Protokol Enjin Volatiliti

Ini Bukan DCA Biasa, Ini Enjin Turun Naik yang Berotak

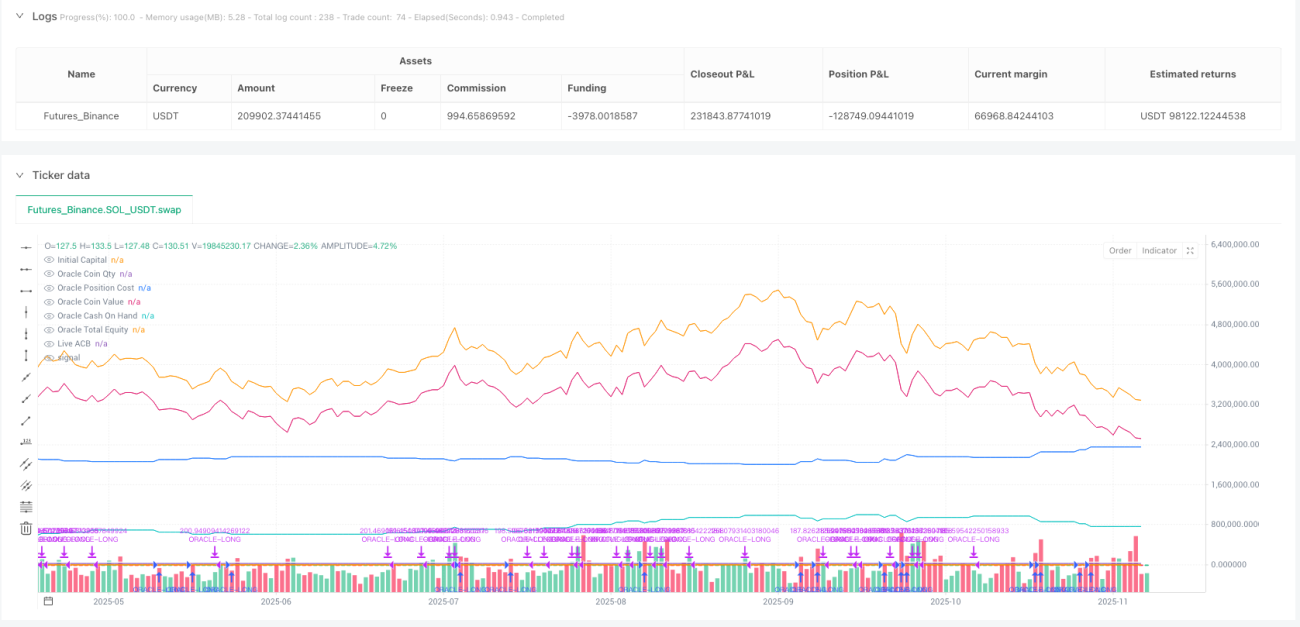

Data ujian balik secara langsung menampar pelaburan tetap tradisional: penurunan 5% mencetus pembelian, kenaikan 3.9% mencetus penjualan, tetapi kuncinya ialah enjin turun naik akan melaraskan ambang pembelian secara dinamik berdasarkan ATR. Semakin tinggi turun naik pasaran, semakin tinggi ambang pembelian, boleh dilaraskan sehingga maksimum 40%. Ini bermakna semasa tempoh turun naik tinggi, strategi akan menunggu penurunan yang lebih besar sebelum masuk.

Masalah strategi DCA tradisional ialah membeli tanpa berfikir, manakala logik teras protokol ini ialah hanya menembak di tingkap peluang sebenar. Melalui ATR(14), ia mengira turun naik semasa, kemudian melaraskan parameter longThreshPct secara dinamik. Contohnya, biasa beli pada penurunan 5%, tetapi jika turun naik semasa mencapai 20%, ambang pembelian sebenar akan dinaikkan kepada 6%.

8 Konfigurasi Pratetap, Setiap Satu Ada Jangkaan Pulangan yang Jelas

Mod Pengumpulan Kitaran BTC: beli pada penurunan 5%, saiz posisi 6%, jumlah tetap $500, sesuai untuk pemegang jangka panjang.

Mod Arbitraj Jangka Pendek BTC: beli pada penurunan 3.1%, saiz posisi 10%, jumlah tetap $6000, jual pada ambang keuntungan 75%.

Penuaian Turun Naik ETH: beli pada penurunan 4.5%, saiz posisi 15%, dibenarkan beli di bawah garis kos, ambang keuntungan 30%.

Setiap konfigurasi telah disahkan melalui ujian balik, bukan parameter yang diputuskan secara rambang. Konfigurasi SOL mempunyai ambang keuntungan 35%, konfigurasi XRP mempunyai ambang keuntungan 10%. Perbezaan ini mencerminkan ciri turun naik dan perbezaan kecairan aset yang berbeza.

Mekanisme Meterai Kluster: Menyelesaikan Masalah Terbesar Strategi DCA

Masalah terbesar DCA tradisional ialah tidak tahu bila untuk berhenti membeli. Protokol ini menyelesaikannya dengan "meterai kluster": sama ada harga naik 3.9% daripada kos purata, atau tiada peluang pembelian yang layak selama 10 kitaran berturut-turut, kluster semasa akan dimeteraikan.

Garis kos purata selepas dimeteraikan menjadi asas rujukan untuk penjualan. Hanya apabila harga menembusi garis kos meterai + ambang keuntungan (30%-75% berbeza), penjualan akan dicetuskan. Ini mengelakkan pembelian tanpa henti dan pengambilan untung terlalu awal.

Mekanisme tiang senyap merupakan satu langkah bijak: jika tiada syarat pembelian dicetuskan selama 10 kitaran berturut-turut, ini bermakna pasaran telah stabil, dan sudah tiba masanya untuk menuai, bukan terus mengumpul.

Kesan Roda Tenaga: Biarkan Keuntungan Melayani Pembelian Seterusnya

Selepas mengaktifkan mod roda tenaga, keuntungan setiap penjualan akan dilabur semula ke dalam kolam tunai, meningkatkan peluru untuk pembelian seterusnya. Ini bukan sekadar faedah kompaun, tetapi memberikan strategi kuasa tembakan yang lebih kuat dalam pasaran menaik.

Contoh: Modal awal $100,000, pengumpulan pusingan pertama untung 20%, selepas jual, kolam tunai menjadi $120,000. Pada pembelian seterusnya, saiz posisi 6% adalah $7,200, bukan $6,000. Dari masa ke masa, kesan bola salji ini akan membesarkan pulangan dengan ketara.

Tetapi roda tenaga juga ada kos: pada peringkat akhir pasaran menaik, kolam tunai yang terlalu besar boleh menyebabkan pembelian berlebihan, jadi perlu kawal ketat had pembelian sekali.

Kawalan Risiko: Tiga Mekanisme Insurans

Insurans Pertama: Kawalan pembelian di atas garis kos. Boleh tetapkan hanya beli di bawah kos purata untuk mengelakkan mengejar kenaikan.

Insurans Kedua: Had jumlah minimum. Setiap belian/penjualan mempunyai keperluan jumlah minimum dolar untuk mengelakkan dagangan kecil yang tidak bermakna.

Insurans Ketiga: Pelarasan enjin turun naik. Semasa turun naik tinggi, ambang pembelian dinaikkan secara automatik; semasa turun naik rendah, ambang diturunkan.

Tetapi strategi ini menunjukkan prestasi biasa dalam pasaran sisi. Jika pasaran mendatar untuk tempoh yang lama, ia tidak dapat mencetuskan penurunan besar untuk membeli, juga tidak dapat mencapai ambang keuntungan untuk menjual, dana akan terikat untuk jangka panjang.

Nasihat Praktikal: Pilih Pasaran yang Tepat adalah Kunci

Protokol ini paling sesuai untuk pasaran yang mempunyai arah aliran yang jelas, terutamanya pasaran kitaran kripto. Mula mengumpul pada akhir pasaran menurun, mula menuai pada pertengahan pasaran menaik, kesan terbaik.

Jangan gunakan dalam situasi berikut: 1) Pasaran saham yang turun naik frekuensi tinggi 2) Pasaran forex yang kekurangan arah aliran jelas 3) Syiling kecil dengan kecairan sangat rendah.

Ujian balik sejarah menunjukkan pulangan terlaras risiko lebih baik daripada pelaburan tetap ringkas, tetapi ini tidak bermakna ia pasti untung pada masa hadapan. Mana-mana strategi kuantitatif mempunyai risiko kegagalan dan perlu dipantau serta dilaraskan secara berterusan.

//@version=6

// ============================================================================

// ORACLE PROTOCOL — ARCH PUBLIC clone (Standalone) — CLEAN-PUB STYLE (derived)

// Variant: v1.9v-standalone (publish-ready) 25/11/2025

// Notes:

// - Keeps your v1.9v canonical script intact (this is a separate modified copy).

// - Single exit mode: ProfitGate + Candle (per-candle) — no selector.

// - Live ACB plot toggle only (sealed ACB still operates internally but is not shown).

// - No freeze-point markers plotted.

// - Sizing: flywheel dynamic sizing remains the primary source but fixed-dollar entry

// and min-$ overrides remain available (as in Arch public PDFs/screenshots).

// - Volatility Engine (VE) applies ONLY to entries; exit-side VE removed.- 1