Estratégia ATR multivariada de futuros de criptomoeda (ensino)

Recentemente, alguns usuários da plataforma estão ansiosos para migrar uma estratégia de linguagem Mai para uma estratégia JavaScript, para que possam adicionar com flexibilidade muitas ideias de otimização. Expanda até mesmo a estratégia para uma versão multissímbolo. Porque as estratégias da linguagem Mai geralmente são estratégias de tendência, e muitas delas são executadas com base em modelos de preço de fechamento. A estratégia não solicita a interface da API de troca com muita frequência, por isso é mais adequada para ser transplantada para uma versão de estratégia multivariada. Neste artigo, tomaremos uma estratégia simples da linguagem Mai como exemplo e a portaremos para uma versão simples da linguagem JavaScript. O objetivo principal é ensinar e testar pesquisas. Se você deseja realizar uma negociação em tempo real, pode ser necessário adicionar alguns detalhes (preço do pedido, precisão da quantidade, controle da quantidade do pedido, pedido por porcentagem de ativos, exibição de informações de status, etc.) e também precisa realizar uma negociação real. -teste de tempo.

A estratégia linguística a ser portada

TR:=MAX(MAX((H-L),ABS(REF(C,1)-H)),ABS(REF(C,1)-L));

ATR:=EMA(TR,LENGTH2);

MIDLINE^^EMA((H + L + C)/3,LENGTH1);

UPBAND^^MIDLINE + N*ATR;

DOWNBAND^^MIDLINE - N*ATR;

BKVOL=0 AND C>=UPBAND AND REF(C,1)<REF(UPBAND,1),BPK;

SKVOL=0 AND C<=DOWNBAND AND REF(C,1)>REF(DOWNBAND,1),SPK;

BKVOL>0 AND C<=MIDLINE,SP(BKVOL);

SKVOL>0 AND C>=MIDLINE,BP(SKVOL);

// 止损

// stop loss

C>=SKPRICE*(1+SLOSS*0.01),BP;

C<=BKPRICE*(1-SLOSS*0.01),SP;

AUTOFILTER;

A lógica de negociação desta estratégia é muito simples. Primeiro, o ATR é calculado com base nos parâmetros e, em seguida, a média dos preços mais altos, mais baixos e de fechamento de todos os BARs da linha K é calculada. O indicador EMA é obtido com base nesses dados médios. Por fim, combine ATR e o coeficiente N nos parâmetros. Calcule as bandas superior e inferior (upBand, downBand).

As posições de abertura e reversão são baseadas no preço de fechamento rompendo as faixas superior e inferior. Se ultrapassar o trilho superior, abra uma posição longa (ao manter uma posição curta); se ultrapassar o trilho inferior, abra uma posição curta.

Quando o preço de fechamento atinge a linha média, a posição é fechada, e quando o preço de fechamento atinge o preço de stop loss, a posição também é fechada (de acordo com o stop loss SLOSS, SLOSS é 1, que é 0,01, ou 1%).

A estratégia é executada em um modelo de preço de fechamento.

OK, agora que entendemos os requisitos estratégicos e as ideias da linguagem Mai, podemos começar a portabilidade.

Migração, protótipo de estratégia de design

O código do protótipo da estratégia não tem mais do que 1~200 linhas. Para facilitar o aprendizado das ideias de escrita da estratégia, os comentários são escritos diretamente no código da estratégia.

// 解析params参数,从字符串解析为对象

var arrParam = JSON.parse(params)

// 该函数创建图表配置

function createChartConfig(symbol, atrPeriod, emaPeriod, index) { // symbol : 交易对, atrPeriod : ATR参数周期 , emaPeriod : EMA参数周期 , index 对应的交易所对象索引

var chart = {

__isStock: true,

extension: {

layout: 'single',

height: 600,

},

title : { text : symbol},

xAxis: { type: 'datetime'},

series : [

{

type: 'candlestick', // K线数据系列

name: symbol,

id: symbol + "-" + index,

data: []

}, {

type: 'line', // EMA

name: symbol + ',EMA:' + emaPeriod,

data: [],

}, {

type: 'line', // upBand

name: symbol + ',upBand' + atrPeriod,

data: []

}, {

type: 'line', // downBand

name: symbol + ',downBand' + atrPeriod,

data: []

}, {

type: 'flags',

onSeries: symbol + "-" + index,

data: [],

}

]

}

return chart

}

// 主要逻辑

function process(e, kIndex, c) { // e 即交易所对象,exchanges[0] ... , kIndex K线数据在图表中的数据系列, c 为图表对象

// 获取K线数据

var r = e.GetRecords(e.param.period)

if (!r || r.length < e.param.atrPeriod + 2 || r.length < e.param.emaPeriod + 2) {

// K线数据长度不足则返回

return

}

// 计算ATR指标

var atr = TA.ATR(r, e.param.atrPeriod)

var arrAvgPrice = []

_.each(r, function(bar) {

arrAvgPrice.push((bar.High + bar.Low + bar.Close) / 3)

})

// 计算EMA指标

var midLine = TA.EMA(arrAvgPrice, e.param.emaPeriod)

// 计算上下轨

var upBand = []

var downBand = []

_.each(midLine, function(mid, index) {

if (index < e.param.emaPeriod - 1 || index < e.param.atrPeriod - 1) {

upBand.push(NaN)

downBand.push(NaN)

return

}

upBand.push(mid + e.param.trackRatio * atr[index])

downBand.push(mid - e.param.trackRatio * atr[index])

})

// 画图

for (var i = 0 ; i < r.length ; i++) {

if (r[i].Time == e.state.lastBarTime) {

// 更新

c.add(kIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close], -1)

c.add(kIndex + 1, [r[i].Time, midLine[i]], -1)

c.add(kIndex + 2, [r[i].Time, upBand[i]], -1)

c.add(kIndex + 3, [r[i].Time, downBand[i]], -1)

} else if (r[i].Time > e.state.lastBarTime) {

// 添加

e.state.lastBarTime = r[i].Time

c.add(kIndex, [r[i].Time, r[i].Open, r[i].High, r[i].Low, r[i].Close])

c.add(kIndex + 1, [r[i].Time, midLine[i]])

c.add(kIndex + 2, [r[i].Time, upBand[i]])

c.add(kIndex + 3, [r[i].Time, downBand[i]])

}

}

// 检测持仓

var pos = e.GetPosition()

if (!pos) {

return

}

var holdAmount = 0

var holdPrice = 0

if (pos.length > 1) {

throw "同时检测到多空持仓!"

} else if (pos.length != 0) {

holdAmount = pos[0].Type == PD_LONG ? pos[0].Amount : -pos[0].Amount

holdPrice = pos[0].Price

}

if (e.state.preBar == -1) {

e.state.preBar = r[r.length - 1].Time

}

// 检测信号

if (e.state.preBar != r[r.length - 1].Time) { // 收盘价模型

if (holdAmount <= 0 && r[r.length - 3].Close < upBand[upBand.length - 3] && r[r.length - 2].Close > upBand[upBand.length - 2]) { // 收盘价上穿上轨

if (holdAmount < 0) { // 持有空仓,平仓

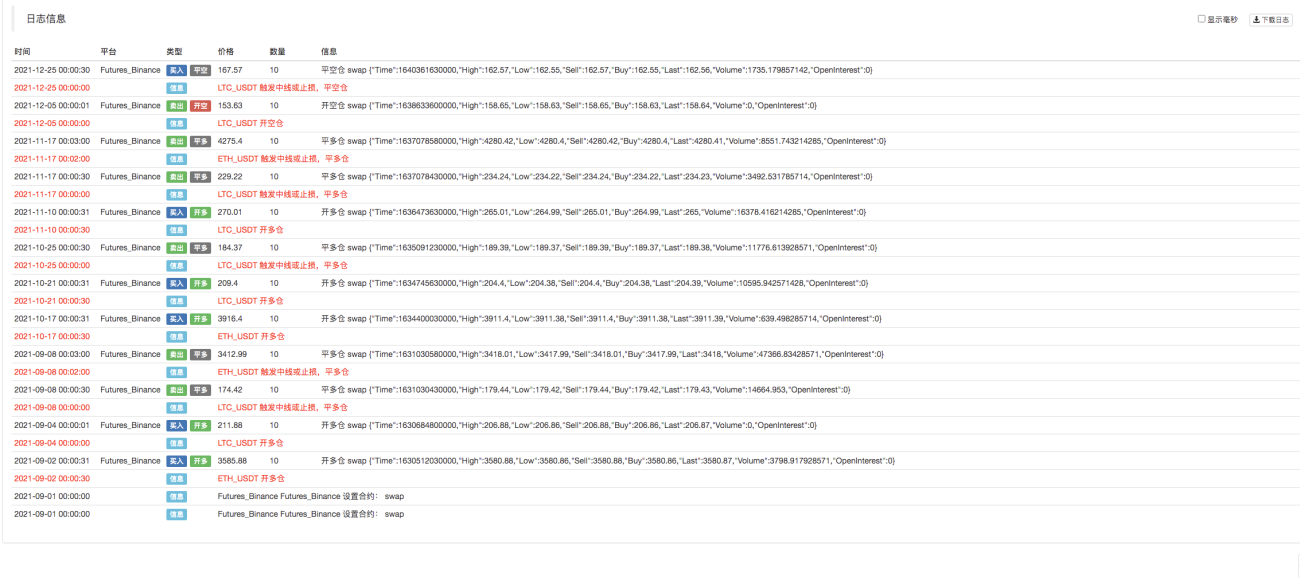

Log(e.GetCurrency(), "平空仓", "#FF0000")

$.CoverShort(e, e.param.symbol, Math.abs(holdAmount))

c.add(kIndex + 4, {x: r[r.length - 2].Time, color: 'red', shape: 'flag', title: '平', text: "平空仓"})

}

// 开多

Log(e.GetCurrency(), "开多仓", "#FF0000")

$.OpenLong(e, e.param.symbol, 10)

c.add(kIndex + 4, {x: r[r.length - 2].Time, color: 'red', shape: 'flag', title: '多', text: "开多仓"})

} else if (holdAmount >= 0 && r[r.length - 3].Close > downBand[downBand.length - 3] && r[r.length - 2].Close < downBand[downBand.length - 2]) { // 收盘价下穿下轨

if (holdAmount > 0) { // 持有多仓,平仓

Log(e.GetCurrency(), "平多仓", "#FF0000")

$.CoverLong(e, e.param.symbol, Math.abs(holdAmount))

c.add(kIndex + 4, {x: r[r.length - 2].Time, color: 'green', shape: 'flag', title: '平', text: "平多仓"})

}

// 开空

Log(e.GetCurrency(), "开空仓", "#FF0000")

$.OpenShort(e, e.param.symbol, 10)

c.add(kIndex + 4, {x: r[r.length - 2].Time, color: 'green', shape: 'flag', title: '空', text: "开空仓"})

} else {

// 平仓

if (holdAmount > 0 && (r[r.length - 2].Close <= holdPrice * (1 - e.param.stopLoss) || r[r.length - 2].Close <= midLine[midLine.length - 2])) { // 持多仓,收盘价小于等于中线,按开仓价格止损

Log(e.GetCurrency(), "触发中线或止损,平多仓", "#FF0000")

$.CoverLong(e, e.param.symbol, Math.abs(holdAmount))

c.add(kIndex + 4, {x: r[r.length - 2].Time, color: 'green', shape: 'flag', title: '平', text: "平多仓"})

} else if (holdAmount < 0 && (r[r.length - 2].Close >= holdPrice * (1 + e.param.stopLoss) || r[r.length - 2].Close >= midLine[midLine.length - 2])) { // 持空仓,收盘价大于等于中线,按开仓价格止损

Log(e.GetCurrency(), "触发中线或止损,平空仓", "#FF0000")

$.CoverShort(e, e.param.symbol, Math.abs(holdAmount))

c.add(kIndex + 4, {x: r[r.length - 2].Time, color: 'red', shape: 'flag', title: '平', text: "平空仓"})

}

}

e.state.preBar = r[r.length - 1].Time

}

}

function main() {

var arrChartConfig = []

if (arrParam.length != exchanges.length) {

throw "参数和交易所对象不匹配!"

}

var arrState = _G("arrState")

_.each(exchanges, function(e, index) {

if (e.GetName() != "Futures_Binance") {

throw "不支持该交易所!"

}

e.param = arrParam[index]

e.state = {lastBarTime: 0, symbol: e.param.symbol, currency: e.GetCurrency()}

if (arrState) {

if (arrState[index].symbol == e.param.symbol && arrState[index].currency == e.GetCurrency()) {

Log("恢复:", e.state)

e.state = arrState[index]

} else {

throw "恢复的数据和当前设置不匹配!"

}

}

e.state.preBar = -1 // 初始设置-1

e.SetContractType(e.param.symbol)

Log(e.GetName(), e.GetLabel(), "设置合约:", e.param.symbol)

arrChartConfig.push(createChartConfig(e.GetCurrency(), e.param.atrPeriod, e.param.emaPeriod, index))

})

var chart = Chart(arrChartConfig)

chart.reset()

while (true) {

_.each(exchanges, function(e, index) {

process(e, index + index * 4, chart)

Sleep(500)

})

}

}

function onexit() {

// 记录 e.state

var arrState = []

_.each(exchanges, function(e) {

arrState.push(e.state)

})

Log("记录:", arrState)

_G("arrState", arrState)

}

Parâmetros de estratégia:

var params = '[{

"symbol" : "swap", // 合约代码

"period" : 86400, // K线周期,86400秒即为一天

"stopLoss" : 0.07, // 止损系数,0.07即7%

"atrPeriod" : 10, // ATR指标参数

"emaPeriod" : 10, // EMA指标参数

"trackRatio" : 1, // 上下轨系数

"openRatio" : 0.1 // 预留的开仓百分比,暂时没支持

}, {

"symbol" : "swap",

"period" : 86400,

"stopLoss" : 0.07,

"atrPeriod" : 10,

"emaPeriod" : 10,

"trackRatio" : 1,

"openRatio" : 0.1

}]'

Testes retrospectivos

Código fonte da estratégia: https://www.fmz.com/strategy/339344

A estratégia serve apenas para backtesting, aprendizado e pesquisa. Por favor, modifique, otimize e consulte o mercado atual você mesmo.

- 1