Protocolo do Motor de Volatilidade

Isto não é um DCA normal, é um motor de volatilidade com inteligência

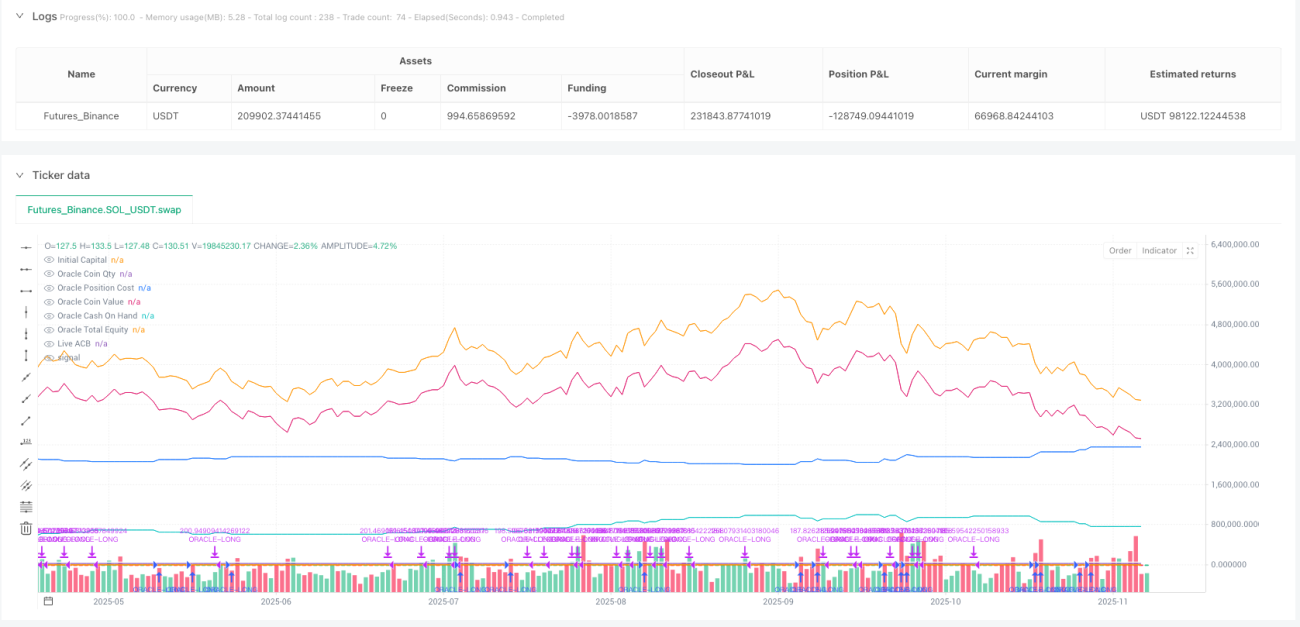

Os dados de backtest refutam diretamente o DCA tradicional: gatilho de compra com queda de 5%, gatilho de venda com alta de 3,9%, mas o segredo está no motor de volatilidade que ajusta dinamicamente o limiar de compra com base no ATR. Quanto maior a volatilidade do mercado, maior o limite de compra, podendo ser ajustado em até 40%. Isso significa que, durante períodos de alta volatilidade, a estratégia espera quedas maiores para entrar.

O problema da estratégia DCA tradicional é comprar sem pensar, enquanto a lógica central deste protocolo é disparar apenas em janelas de oportunidade reais. Através do ATR(14), calcula-se a volatilidade atual e ajusta-se dinamicamente o parâmetro longThreshPct. Por exemplo, normalmente compra-se com queda de 5%, mas se a volatilidade atual atingir 20%, o limiar real de compra será elevado para 6%.

8 configurações predefinidas, cada uma com expectativas claras de retorno

Modo de acumulação cíclica BTC: compra com queda de 5%, posição de 6%, valor fixo de 500 dólares, ideal para holders de longo prazo.

Modo de arbitragem de curto prazo BTC: compra com queda de 3,1%, posição de 10%, valor fixo de 6.000 dólares, venda com limite de lucro de 75%.

Colheita de volatilidade ETH: compra com queda de 4,5%, posição de 15%, permite compra abaixo do custo médio, limite de lucro de 30%.

Cada configuração foi validada por backtest, não são parâmetros decididos aleatoriamente. A configuração SOL tem limite de lucro de 35%, a configuração XRP tem limite de lucro de 10%. Essas diferenças refletem as características de volatilidade e liquidez de cada ativo.

Mecanismo de selamento de cluster: resolve o maior problema do DCA

O maior problema do DCA tradicional é não saber quando parar de comprar. Este protocolo resolve com o "selamento de cluster": ou o preço sobe 3,9% acima do custo médio, ou não há nenhuma oportunidade de compra qualificada por 10 períodos consecutivos, selando o cluster de acumulação atual.

A linha de custo médio após o selamento torna-se a referência base para venda. A venda só é acionada quando o preço ultrapassa a linha de custo selada + limite de lucro (variando de 30% a 75%). Isso evita compras intermináveis e lucros prematuros.

O mecanismo de barra de silêncio é um toque de mestre: se não houver condição de compra por 10 períodos consecutivos, significa que o mercado se estabilizou, e é hora de se preparar para colher, não para continuar acumulando.

Efeito flywheel: faz o lucro servir para a próxima compra

Com o modo flywheel ativado, o lucro de cada venda é reinvestido no pool de caixa, aumentando a munição para a próxima compra. Não é juros compostos simples, mas sim dar à estratégia um poder de fogo mais forte durante o mercado de alta.

Exemplo: capital inicial de $100.000, primeira acumulação com lucro de 20%, após a venda o pool de caixa se torna $120.000. Na próxima compra, a posição de 6% será de $7.200 em vez de $6.000. Com o tempo, este efeito bola de neve amplifica significativamente os retornos.

Mas o flywheel tem um custo: no final do mercado de alta, o pool de caixa grande demais pode levar a compras excessivas, exigindo controle rigoroso do limite máximo por compra.

Controle de risco: mecanismo de tripla segurança

Primeira barreira: controle de compra acima da linha de custo. Pode-se configurar para comprar apenas abaixo do custo médio, evitando comprar em picos.

Segunda barreira: limite de valor mínimo. Cada compra/venda tem um valor mínimo em dólar, evitando transações pequenas e irrelevantes.

Terceira barreira: ajuste do motor de volatilidade. Durante alta volatilidade, o limiar de compra é automaticamente aumentado; durante baixa volatilidade, é reduzido.

Mas esta estratégia tem desempenho medíocre em mercados laterais. Se o mercado ficar muito tempo em range, sem conseguir acionar quedas significativas para compra nem atingir o limite de lucro para venda, o capital fica preso por muito tempo.

Conselhos práticos: escolher o mercado é crucial

Este protocolo é mais adequado para mercados com tendências claras, especialmente os ciclos do mercado de criptomoedas. Acumular no final do bear market e colher no meio do bull market traz os melhores resultados.

Não use nas seguintes situações: 1) mercados de ações com alta volatilidade frequente 2) mercados de câmbio sem tendência clara 3) criptomoedas pequenas com liquidez extremamente baixa.

Os backtests históricos mostram retornos ajustados ao risco superiores ao DCA simples, mas isto não significa lucro garantido no futuro. Qualquer estratégia quantitativa corre risco de falha, exigindo monitoramento e ajustes contínuos.

//@version=6

// ============================================================================

// ORACLE PROTOCOL — ARCH PUBLIC clone (Standalone) — CLEAN-PUB STYLE (derived)

// Variant: v1.9v-standalone (publish-ready) 25/11/2025

// Notes:

// - Keeps your v1.9v canonical script intact (this is a separate modified copy).

// - Single exit mode: ProfitGate + Candle (per-candle) — no selector.

// - Live ACB plot toggle only (sealed ACB still operates internally but is not shown).

// - No freeze-point markers plotted.

// - Sizing: flywheel dynamic sizing remains the primary source but fixed-dollar entry

// and min-$ overrides remain available (as in Arch public PDFs/screenshots).

// - Volatility Engine (VE) applies ONLY to entries; exit-side VE removed.- 1