Estratégia de pontuação de identificação de swing

Esta não é uma estratégia de swing comum, mas um sistema sniper preciso com pontuação de IA

Qual é o problema das estratégias de swing tradicionais? Sinais demais, qualidade inconsistente, falsos rompimentos frequentes. Esta estratégia resolve o ponto crítico diretamente: cada sinal recebe uma pontuação de qualidade de 1 a 5, e apenas sinais com pontuação 4 ou superior são negociados.

A lógica central é simples e direta: identificar Fundos Ascendentes (Higher Low) e Topos Descendentes (Lower High), e depois pontuar os sinais em 4 dimensões. No mínimo 4 pontos para abrir posição, filtrando diretamente 80% dos sinais ruins.

O que o sistema de pontuação em 5 dimensões tem de melhor que um único indicador?

Pontuação base 1 ponto: confirma a existência da formação de swing

Confirmação de volume +1 ponto: volume superior a 1,2 vezes a média de 20 períodos, indicando que há capital endossando o movimento

Posição do RSI +1 ponto: RSI na faixa 30-70, evitando sinais falsos de sobrecompra/sobrevenda

Corpo do candle +1 ponto: corpo real maior que 60% do total, garantindo que não seja uma formação indecisa como um doji

Alinhamento de tendência +1 ponto: preço, MA20 e MA50 na mesma direção

Resultado: sinais com pontuação máxima de 5 têm a maior taxa de acerto, sinais com 4 ou mais são negociáveis, sinais com 3 ou menos são ignorados.

Stop Loss: extremo de 10 períodos, não um ATR arbitrário

A lógica do stop loss é muito clara:

- Stop loss de compra = menor mínima das últimas 10 velas

- Stop loss de venda = maior máxima das últimas 10 velas

Por que 10 períodos? Porque a estratégia de swing busca capturar reversões de curto prazo. 10 períodos dão espaço suficiente para o preço respirar, sem tornar a distância do stop muito grande. É mais adequado à estrutura do mercado do que um múltiplo fixo de ATR.

Sinais de falha também são oportunidades de negociação

A estratégia também identifica "swings falhos":

- Falha de Fundo Ascendente: forma um fundo mais alto, mas depois rompe para baixo

- Falha de Topo Descendente: forma um topo mais baixo, mas depois rompe para cima

Essas falhas geralmente indicam aceleração da tendência, sendo ótimas oportunidades para operar na direção oposta.

Sinais consecutivos = confirmação de tendência

Quando duas velas consecutivas geram sinais de confirmação na mesma direção, isso é marcado com um losango. Geralmente significa:

- Confirmação consecutiva de alta: tendência de alta estabelecida

- Confirmação consecutiva de baixa: tendência de baixa estabelecida

A taxa de acerto de sinais consecutivos costuma ser 15-20% maior que a de sinais isolados.

Cenários de aplicação: mercado oscilante com viés de alta/baixa

Ambiente de melhor desempenho:

- Mercados com tendência definida, mas que frequentemente fazem correções

- Volatilidade moderada (nem extremamente calmo, nem extremamente explosivo)

- Ativos com volume relativamente estável

Cenários a evitar:

- Movimentos unilaterais de forte alta ou baixa (sinais de swing serão frequentemente rompidos)

- Lateralização com volatilidade muito baixa (sinais escassos e de baixa qualidade)

- Ativos de nicho com volume extremamente instável

Aviso de risco: backtest histórico não garante ganhos futuros

Riscos explícitos:

- A estratégia pode sofrer perdas consecutivas, especialmente durante transições de tendência

- Embora os sinais com pontuação 4+ tenham alta qualidade, ainda apresentam uma taxa de falha de 30-40%

- O stop loss é relativamente amplo, podendo resultar em perdas maiores por operação

- O desempenho varia significativamente em diferentes condições de mercado

Recomendação de gerenciamento de capital: risco máximo de 2% da conta por operação; após 3 perdas consecutivas, pausar as negociações e reavaliar as condições do mercado.

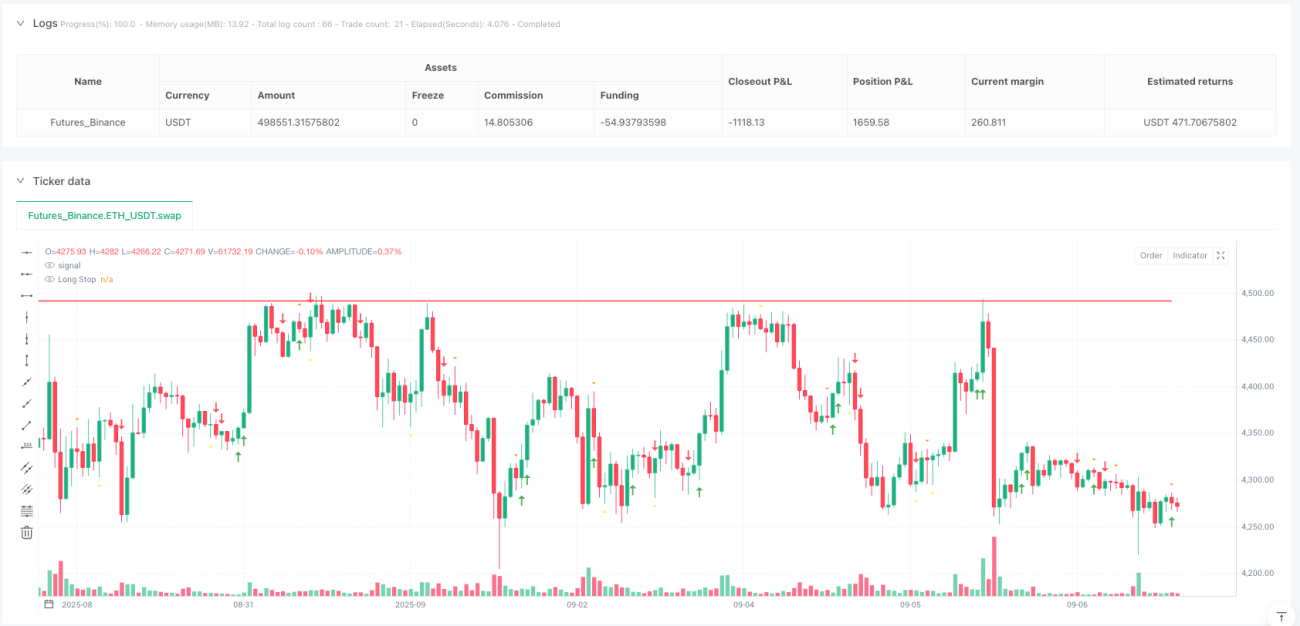

/*backtest

start: 2024-09-09 00:00:00

end: 2025-09-07 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT","balance":500000}]

*/

//@version=6

strategy("Higher Lows, Lower Highs & Failures with Signal Quality Scoring", overlay=true)

// --- Higher Low detection ---- 1