Estratégia de Multiplicador de Parâmetros: O Metrônomo de Mercado com Fusão de Múltiplos Indicadores

🎯 Que estratégia divina é essa?

Sabia? Esta estratégia é como instalar um "super radar" no mercado! Não se trata apenas de observar um ou dois indicadores, mas de combinar 9 indicadores técnicos diferentes como uma orquestra. Cada indicador é um "instrumento" e só quando eles tocam "notas" harmoniosas é que a estratégia emite um sinal de negociação. Imagine que você tem 9 especialistas dando conselhos ao mesmo tempo – você só age quando a maioria concorda!

📊 Revelação do princípio central

Ponto-chave! A essência desta estratégia está no conceito de "multiplicador de parâmetros". Ela padroniza indicadores como RSI, ADX, Momentum, Taxa de Variação, ATR, Volume, Aceleração e Inclinação para a mesma escala e depois os multiplica para obter um "valor de força combinada". É como cozinhar: cada tempero tem sua proporção ideal. Esta estratégia ajuda a encontrar a combinação perfeita dos "temperos" do mercado! Quando o valor de força combinada cruza sua média móvel, é o momento ideal para entrar.

🔧 Ferramenta de negociação personalizável

Qual é a parte mais legal desta estratégia? Você pode montá-la como blocos de montar! Não quer usar um indicador? Desligue-o diretamente. Quer ajustar os períodos? Fique à vontade. Ainda tem um filtro de tendência SMA para evitar os grandes buracos de negociar contra a tendência. É como um "kit de ferramentas DIY para estratégias de negociação", permitindo ajustar a configuração conforme as diferentes condições do mercado.

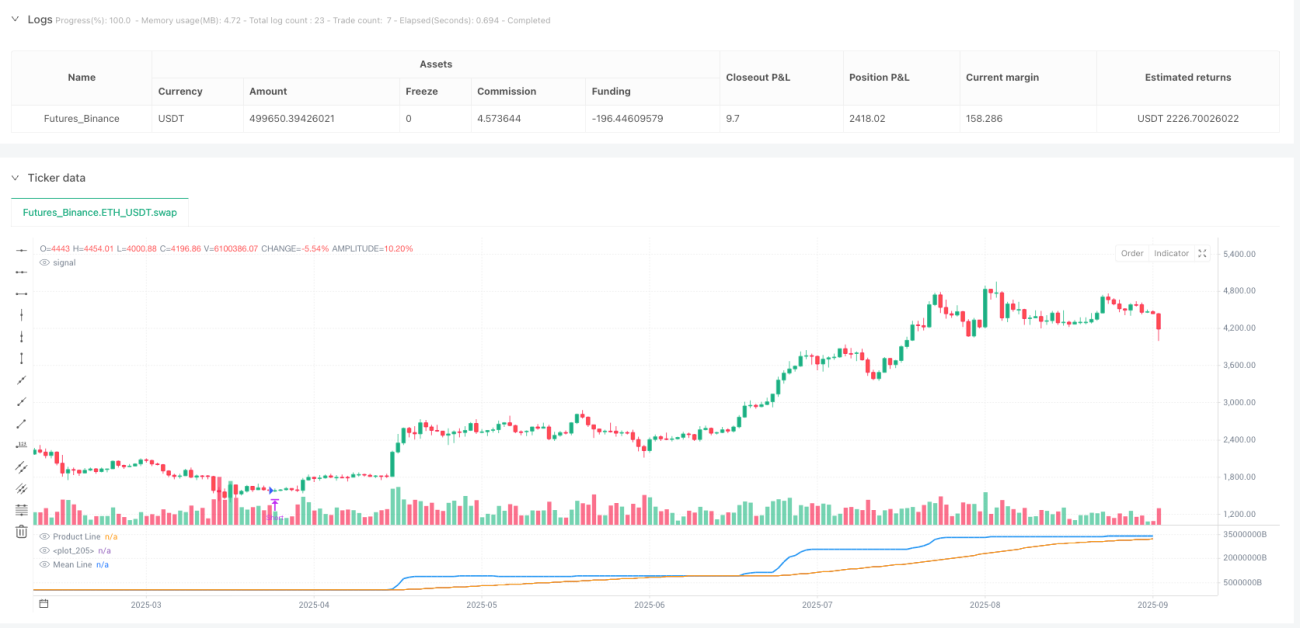

⚡ Guia de aplicação prática

Dica para evitar armadilhas! Esta estratégia é particularmente adequada para mercados mistos de oscilação e tendência. Quando a linha azul do produto cruza para cima a média móvel laranja, compre; quando cruza para baixo, venda. A estratégia também possui um mecanismo automático de fechamento de posição, evitando que você continue segurando uma posição quando um sinal contrário aparece. Lembre-se: ativar o filtro de tendência permite que você navegue com facilidade nas grandes tendências; desativá-lo captura mais oportunidades de curto prazo!

//@version=5

strategy("Parametric Multiplier Backtester", shorttitle="PMB", overlay=false)

// Author: Script_Algo

// License: MIT

// Permission is hereby granted, free of charge, to any person obtaining a copy

// of this software and associated documentation files (the "Software"), to deal

// in the Software without restriction, including without limitation the rights

// to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

// copies of the Software, subject to the following conditions:

// The above copyright notice and this permission notice shall be included in

// all copies or substantial portions of the Software.- 1