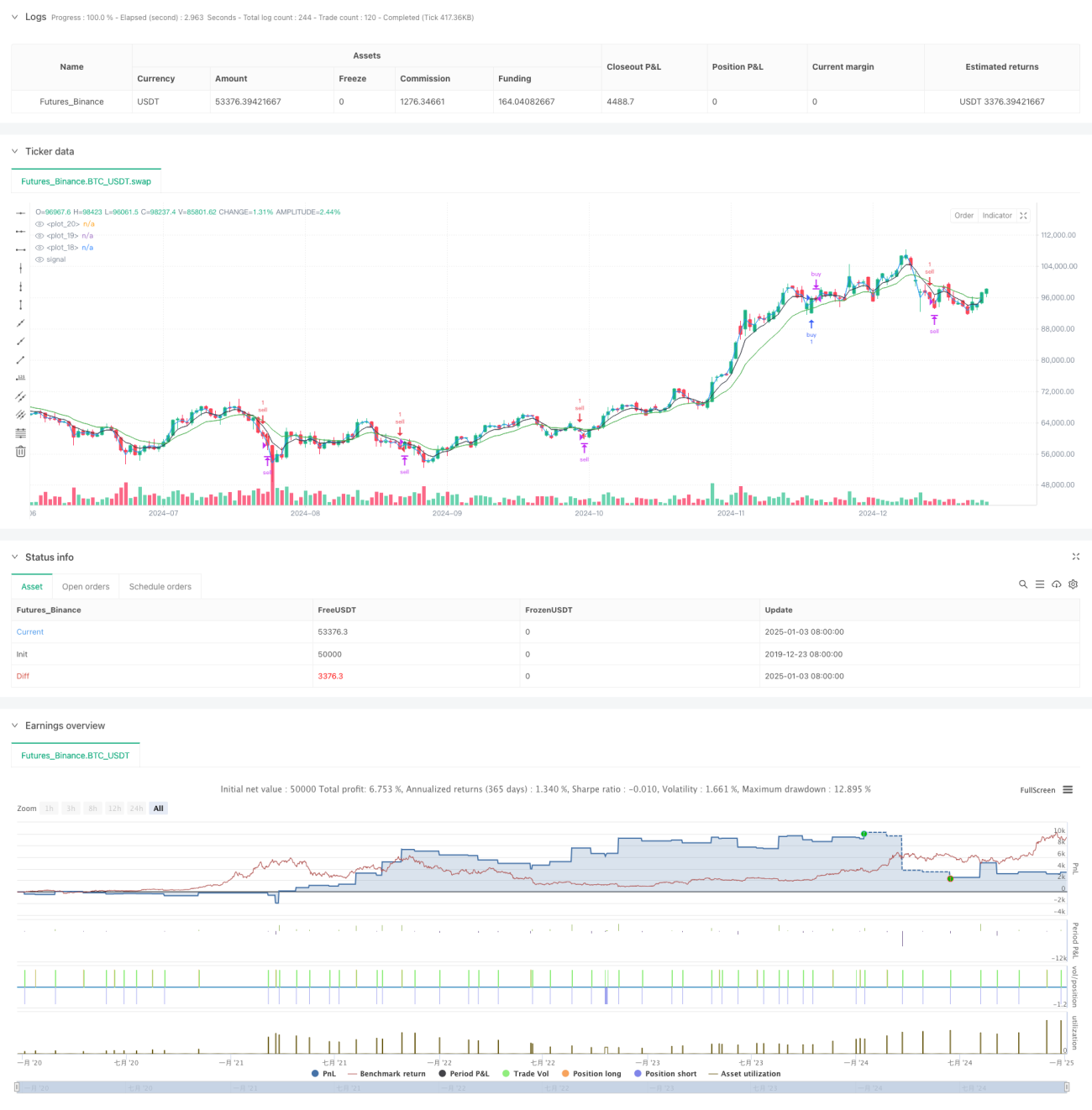

Esta é uma estratégia de negociação de momentum abrangente baseada em múltiplos indicadores de cruzamento de médias móveis e indicadores de preço e volume. A estratégia gera sinais de negociação com base na combinação de múltiplos indicadores, como o cruzamento das médias móveis exponenciais (EMA) rápidas e lentas, o preço médio ponderado por volume (VWAP) e o SuperTrend, além de incorporar condições como janelas de tempo intradiário e faixas de variação de preço para controlar entradas e saídas.

Princípio da Estratégia

A estratégia utiliza as EMAs de 5 e 13 períodos como principais indicadores de tendência. Quando a EMA rápida cruza acima da EMA lenta e o preço de fechamento está acima do VWAP, é gerado um sinal de compra (long). Quando a EMA rápida cruza abaixo da EMA lenta e o preço de fechamento está abaixo do VWAP, é gerado um sinal de venda (short). Além disso, a estratégia incorpora o indicador SuperTrend como confirmação de tendência e base para stop loss. São estabelecidas diferentes condições de entrada para diferentes dias de negociação, incluindo a variação do preço em relação ao fechamento anterior e a faixa de oscilação entre máxima e mínima do dia.

Vantagens da Estratégia

- A combinação de múltiplos indicadores técnicos aumenta a confiabilidade dos sinais de negociação.

- Condições de entrada diferenciadas para diferentes dias de negociação melhoram a adaptação às características do mercado.

- Mecanismos dinâmicos de take profit e stop loss permitem um controle eficaz de riscos.

- A restrição de janelas de tempo intradiário evita riscos durante períodos de alta volatilidade.

- A limitação baseada em pontos máximos/mínimos anteriores e faixas de oscilação de preço reduz o risco de comprar em topos e vender em fundos.

Riscos da Estratégia

- Podem ocorrer sinais falsos em movimentos rápidos de mercado.

- Pode haver atraso no início de reversões de tendência.

- A otimização de parâmetros pode apresentar risco de overfitting.

- Os custos de negociação podem impactar a rentabilidade da estratégia.

- Períodos de alta volatilidade do mercado podem resultar em grandes drawdowns.

Direções de Otimização

- Considerar a introdução de indicadores de análise de volume para confirmar ainda mais a força da tendência.

- Otimizar as configurações de parâmetros para diferentes dias de negociação, aumentando a adaptabilidade da estratégia.

- Adicionar mais indicadores de sentimento do mercado para melhorar a precisão das previsões.

- Aprimorar os mecanismos de take profit e stop loss para aumentar a eficiência do uso de capital.

- Considerar a inclusão de indicadores de volatilidade para otimizar o gerenciamento de posições.

Resumo

Esta estratégia combina o acompanhamento de tendência com a negociação de momentum por meio do uso integrado de múltiplos indicadores técnicos. O design considera a diversidade do mercado, adotando regras de negociação diferenciadas para diferentes dias de negociação. Com controle de risco rigoroso e mecanismos flexíveis de take profit e stop loss, a estratégia demonstra bom valor de aplicação prática. No futuro, a estabilidade e a lucratividade da estratégia podem ser aprimoradas com a introdução de mais indicadores técnicos e a otimização de parâmetros.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=6

strategy("S1", overlay=true)

fastEMA = ta.ema(close, 5)- 1