software and associated documentation files (the "Software"), to deal

// in the Software without restriction, including without limitation the rights

// to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

// copies of the Software, subject to the following conditions:

// The above copyright notice and this permission notice shall be included in

// all copies or substantial portions of the Software.- 1