Visão Geral

Esta estratégia é um sistema de acompanhamento de tendências baseado em volume e variação de preços, que prevê a direção do mercado calculando o oscilador de volume líquido (NVO). A estratégia combina vários tipos de médias móveis (EMA, WMA, SMA, HMA), comparando a posição do oscilador com sua linha de sobreposição EMA para determinar a tendência do mercado e realizar negociações no momento adequado. A estratégia também inclui mecanismos de stop loss e take profit para controlar riscos e garantir lucros.

Princípio da Estratégia

O núcleo da estratégia é calcular o valor do oscilador de volume líquido diário para avaliar o sentimento do mercado. As etapas de cálculo específicas são:

- Cálculo do multiplicador da faixa de preço: com base no preço máximo, mínimo e de fechamento do dia, calcula-se um multiplicador entre 0 e 1.

- Cálculo do volume efetivo de alta e baixa: pondera-se o volume de acordo com a direção da variação de preço e o multiplicador.

- Cálculo do volume líquido: subtrai-se o volume efetivo de baixa do volume efetivo de alta.

- Aplicação da média móvel selecionada: suaviza-se os dados de volume líquido.

- Cálculo da linha de sobreposição EMA: usada como linha de referência para julgar a tendência.

- Cálculo da taxa de variação (ROC): utilizada para avaliar mudanças na intensidade da tendência.

Os sinais de negociação são gerados com base nas seguintes regras:

- Condição de compra: o oscilador cruza acima da linha de sobreposição EMA.

- Condição de venda: o oscilador cruza abaixo da linha de sobreposição EMA.

- Stop loss: com base em um percentual do preço.

- Take profit: com base em um percentual do preço.

Vantagens da Estratégia

- Análise multidimensional: combina informações de três dimensões: preço, volume e taxa de variação da tendência.

- Alta flexibilidade: suporta vários tipos de médias móveis, podendo ser ajustada conforme diferentes características do mercado.

- Gerenciamento de risco completo: inclui mecanismos de stop loss e take profit, controlando riscos de forma eficaz.

- Visualização forte: exibe mudanças na intensidade da tendência através de histogramas, facilitando a compreensão do estado do mercado.

- Alta adaptabilidade: através do design parametrizado, pode se adaptar a diferentes ambientes de mercado e instrumentos de negociação.

Riscos da Estratégia

- Risco de reversão de tendência: pode gerar sinais falsos frequentes em mercados laterais.

- Risco de atraso: as médias móveis possuem certo atraso, o que pode resultar em entrada e saída em momentos não ideais.

- Sensibilidade a parâmetros: diferentes combinações de parâmetros podem levar a grandes variações no desempenho da estratégia.

- Dependência do ambiente de mercado: pode ter desempenho insatisfatório em certas condições de mercado.

- Limitação técnica: depende apenas de indicadores técnicos, sem considerar fatores fundamentais.

Recomendações de controle de risco:

- Recomenda-se otimizar parâmetros em diferentes ambientes de mercado.

- Pode-se combinar com outros indicadores técnicos para confirmação de sinais.

- Ajustar adequadamente os parâmetros de stop loss e take profit para se adaptar a diferentes volatilidades do mercado.

Direções de Otimização da Estratégia

-

Otimização do mecanismo de confirmação de sinal:

- Adicionar condição de confirmação de volume.

- Incluir filtro de intensidade de tendência.

- Introduzir mecanismo adaptativo de volatilidade.

-

Otimização do gerenciamento de risco:

- Implementar stop loss dinâmico.

- Adicionar módulo de gerenciamento de capital.

- Introduzir mecanismos de construção e redução gradual de posições.

-

Otimização de parâmetros:

- Desenvolver mecanismo de ajuste adaptativo de parâmetros.

- Implementar troca de parâmetros com base no ambiente de mercado.

- Adicionar modelo de aprendizado de máquina para otimização de parâmetros.

Resumo

Esta estratégia constrói um sistema de acompanhamento de tendências relativamente completo através da análise integrada de dados de volume e preço. A principal característica da estratégia é combinar vários indicadores técnicos e oferecer opções flexíveis de configuração de parâmetros. Embora existam certos riscos, com controle de risco razoável e otimização contínua, a estratégia tem potencial para obter ganhos estáveis em negociações reais. Recomenda-se que os traders realizem backtests completos antes de usar a estratégia ao vivo e ajustem os parâmetros adequadamente conforme as condições específicas do mercado.

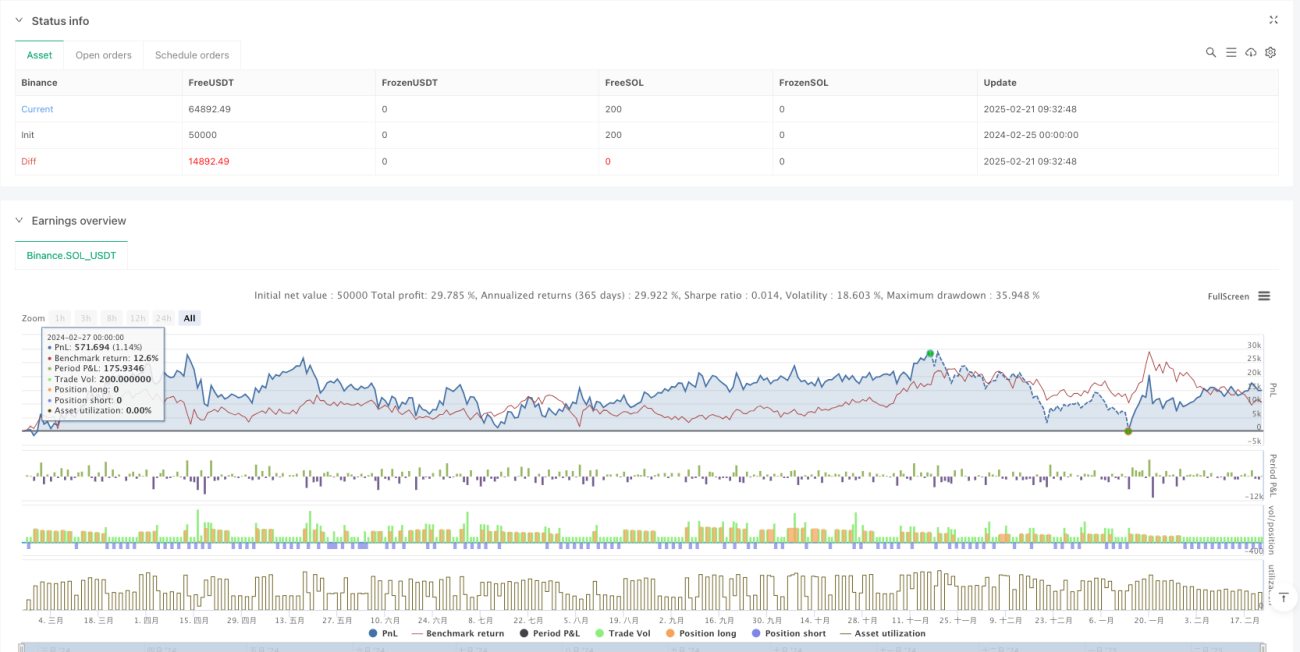

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("EMA-Based Net Volume Oscillator with Trend Change", shorttitle="NVO Trend Change", overlay=false, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input parameters- 1