Estratégia de rastreamento de tendência em múltiplos timeframes com stop loss e take profit baseados em ATR

Visão Geral

Esta é uma estratégia de negociação de tendência que combina o UT Bot com a Média Móvel Exponencial (EMA) de 50 períodos. A estratégia opera principalmente em gráficos de 1 minuto para negociações de curto prazo, utilizando a linha de tendência do período de 5 minutos como filtro direcional. O ATR é usado para calcular dinamicamente o stop loss, e são definidos dois níveis de take profit para otimizar os ganhos.

Princípio da Estratégia

A lógica central da estratégia baseia-se nos seguintes componentes-chave:

- Uso do UT Bot para calcular níveis dinâmicos de suporte e resistência.

- Utilização da EMA de 50 períodos no gráfico de 5 minutos para determinar a direção geral da tendência.

- Combinação da EMA de 21 períodos com os sinais do UT Bot para identificar pontos de entrada específicos.

- Definição de stop loss dinâmico através de múltiplos do ATR.

- Estabelecimento de dois alvos de take profit (0,5% e 1%) para encerrar 50% da posição cada.

Quando o preço rompe os níveis de suporte/resistência calculados pelo UT Bot e ocorre um cruzamento entre a EMA de 21 períodos e o UT Bot, se o preço estiver na direção correta da EMA de 50 períodos de 5 minutos, o sinal de negociação é acionado.

Vantagens da Estratégia

- A combinação de múltiplos períodos de tempo aumenta a confiabilidade das negociações.

- O stop loss dinâmico baseado no ATR se adapta automaticamente à volatilidade do mercado.

- Os dois alvos de take profit equilibram ganhos e taxa de acerto.

- O uso de velas Heikin Ashi ajuda a filtrar alguns falsos rompimentos.

- Suporte flexível para direções de negociação (apenas compra, apenas venda ou ambos).

Riscos da Estratégia

- Negociações de curto prazo podem enfrentar spreads e custos de corretagem elevados.

- Em mercados laterais, podem ocorrer sinais falsos frequentes.

- As múltiplas condições podem levar à perda de algumas oportunidades potenciais.

- Os parâmetros do ATR precisam ser otimizados para diferentes mercados.

Direções de Otimização da Estratégia

- Adicionar indicadores de volume como confirmação auxiliar.

- Considerar a incorporação de mais indicadores de sentimento do mercado.

- Desenvolver parâmetros adaptativos para diferentes características de volatilidade.

- Adicionar filtros de horário de negociação.

- Desenvolver um sistema de gerenciamento de posições mais inteligente.

Resumo

A estratégia constrói um sistema de negociação completo através da combinação de múltiplos indicadores técnicos e períodos de tempo. Ela não apenas define condições claras de entrada e saída, mas também oferece um mecanismo robusto de gerenciamento de risco. Embora ainda exija a otimização de parâmetros de acordo com as condições específicas do mercado na prática, a estrutura geral tem boa utilidade e flexibilidade de expansão.

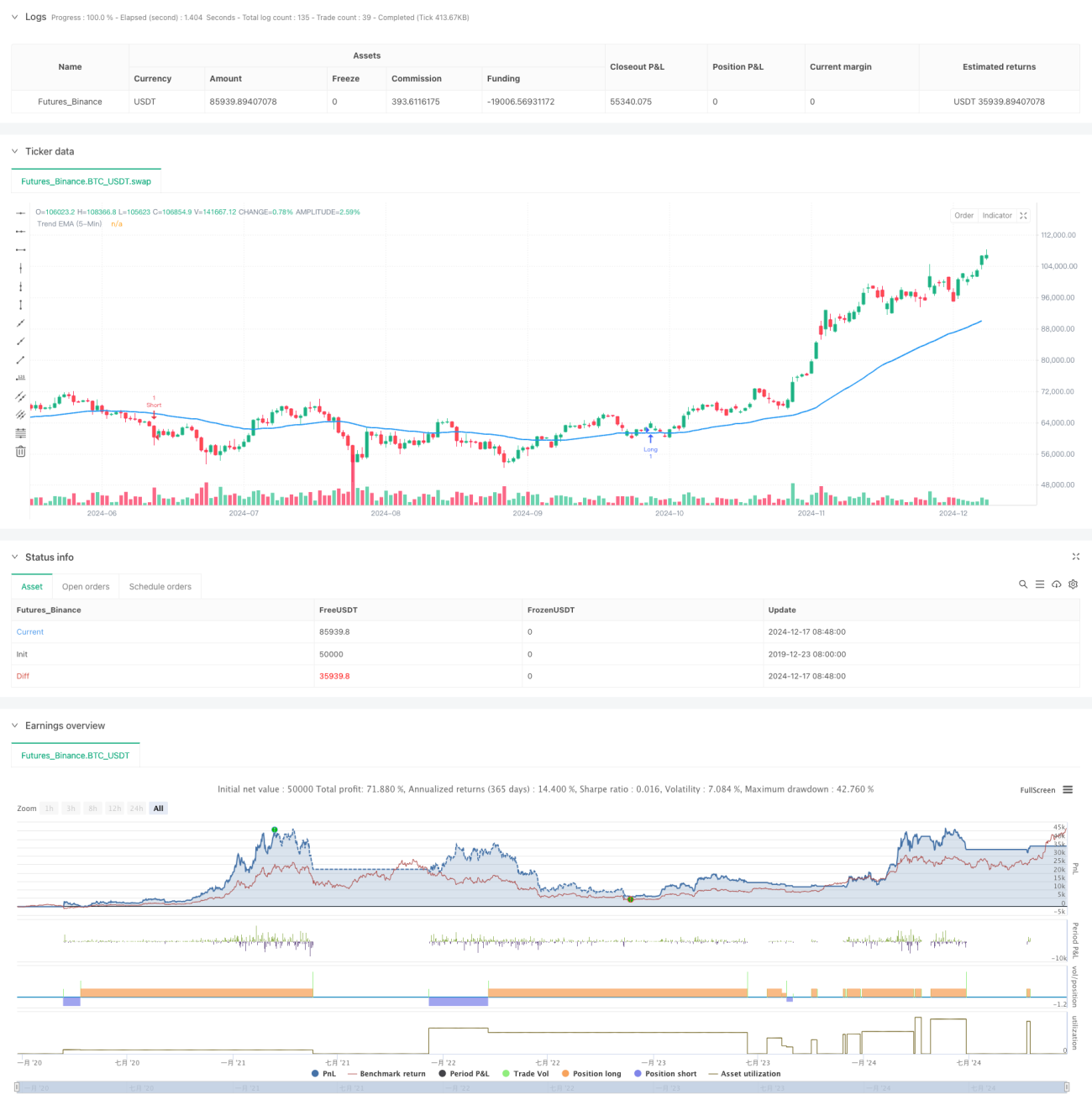

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

- 1